The Sales and Service Tax (SST) is Malaysia’s current consumption tax framework, implemented in 2018 as a replacement for the Goods and Services Tax (GST). It consists of two distinct components:

Sales Tax, which is imposed on taxable goods that are manufactured locally or imported; and

Service Tax, which applies to specific prescribed services provided within Malaysia.

For comprehensive details and official guidance, please refer to the Royal Malaysian Customs Department (RMCD) website at mysst.customs.gov.my.

Under the expanded scope of the Sales and Service Tax (SST) framework for the financial services sector, a Regulated Financial Services Provider is deemed a taxable person and is required to register with the RMCD if the value of taxable financial services exceeds RM1 million within a 12-month period.

As a Regulated Financial Services Provider, MIMMB falls within the scope of the updated regulations. Accordingly, its services will be subject to Service Tax at the rate of 8%, effective from the implementation date.

MIMMB will begin applying the Sales and Service Tax (SST) effective 1 October 2025, in accordance with the expanded scope of the SST framework introduced by the Government of Malaysia.

The SST charges will be borne by the investor.

Note: Where applicable, SST will be calculated based on the fee amount and will be reflected in your transaction statement.

SST is applicable if any fees—such as sales charge, admin fee or exit fee—are incurred during the switching transaction.

No, income or dividend distributions—whether received in cash or reinvested—are not subject to SST.

Yes, SST applies to foreign investors if the transactions are conducted within Malaysia.

Yes. If you exercise your cooling-off right, any SST paid in relation to the transaction will be refunded accordingly.

The implementation of SST affects the calculation of fees associated with transactions. Below is a breakdown of how SST is applied:

Calculation Details (after SST)

Sales Charge Calculation

= Investment Amount / (1 + Sales Charge (%) + SST (%)) × Sales Charge (%)

= RM10,000 / (1 + 0.05 + [0.05 × 0.08]) × 0.05

= RM10,000 / 1.054 × 0.05

= RM474.38

SST on Sales Charge

= Sales Charge × SST(%)

= RM474.38 × 8%

= RM37.95

Net Investment Amount

= Investment Amount − Sales Charge − SST

= RM10,000 − RM474.38 − RM37.95

= RM9,487.67

*MIMMB - Manulife Investment Management (M) Berhad

FAQs for Foreign Account Tax Compliance Act (FATCA) and Common Reporting Standards (CRS)

Non-EPF investment – Individual

Investment via EPF Members Investment Scheme

Termination of EPF Members Investment Scheme

Monthly switching instruction (MSI)

Amendment of account holder's particulars

Financial process exchange (FPX) collection application

FAQs for Manulife PRS Nestegg Series, Manulife PRS Shariah Nestegg Series (Class C Units)

FAQs for Manulife iFunds Regular Savings Plan (RSP)

Please fill up Unit Holder Maintenance form with your latest details and submit to your Servicing Advisor, MIMMB Branch offices or email it to us at MY_CustomerService@manulife.com

You may obtain a copy of the Unit Holder Maintenance form from/ by:

(i) any of our branches; or

(ii) downloading a copy from our company website: https://www.manulifeim.com.my/content/dam/wam/my/en/resources/forms/UH-M.pdf; or

(iii) contacting your Servicing Advisor; or

(iv) contacting Manulife’s Customer Service Hotline at 03-2719 9271; or

(v) email to us at MY_CustomerService@manulife.com

You may update your other tax residency country and tax-payer identification number (TIN) using FATCA & CRS Self-certification form.

If there is any change in circumstances regarding your tax residency status, this change resulted the information disclosed in the FATCA & CRS Self-certification form become inaccurate or incomplete, you must notify us within 30 days by submitting a new FATCA & CRS Self-certification form.

You may obtain a copy of the Unit Holder Maintenance form from/ by:

(i) any of our branches; or

(ii) downloading a copy from our company website: https://www.manulifeim.com.my/content/dam/wam/my/en/resources/forms/individual-controlling-person-self-certification-form.pdf; or

(iii) contacting your Servicing Advisor; or

(iv) contacting Manulife’s Customer Service Hotline at 03-2719 9271; or email to us at MY_CustomerService@manulife.com

Under the FATCA provisions, we are required to conduct due diligence and reporting in accordance with IGA signed between US government and Malaysia Government. We are required to determine if you are a US person or not as part of the due diligence process. As such, there are occasions where we may require from you to provide FATCA form even if you are not a US person.

Compliance with the CRS is mandatory under Malaysian law and require us to collect certain information from customer(s) in order to establish customer(s)’ country (or countries) of tax residence.

You may be required to provide us with a CRS form(s) to confirm your country (or countries) of tax residence. Furthermore, where circumstances require, we may request additional information and documentation from you. This includes, in some cases, a new CRS form, even though you have submitted the same to us in the past.

Without a valid CRS form from you, it may not be possible for you to open a new account with us. In certain circumstances, we may, decline to enter into any further transaction with you, and/or close your existing account(s) with Manulife.

Individuals aged 18 and above on their last birthday.

Yes, but only limited to one joint holder.

Yes, a minor below 18 years old. He / she must invest as a designated account holder together with a first holder who is 18 years old or above.

No.

The company will notify the unit holder and his/her UT Adviser and the investment will be reversed and cancelled accordingly.

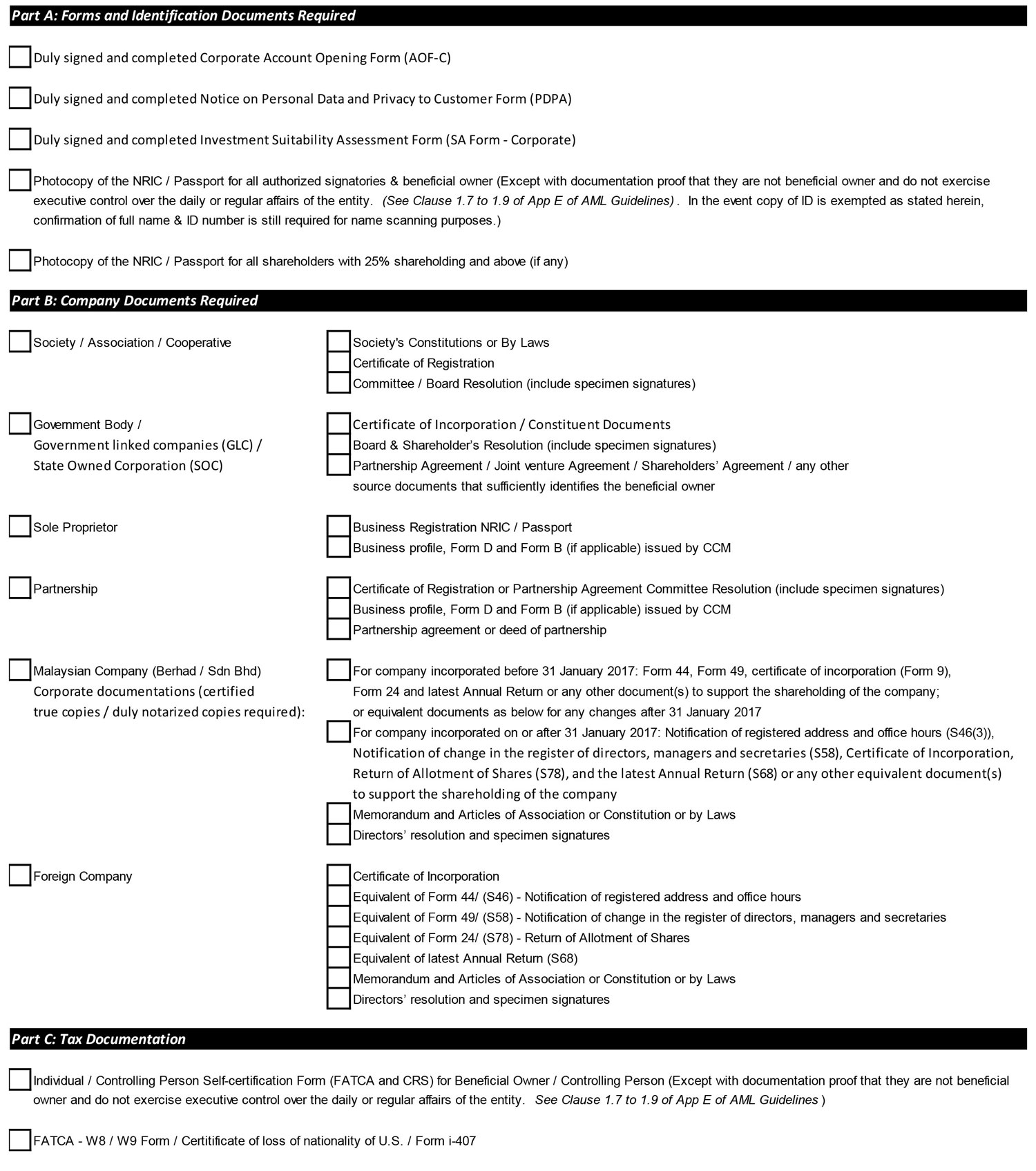

A first time investor is required to submit a duly completed Account Opening Form, a photocopy of NRIC, a Suitability Assessment (SA) Form and a Consent On Personal Data And Privacy Form.

For subsequent investment in a new fund, the investor is required to submit a duly signed Additional Investment Slip.

While for an additional investment in an existing fund, only Additional Investment Slip (need not be signed) is to be submitted.

The prospective investor may contact our Customer Service Hotline at 03-2719 9271 or visit the nearest MIMMB branch offices.

Payment may be made through MIMMB Branch Offices / Service Centres as indicated in the Prospectuses.

Cheques, bank drafts or cashiers orders should be made payable to "Manulife Investment Management (M) Berhad-Client Trust Account " and crossed "ACCOUNT PAYEE ONLY". Please write your name, new NRIC/Passport number and telephone number at the back of all cheques, bank drafts or cashiers orders.

Cheques, bank drafts or cashiers orders payable to the Company must be issued or purchased by the respective unit holder(s). For bank drafts or cashiers orders, a copy of the Remittance Application Form must be submitted together with the required investment documents.

A unit holder can issue one cheque for multiple funds and multiple accounts.

Investors are advised to read and understand the Master Prospectus and the respective Product Highlights Sheet(s) for minimum transaction amount.

There is no maximum limit to invest, however, any investment amount in excess of 10% of the fund size would require the approval of MIMMB's senior management.

Visit our website at www.manulifeim.com.my to view our fund prospectuses or contact our Customer Service Hotline at 03-2719 9271

Yes. If he/she is an existing MIMMB unit holder , he/she can invest via Maybanwww.maybank2u.com.my

The cut-off time for submission of investment on any Business Day, is 3.00pm over the service counter, 4.00pm for online payment and 11.30am on a Bursa Malaysia half day trading day.

Yes. Applicable only to Manulife Investment Growth Fund with a minimum Net Asset Value (NAV) of RM10,000.00.

Yes. He/ She is required to complete the "Nominee For Insurance" of the Account Opening Form or Unit Holder Record Maintenance Form for an existing investor.

Units would be created on the NAV per unit at the end of the Business Day on which the requests for purchase are received or deemed to have been received by the Manager at or before 3.00pm (4.00pm for online payment) and 11.30am on a Bursa Malaysia half day trading day. Any application received after the cut-off time would be considered as being transacted on the next Business Day.

To be eligible, he/she must be below 55 years old. Please refer to www.kwsp.gov.my for more information.

A completed Account Opening Form or Additional Investment Slip, KWSP 9N (AHL) Form, a certified true copy of MyKad (front and back on the same page of an A4-sized paper). A first time investor is required to complete a Suitability Assessment (SA) Form and a Consent On Personal Data And Privacy Form.

Investment can be made at anytime (subject to eligible investment amount in 3 months time).

The amount to be withdrawn must not be less than RM1,000 and not more than 30 per cent of the amount exceeding the required Basic Savings in Account 1. Refer www.kwsp.gov.my for more information.

No.

The company will notify the unit holder and his/her UT Adviser and the investment will be reversed and cancelled accordingly.

A Transaction Statement.

Yes. He/ She can provide a toe print.

Units would be created on the NAV per unit at the end of the Business Day on which the requests for purchase are received or deemed to have been received by the Manager at or before 3.00pm and 11.30am on a Bursa Malaysia half day trading day. Any application received after the cut-off time would be considered as being transacted on the next Business Day.

No. Before EPF disburses the payment to MIMMB, the investment is considered as "Float" units. These units cannot be redeemed or switched into another fund. After EPF disburses the payment to MIMMB, the investment is considered as confirmed units and these units can then be redeemed or switched into another fund.

No.

Unit holder may submit a photocopy of duly verified Maklumat Kandungan Cip which can be obtained from Jabatan Pendaftaran Negara (JPN). The KWSP 9N (AHL) Form, a certified true copy of MyKad and the Maklumat Kandungan Cip will be forwarded to EPF for processing.

EPF will take 1 – 2 weeks to process such cases.

No.

The next of kin of the unit holder needs to inform the EPF that the unit holder has passed away. EPF will then send a release control letter to MIMMB. After the account has been transferred to a non-EPF account, the beneficiary may apply to transfer or repurchase the units from the deceased unit holder's account by submitting relevant documents such as Letter of Administration or Grant of Probate.

The purpose of the release control letter, issued by EPF, is for EPF to relinquish control of the Member's EPF investment to MIMMB. Thereafter, the unit holder has the right to repurchase the units (the cheque is made payable to his name) or transfer the units to a third party.

No.

Yes. A letter will be sent to the unit holder after the account has been converted to a Non-EPF account.

Any corporation, society, association, government and non-government body that is registered in Malaysia or overseas.

First-time investor is required to submit a duly completed forms and documents as below:

For subsequent investment in a new fund, the investor is required to submit a duly signed Additional Investment Slip and provide valid payment proof.

While for an additional investment in an existing fund, Additional Investment Slip (need not be signed) and provide valid payment proof are required to be submitted.

Yes. Provided it is stated in the Board of Directors’ Resolution to the Manager.

Yes, however, the cooling-off period is only applicable to any person investing for the first time in any unit trust funds managed by MIMMB and it excludes corporations / institutions, staff of MIMMB and persons registered to deal in unit trusts. Unit holders have the right, within six (6) Business Days of the receipt by MIMMB of their application for units, to call for a withdrawal of their investment.

However, for EPF investments' investors are not entitled to cooling-off rights.

No.

The request to exercise your cooling-off rights must be submitted to any MIMMB branch offices or service centres or head office within six (6) business days commencing from the date of purchase. MIMMB will refund the applicant within seven (7) business days upon receipt of the cooling-off notice.

A completed Repurchase Form.

Any MIMMB branch offices or service centres or head office.

No.

No.

Investors are advised to read and understand the Master Prospectus and the respective Product Highlights Sheet(s) for minimum transaction units and the minimum holding of the fund.

No.

For MPC unit holders, it is company policy that the repurchase cheque be issued within T+2 calendar days (provided the following is a business day) from the date of receipt of the duly completed repurchase documents.

For non-MPC unit holders, it is company policy that the repurchase cheque be issued within 7 calendar days from the date of receipt of the duly completed repurchase documents.

However, the industry practice is 7 business days from the date of receipt of the duly completed repurchase documents to issue the repurchase cheques.

Yes but only into Maybank or RHB, unless he/ she is a MPC member.

No. However, for special request to dispatch the repurchase cheque by courier or registered mail, the courier or registered mail charges will be borne by the unit holder and will be deducted from the repurchase proceeds accordingly.

The repurchase amount will be based on the NAV per unit at the end of the Business Day on which the requests for repurchase are received or deemed to have been received by the Manager at or before 3.00pm and 11.30am on a Bursa Malaysia half day trading day. Any request received after this cut-off time would be considered as being transacted on the next Business Day.

The unit holder can enclose a "Regular Investment Amendment (RIA) Form" upon submission of a repurchase request. The monthly standing instruction will then be cancelled.

Switching of fund is a facility which enables a unit holder to convert units of a particular fund for the units of other funds managed by MIMMB.

Yes. RM25 per transaction (deducted from the switching amount) except for :

a. The first 6 switching transactions in a calendar year.

b. MPC unit holders.

c. Monthly Switching Instruction.

d. Switching at NAV Price with sales charge.

The switching amount will be based on the NAV per unit at the end of the Business Day on which the requests for switching are received or deemed to have been received by the Manager at or before 3.00pm and 11.30am on a Bursa Malaysia half day trading day. Any request received after this cut-off time would be considered as being transacted on the next Business Day.

A completed Switching Form.

For switching request into a new fund, a Suitability Assessment (SA) Form is required if you have not completed one previously.

Investors are advised to read and understand the Master Prospectus and the respective Product Highlights Sheet(s) for minimum transaction units / amount and the minimum holding of the fund.

If the switching is made to an initial (new) fund, the net amount switched after deduction of sales charge (if any) must meet the minimum requirement of the fund's initial investment amount.

The unit holder can enclose a “Regular Investment Amendment (RIA) Form” upon submission of his/her switching request. The monthly standing instruction will be credited into the new fund (switched to new fund).

Online Switching of fund is an online facility which enables a unit holder to convert units of a particular fund for the units of any other fund managed by MIMMB.

The switching amount will be based on the NAV per unit at the end of the Business Day on which the requests for switching are received or deemed to have been received by the Manager at or before 4.00pm and 11.30am on a Bursa Malaysia half day trading day. Any request received after this cut-off time would be considered as being transacted on the next Business Day.

Investors are advised to read and understand the Master Prospectus and the respective Product Highlights Sheet(s) for minimum transaction units / amount and the minimum holding of the fund.

If the Switching request is made to an initial (new) investment, the net amount switched after deduction of sales charge (if any) must meet the minimum initial investment required by the switch-to fund.

A Suitability Assessment (SA) Form is required if you have not completed one previously.

Yes. Please submit one request for each fund. For example, if you switch from three different funds, you need to submit three requests.

Yes. Investor is allowed to switch from one fund to a maximum of five funds but adviser is allowed to switch from one fund to a maximum of three funds.

Yes. There is an administrative charge of RM15 per request (deducted from the switching amount) except for :

a. The first 6 switching transactions in a calendar year

b. MPC unitholders

c. Switching at NAV Price with sales charge

d. Switching out from Manulife Investment Asia-Pacific REIT Fund within 30 calendar days of purchase which has a 1% exit fee

e. Switching out from Manulife Investment-HW Shariah Flexi Fund within 90 calendar days of purchase which has a 1% exit fee

Monthly Switching Instruction is a facility for an existing unit holder who wish to switch from one fund to another on a regular basis.

The unit holder(s) and the UT Adviser of the "switched from" and "switched to" fund must be within the same account. All applications must be submitted to MIMMB by the 5th of the month. Otherwise, it will be considered as the following month's request.

The minimum number of units for each MSI is 100 units.

No.

The Switching date is on the 15th day of each month. If the 15th of the month falls on a non-business day, the price will be based on the valuation determined at the end of the next Bursa Malaysia business day.

A unit holder may request to increase, decrease, change funds or cancel Monthly Switching Instruction by completing a Monthly Switching Instruction (MSI) Form.

For request to change funds or to switch into new funds, a Suitability Assessment (SA) Form is required if the unit holder has not completed one previously.

In the event of insufficient units in a unit holder's fund portfolio, the Monthly Switching will not be effected for the month concerned. Subsequent monthly Switching Instruction will only be effected when there are sufficient units in the unit holder's fund portfolio.

Yes, you are advised to inform MIMMB in writing, in the event you wish to cancel/increase/decrease your Monthly Switching Instruction. However, the Fund Managers reserve the right to terminate your Monthly Switching Instruction for payments that are unsuccessful for three (3) consecutive months.

The person transferring the units.

The person to whom the units of investment are transferred to and must be related to the transferor.

A completed Transfer Form, a photocopy of NRIC of transferor and transferee, documentations to support relationship, an Account Opening Form , a Suitability Assessment (SA) Form and a Consent On Personal Data And Privacy Form if the transferee is a first time investor of MIMMB.

Yes.

Investors are advised to read and understand the Master Prospectus and the respective Product Highlights Sheet(s) for minimum transaction units.

Investors are advised to read and understand the Master Prospectus and the respective Product Highlights Sheet(s) for minimum holding of the fund.

A RM3.00 charge will be deducted from the transfer. This charge is waived for transfer of units for a deceased unit holder and for MPC unit holders.

No. Transfer must be made within the same fund in different accounts.

A Transaction Request Form for Deceased Account, a copy of Letter of Administration or Grant of Probate, photocopy of NRIC of beneficiary(s), an Account Opening Form, a Suitability Assessment (SA) Form and a Consent On Personal Data And Privacy Form if the beneficiary(s) is a first time investor of MIMMB.

A unit holder may write to us or complete the Unit Holder Record Maintenance Form and submit the form to any MIMMB branch offices or service centres.

A unit holder is required to enclose a clear photocopy of his/ her NRIC, Passport or Birth Certificate if he/she wishes to update his/her Name, Old/ New NRIC Number and Birth Certificate Number. For other amendments, photocopies of the above mentioned documents are not required.

Yes. A unit holder is required to complete the Unit Holder Record Maintenance Form and witnessed by any MIMMB staff.

For change of signature(s) in the case of joint account, both holders must sign the Unit Holder Record Maintenance Form and witnessed by any MIMMB staff.

Yes. Both holders must sign for a request to change the Authority to operate an account by completing the Unit Holder Record Maintenance Form.

A unit holder may complete the Unit Holder Record Maintenance Form and submit the form to any MIMMB branch offices or service centres.

Yes. However, only the Principal Holder may request for change of the beneficiary(s) by submitting a Unit Holder Record Maintenance Form to any MIMMB branch offices or service centres.

Maybank

The Autodebit Form must be completed and duly signed by the Bank Account Holder(s). The signature(s) on the Autodebit Form must be the same as the specimen signature(s) in the Bank's record.

A copy of the Bank Passbook / Statement to be enclosed for verification.

Yes. However, a unit holder may only submit to Autodebit Centre, Maybank Head Office.

Investors are advised to read and understand the Master Prospectus and the respective Product Highlights Sheet(s) for minimum transaction units / amount and the minimum holding of the fund.

The effective date is on the 28th day of each month. If the 28th of the month falls on a non-business day, the price will be based on the valuation determined at the end of the next Bursa Malaysia business day.

The Autodebit payment will be processed on the following Business day after the Autodebit effective date.

Yes. RM1.00 per transaction will be deducted from the unit holder's account for total deduction below RM500.00.

A unit holder may request to increase, decrease, change funds or cancel Autodebit by submitting the "Regular Investment Amendment (RIA) Form" or a Letter of consent to either MIMMB or Autodebit Centre, Maybank Head Office at least 14 business days before the next investment due date.

Suitability Assessment Form (SA) is not required for a unit holder who wishes to change existing instruction to invest into existing funds. However, in the event the unit holder wishes to change existing instruction to invest into new funds, then Suitability Assessment Form (SA) is required if he/ she has not completed one before.

However, the Fund Manager reserves the right to terminate your Autodebit request for payments that are unsuccessful for three (3) consecutive months.

The unit holder may contact Autodebit Centre, Maybank Head Office at 03-2070 8833 ext. 4632/ 3343 or MIMMB Customer Service Hotline at 03-2719 9271 or visit any MIMMB branch offices.

No.

No.

No.

A minimum charge of RM1.50 will be imposed if your FPX investment amount in total is below RM500.00. No charges will be levied if your FPX investment amount in total is RM500.00 and above.

The FPX direct debit service will commence 21 business days from the submission date of forms to the beneficiary bank.

The standard transaction date available for the FPX Service will be either on the 10th or 28th of each calendar month.

If the deduction date falls on a non-business day, the units credited will be calculated at the end of the following business day.

Yes, you are advised to inform MIMMB in writing or submitting the "Regular Investment Amendment (RIA) Form" at least 14 business days before the next investment due date, in the event you wish to increase, decrease, cancel the regular investment amount.

Suitability Assessment Form (SA) is not required for a unit holder who wishes to change existing instruction to invest into existing funds. However, in the event the unit holder wishes to change existing instruction to invest into new funds, then Suitability Assessment Form (SA) is required if he/ she has not completed one before.

However, the Fund Manager reserves the right to terminate your FPX request for payments that are unsuccessful for three (3) consecutive months.

No, you only need to submit one (1) duly signed FPX Application Form together with the 'FPX Deduction for Multiple Unitholders' Accounts Form’ (FPX-M).

The preferred bank account type is Current Account as the unit holder's signature can be verified online.

Yes, provided that you present yourself at the bank for verification of signature. No representative is allowed.

The participating banks are:

| No. | Bank Abbreviation | Bank Name | |

| 1. | ABB | Affin Bank Berhad | |

| 2. | ARM | Al Rajhi Banking & Investment Corporation | |

| 3. | ABMB | Alliance Bank Malaysian Berhad | |

| 4. | AMBB | AmBank Malaysia Berhad | |

| 5. | BIMB | Bank Islam Malaysia Berhad | |

| 6. | BKRM | Bank Kerjasama Rakyat Malaysia B2C | |

| 7. | BMMB | Bank Muamalat Malaysia Berhad | |

| 8. | BOFA | Bank of America (M) Berhad | |

| 9. | BOCM | Bank Of China ( Malaysia) Berhad | |

| 10. | BTMU | Bank of Tokyo (MUFG) | |

| 11. | AGRO | Bank Pertanian (Agrobank) | |

| 12. | BNPP | BNP Paribas | |

| 13. | CIMB | CIMB Bank Berhad | |

| 14. | CITI | Citibank Berhad | |

| 15. | DBB | Deutsche Bank (Malaysia) Berhad | |

| 16. | HLBB | Hong Leong Bank Berhad | |

| 17. | HSBC | HSBC Bank Berhad FPX | |

| 18. | ICBC | Industrial and Commercial Bank of China | |

| 19. | JPMC | J.P Morgan Chase Bank | |

| 20. | MBB | Malayan Banking Berhad | |

| 21. | MCBM | Mizuho Bank (Malaysia) Berhad | |

| 22. | OCBC | OCBC Bank Malaysia Berhad | |

| 23. | PBB | Public Bank Berhad | |

| 24. | RHB | RHB Bank Berhad | |

| 25. | SCB | Standard Chartered Bank Malaysia Berhad | |

| 26. | SMBC | Sumitomo Mitsui Banking Corporation Malaysia Berhad | |

| 27. | UOB | United Overseas Bank |

No, the unit holder can only cancel his/ her FPX standing instruction via MIMMB in writing at least 14 business days before the next investment due date.

The other Joint Holder (either primary or joint holder) have full authority over the account.

No, the account will remain active.

The Court orders or probate are only applicable to single-name accounts. For joint accounts, if one holder passes away, the surviving holder can take any action on the account.

PRS is a voluntary scheme designed to facilitate the accumulation of retirement savings by individuals for their retirement needs. The fund options under a PRS are intended to enhance long-term returns for members within a regulated framework. Assets of each PRS are segregated from the PRS Providers and held by an independent Scheme Trustee under a trust.

There are 2 contribution options available for members to choose from.

i.e., the Default Option and Self Selection Option.

Manulife PRS offers both Core and Non-Core Funds as investment selection which you can choose to invest based on your retirement needs, goals and risk appetite.

Core Funds

Core Funds consists of Manulife PRS NESTEGG Series and Manulife Shariah PRS NESTEGG Series. Under Default Option, these are the funds eligible that meet the requirement specified in Securities Commission Malaysia (SC) – Guidelines on Private Retirement Scheme. The fund selection is determined by the member’s age.

**The age group is subject to changes as amended by the relevant authorities from time to time.

Manulife PRS NESTEGG Series

Core - Growth

Core - Moderate

Core - Conservative

Manulife Shariah NESTEGG Series

Core - Growth

Core - Moderate

Core - Conservative

Members who selected Default Option will not be eligible to purchase Non-Core funds. To purchase Non-Core Funds, members must select Self Selection Option.

Non-Core funds consists of:

**For members who contributed into non-core funds is entitled for Free Insurance/ Takaful Coverage, Terms and Condition applies. You are advised to read and understand the relevant Disclosure Documents and Product Highlights Sheet of the respective PRS funds. If in doubt, please consult our PRS licensed consultants or contact our Customer Service at 03-2719 9271 or email to PRSinfo_MY@manulife.com

If you are 18 years old and above.

Individuals:

Employers: Employer contributes for Employees (Entity eligible up to 7% above EPF statutory rate for Tax Deduction on contributions to PRS made on behalf of employees).

PRS only allows individual accounts. Therefore, no joint accounts are allowed.

The PRS is a supplementary form of retirement savings in addition to the EPF. It is voluntary in nature. Members are not permitted by law to withdraw from EPF to contribute to the PRS.

Contributions to any fund(s) under the PRS will be maintained in two separate sub-accounts by the PRS Providers as follows:

Individual

You may obtain a tax relief of up to RM3,000 every year for your contributions made to PRS. The 10-year PRS tax incentive was supposed to end in 2021 will be extended until the year 2030 assessment. You can claim your individual tax relief based on gross amount invested. Keep the contribution statements to support the claim for tax relief as proof of contributions made for the year of assessment.

Employer

Employers that contribute to PRS on behalf of their employees are eligible up to 7% above EPF statutory rate for Tax Deduction.

For more information, you can visit the PPA website at www.ppa.my

You may withdraw only from sub-account B, once a year after one year from the date of your first contribution. However, each withdrawal will incur 8% tax penalty based on your sum of withdrawal. The tax penalty is imposed by the tax authority to discourage contributors from withdrawing as the objective of PRS is to accumulate additional savings for retirement.

There are certain Pre-withdrawal conditions that are waived from Tax Penalty (Implemented in year 2020) such as:

You can check your PRS account holdings through Manulife online portal at www.manulifeim.com.my or the PPA website at www.ppa.my

Now you can login to Manulife iFUNDS Login to check current account holding. PRS Statements is available to download online effective 25th Feb 2021 onwards.

For Individual, payment source is compulsory from own asset account to own Manulife PRS Account

Employer can perform contribution on behalf of employees

Returns of PRS funds are not guaranteed and it does not have any statutory minimum dividend policy. You are advised to read and understand the relevant Disclosure Documents and Product Highlights Sheet of the respective PRS funds. If in doubt, please consult our PRS licensed consultants or contact our Customer Service at 03-2719 9271 or email to PRSinfo_MY@manulife.com

When you invest in PRS funds, you stand to benefit from a diversified portfolio of assets with just a minimal contribution amount. In addition, the overall risk is also minimized due to diversification within the fund. This would otherwise not be possible if you invest directly in the stock market.

You may also stand to benefit from ringgit cost averaging by investing in a disciplined manner over the long-term period since the full contribution can only be withdrawn upon reaching retirement. With this method, you would not be affected as much by the market timing factor.

Although the underlying risks of investing in PRS funds may be higher, the overall risk position is minimized through its diversified portfolio.

Kindly take note that past performance is not indicative of future performance. You are advised to read and understand the relevant Disclosure Document and Product Highlights Sheet of respective PRS funds. If in doubt, please consult your PRS Licensed Consultant.

PRS is regulated under a framework developed by the Securities Commission Malaysia. The PRS forms the 3rd pillar of Malaysia’s multi pillar pension framework and the right enabling environment is crucial for its success.

PPA is a body approved by Securities Commission Malaysia to oversee and promote the growth of the industry, create general awareness, and educate the public on PRS as well as protect your interest as a contributor.

Each PRS Scheme is required to appoint an approved PRS scheme trustee to actively monitor the operation and management of the fund as well as to safeguard the assets of the Fund and act in the best interest of the members. The scheme trustee has fiduciary duty to ensure that the PRS providers comply with the scheme’s deed and disclosure document. In addition, the PRS Scheme trustee provides custodianship of the PRS fund’s assets.

Manulife is a leading Global Pension Funds Provider with more than 76 years of experience in managing pension funds globally. For more than 50 years, Malaysians have looked to Manulife for strong, reliable, trustworthy, and forward-thinking solutions to their financial needs. Manulife not only has experience in handling investment needs in Malaysia but also has locally based investment professionals in Canada, Hong Kong, China, Indonesia, Japan, Philippines, Singapore, Thailand, Taiwan, United Kingdom, United States, Vietnam, Australia, Uruguay, Brazil, and New Zealand. This gives us an advantage in terms of extensive local knowledge and exceptional financial expertise.

Manulife Private Retirement Scheme offers various Conventional and Shariah funds for you to invest according to your retirement objective, goals, and risk appetite.

Open a PRS account only takes a few minutes by access into Manulife iFUNDS Login https://client.asia.manulifeam.com/en_MY/login

All you need is your identity documents.

Speak to our PRS Licensed Consultant or contact our Customer Service at 03-2719 9271 or email to PRSinfo_MY@manulife.com

For investors who totally New in PRS industry will be charged with 1-time off PPA Account Opening Fee RM10. PPA Account Opening Fee is charged only once in a lifetime.

(* For year 2021, PPA Account Opening Fee RM 10.00 is waived until further notice.)

For existing investors in PRS industry who open account with Manulife, no PPA charges will be applied.

PPA Annual Fee RM 8 will be charged once a year. PPA will charge on members’ 1st transaction of the year for each provider.

* PPA charges are subject to any other circumstances as may be specified by the Administrator. The note is added to accommodate any changes / waiver in PPA fees as the PPA may from time to time decide.

Class C Units are a class of units introduced for the private retirement scheme funds of the MANULIFE PRS NESTEGG SERIES & MANULIFE PRS SHARIAH NESTEGG SERIES which is a private retirement scheme operated by Manulife Investment Management (M) Berhad (“the Provider”).

For the salient features of Class C Units, kindly refer relevant Disclosure Documents and Product Highlights Sheet of the respective PRS funds. If in doubt, please consult our PRS licensed consultants or contact our customer service.

a. The Scheme will be able to grow its net asset value through the injection of additional or new contributions from Members or potential members, and the Scheme will be able to invest in more instruments within the permitted investments of the Scheme;

b. Members who are currently contributing to Class A Units will be able to switch to Class C Units, subject to a switching fee of 3.00%* of the amount switched, to enjoy a lower management fee via Class C Units as compared to the management fee of Class A Units; and

c. Members will be able to redeem their contributions in Class C Units without any Redemption Charge.

You are advised to read and understand the relevant Disclosure Documents and Product Highlights Sheet of the respective PRS funds. If in doubt, please consult our PRS licensed consultants or our customer service.

You can purchase Class C Units through our:

The launching price of Class C Units on 28 April 2016 is based on the last available price of Class A Units.

RM100 or such other amount as the Provider may decide from time to time.

RM100 or such other amount as the Provider may decide from time to time.

No, all classes of Units in each of the Funds of the Scheme are managed under one account.

Switching from Class A Units to Class C Units is permitted and a switching fee of 3.00%* of the amount switched out will be imposed by the Provider on the Member.

For Class C Units, however, switching of Units can only be done within the same class of units. Members are not permitted to switch their vested Units and/or conditionally vested Units from Class C Units to Class A Units.

Class A Units

No switching fee will be imposed on the first 12 switching transactions made during a Calendar Year between the Funds of the Scheme or between a Fund of the Scheme and any other fund in another private retirement scheme operated by the Provider.

A switching fee of RM25.00* will be imposed by the Provider on the Member for each subsequent switching transaction made within the same class of Units during the same Calendar Year.

For each subsequent switching transaction made from Class A or Class B Units to Class C Units during the same Calendar Year, a switching fee of 3.00%* of the amount switched out will be imposed by the Provider on the Member.

The Provider may, at its discretion, waive the switching fee based on the terms and conditions as may be determined from time to time.

Class C Units

No switching fee will be imposed on the first 12 switching transactions made during a Calendar Year: (1) between the Funds of the Scheme within the same class of Units; or (2) between a Fund of the Scheme and any other fund in another private retirement scheme operated by the Provider within the same class of Units.

A switching fee of RM25.00* will be imposed by the Provider on the Member for each subsequent switching transaction made within the same class of Units during the same Calendar Year.

The Provider may, at its discretion, waive the switching fee based on the terms and conditions as may be determined from time to time.

Yes, he may do so. However, a sales charge of 3.00% of NAV per unit will be imposed.

Yes.

a) Paper Flow: Investor required to submit Account Opening Form for New customers and Additional Contribution Form for existing customers with percentage written on desired fund with total Contribution Amount and payment proof of contribution made to Manulife Investment Management (M) Berhad - Client Trust Account.

b) Electronic Platform-Manulife iFUNDS: Investor only required to perform account opening /additional contribution selection and make payment online via FPX. No paper submission is required.

A new Member has to complete the transfer form provided by the Private Pension Administrator ("PPA") and the Provider’s private retirement scheme Joint Account Opening Form. Existing Members need to complete the PPA transfer form if they wish to transfer their contributions from another private retirement scheme provider.

PRS NON-CORE FUNDS

The Fund suitable for investors who seek investment exposure mainly through diversified portfolio of REITs within Asia-Pacific Region, long-term capital growth, seek sustainable distribution of units, seek an additional retirement saving scheme other than mandatory retirement scheme.

The Fund aims to provide long-term capital appreciation and sustainable income by investing in one collective investment scheme which mainly invests in REITS.

The Fund also suitable for Employers who wish to contribute on behalf of their employees having the aforesaid characteristics.

You are advised to read and understand the relevant Disclosure Documents and Product Highlights Sheet of the respective PRS funds. If in doubt, please consult our PRS licensed consultants.

The Fund suitable for investors who seek to invest in Shariah-compliant investment and investment exposure mainly through diversified portfolio of REITs globally, seek sustainable distribution of units and potential capital growth on investors contributions over medium to long-term (between 3 to 5 years), additional retirement saving scheme other than mandatory retirement scheme.

The Fund aims to provide regular income and capital appreciation by investing in one Islamic collective investment scheme which invest mainly in Islamic REITS.

The Fund also suitable for Employers who wish to contribute on behalf of their employees having the aforesaid characteristics.

You are advised to read and understand the relevant Disclosure Documents and Product Highlights Sheet of the respective PRS funds. If in doubt, please consult our PRS licensed consultants.

The Fund is suitable for Members who:

The Fund aims to achieve capital appreciation by investing in a portfolio of Islamic collective investment schemes. The Fund will invest a minimum of 95% of the Fund’s NAV in a portfolio of Islamic CIS that aims to provide capital appreciation through exposure into China and India markets. The remaining NAV of the Fund will be invested in Islamic liquid assets such as cash, Islamic money market instruments, general investment accounts and/or Islamic deposits with financial institutions for liquidity purposes.

You are advised to read and understand the relevant Disclosure Documents and Product Highlights Sheet of the respective PRS funds. If in doubt, please consult our PRS licensed consultants.

*the rate and amount disclosed are exclusive of any goods and services tax.

![]()

©1999 - 2026 Manulife Investment Management (M) Berhad (Registration No. 200801033087 (834424-U))