We are halfway through 2022 – six months of what would likely go down in history as one of the most excruciating downturns in financial markets. Investors across almost all asset classes were pummelled and whiplashed by shifting markets, brought about by a lethal combination of soaring inflation, aggressive monetary policy tightening and geopolitical conflicts, which came right on the heels of a global pandemic. In this Investment Note, we examine how the Malaysian financial market has fared in the bigger scheme of things and the outlook of the market for 2H 2022.

Equity market

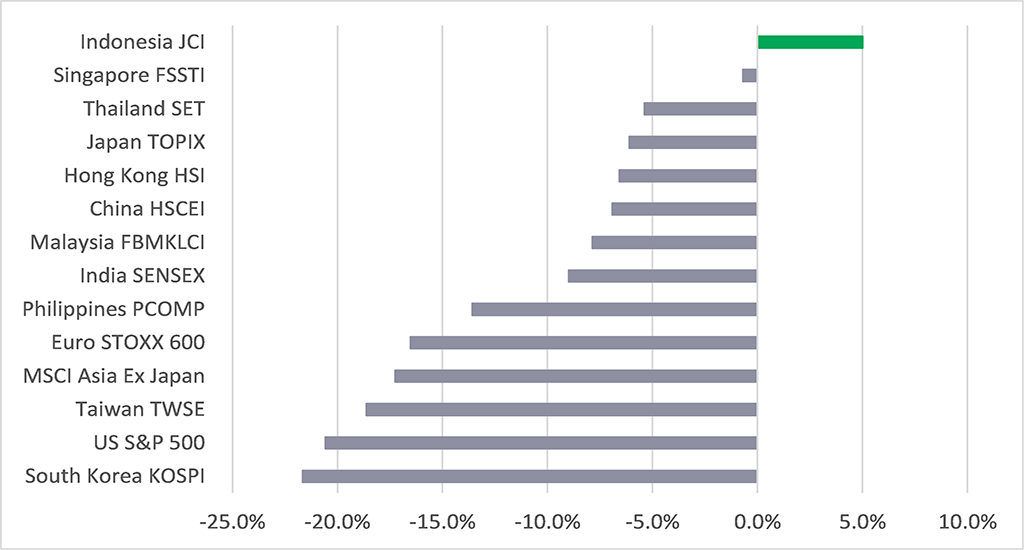

Chart 1: Performances of major stock indices (%) year-to-date (YTD) 30 June 2022

Source: Bloomberg, Manulife Investment Management, as of 30 June 2022. Past performances are not an indication of future performances.

Up till the end of May 2022, the local bourse had demonstrated remarkably resilient performance, eking out a positive return amid the sea of red in global equity markets. The Malaysia equity market was propped up by commodity-related stocks in the plantation and energy sectors as well as banking stocks. The former a beneficiary of the elevated commodity prices while the latter tend to perform well in a rising rate environment.

Alas, performance tumbled in June 2022 as inflation fear morphed into recession fear; FBM KLCI posted a return of -7.9% YTD 30 June 2022. Given the multi-decade high inflation rates and exceptionally low real interest rates across most parts of the world, it is little wonder that rate hike trajectory has shifted a gear higher. With the exception of the Bank of Japan and People’s Bank of China, central banks are making it clear that they will do whatever it takes to tame inflation, perhaps even to the extent of “tolerating” recessions.

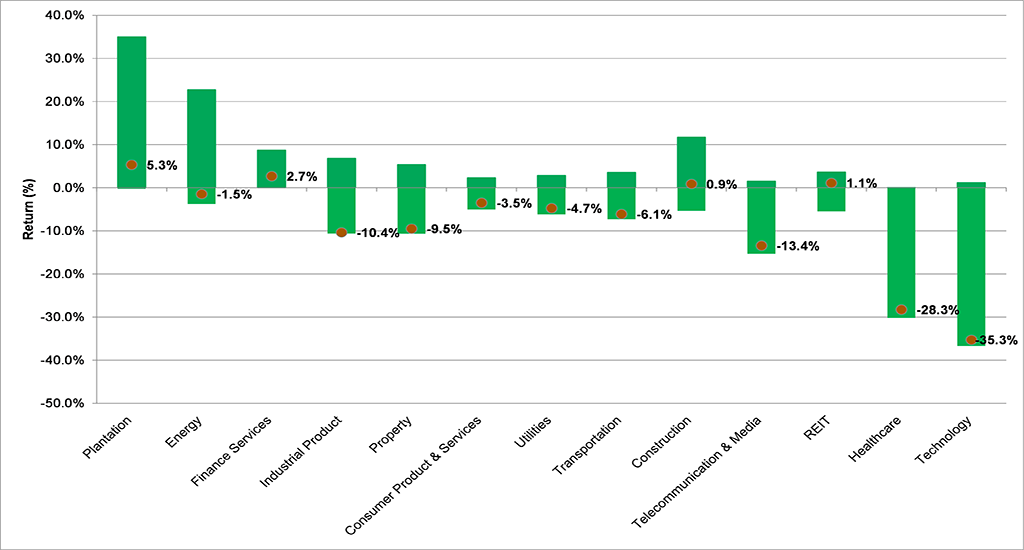

The increasingly “realistic” prospects of a recession bit into financial markets, turning sentiment risk-off. The entire commodity complex was also affected; global commodities experienced cumulative losses of more than 10% in the last two weeks of June, marking the sharpest decline since March 2020. As observed in Chart 2, plantation sector remained the best performing sector despite the large drop in stock prices following the commodities selloff in June. The other sectors which were still in the black were financial services and real estate investment trusts.

The worst performing sector was technology – understandably so since tech-based, growth stocks bore the brunt of devaluation as interest rate rose. Healthcare sector also languished due to the dismal performances of glove stocks as the world slowly moved on from pandemic SOPs and restrictions.

Chart 2: Performances of sectors in Malaysia stock market – YTD range and as of 30 June 2022

Source: Bloomberg, Manulife Investment Management, as of 30 June 2022. Past performances are not an indication of future performances.

What then are the prospects for the second half of the year? We expect 2H 2022 to be equally if not more challenging than the first half of the year given higher risks of growth slowdown and persistent inflationary pressure. Short-term volatility is expected to be the flavour of the day though we think the local equity market remains supported by the following factors:

All things considered, the growth outlook for the Malaysian economy is strong – gross domestic product (GDP) growth for 2022 is forecasted at 5.3% – 6.3%, compared to last year’s low growth rate of +3.1%

Malaysian equity market has always been known for its stability and defensiveness, particularly during volatile periods. Based on the factors highlighted in the previous section, Malaysian equity is likely a suitable market to ride through the challenging macro environment.

We have increased exposure in the commodity space since the beginning of the year to take advantage of the soaring commodity prices. This tilt was well received in our portfolio, contributing to the bulk of many of our funds’ outperformance in Q1 2022.

We have also added exposures to stocks that benefit from a rising interest rate environment. Most central banks around the globe are expected to lift rates this year – Malaysia is no exception. In its latest meeting on the 11 May 2022, Bank Negara Malaysia (BNM) announced an earlier-than-expected 25 basis points (bps) interest rate hike.

Hence, we will continue to pivot over into recovery stocks, targeting to reduce portfolio volatility, favouring the financials, commodities and utilities sectors. Nevertheless, we are still maintaining a selective exposure on technology stocks that are growing and remain long-term structural winners. These stocks will aid us to sustain our performance once the market rebounds.

This market sell down presented us with a myriad of opportunities to cherry pick stocks identified for longer-term investments at a good entry price. At the same time, we continue to maintain a well-balanced portfolio which we believe is essential in navigating today’s highly volatile market. Staying patient and focused would help to navigate this down trending market.

Fixed income market

After a brutal year in 2021, bond markets were devastated yet again in 2022 as rise in bond yields turned meteoric in the second quarter. Malaysian Government Securities (MGS) yield movements essentially mirrored what happened in the US Treasury market and most bond markets worldwide. Economic rebound as the world stepped out of the pandemic meant interest rate hike, which naturally translated into higher bond yield.

What was deemed “transitory” inflation in developed markets for most 2021 became a fearsome “inflation monster” that has to be vanquished by all means in 2022. Central banks, particularly US Federal Reserve signalled aggressive monetary tightening and signalled willingness to do “whatever it takes” to control inflation, even at the expense of growth.

Although the fundamentals in Malaysia does not warrant such a drastic yield increase – domestic GDP growth is still expected to be strong and inflation level remains manageable – it is difficult to rise above the global bearish sentiment for bond market.

We are neutral on the overall outlook of MGS. In the short-term, we are wary on risks stemming from inflationary pressure and funds outflow. Despite manageable domestic inflation level at this juncture, it remains to be seen whether global food and energy inflation will find its way into the local economy to apply price pressure. Meanwhile, receding global liquidity amid the commencement of quantitative tightening in the US and geopolitical risks are likely to continue causing market volatility and possible funds outflow from Emerging Market, including Malaysia.

In the longer term, however, we are more optimistic on the outlook of MGS. Most parts of the yield curve has priced in a full normalisation of the overnight policy rate (OPR) to 3.00% and current demand-supply dynamics. We believe prospects for MGS investments will brighten once external development stabilises and rate fears recede. From a different perspective, the rise in bond yields also serve as a timely correction for the bond market – a painful but sure solution to the “low for longer” conundrum we were facing just two years ago.

We maintained a defensive portfolio for our fixed income funds for most of 2021 and 1H 2022, with higher cash level and shorter portfolio duration. We have gradually lengthened portfolio duration recently after yields have realigned higher.

Chart 3: MGS yield, UST yield and OPR (1 January 2017 – 30 June 2022)

Source: Bloomberg, Manulife Investment Management, as of 30 June 2022. Past performances are not an indication of future performances.

Going forward, we will be adopting active tactical strategies in the management of our funds, particularly within the government and corporate bond space, while maintaining reasonable fund liquidity. We are maintaining a flexible approach in adjusting our duration when necessary, in view of market volatility and the myriad of geopolitical/events risks.

We believe that income return will be the primary contributor towards our fixed income portfolio returns and have positioned our investment portfolio to leverage on corporate bonds for yield enhancement. This move would also provide us with better price stability as any upward movement in rates would be buffered by credit spreads.

1Source: CGS-CIMB, as of 31 May 2022

2Source: MIDF Research, as of 17 June 2022

2026 Outlook: Clearer picture, better growth

This year’s outlook spotlights a world in flux – U.S. stimulus, Europe’s rebound, China’s policy pivots, and Japan’s innovation surge all shape a landscape full of both opportunities and challenges.

2026 Asian Fixed Income Outlook: Positive momentum poised to continue amid ample investment opportunities

Asian fixed income posted strong gains in 2025 amid myriad challenges. Entering the new year, the asset class is poised for continued momentum on the back of numerous beneficial tailwinds. In this 2026 Outlook, the Asian Fixed Income team analyses the key factors likely to propel performance and identifies opportunities for investors based on key themes and developments in three regional bond markets: China, Japan, and India.

2026 Global Macroeconomic Outlook: clearer picture, better growth

Our 2026 macro outlook highlights key themes across global economies and commodities, what we'll be watching closely in the new year, and portfolio takeaways for investors to consider.

2026 Outlook: Clearer picture, better growth

This year’s outlook spotlights a world in flux – U.S. stimulus, Europe’s rebound, China’s policy pivots, and Japan’s innovation surge all shape a landscape full of both opportunities and challenges.

2026 Asian Fixed Income Outlook: Positive momentum poised to continue amid ample investment opportunities

Asian fixed income posted strong gains in 2025 amid myriad challenges. Entering the new year, the asset class is poised for continued momentum on the back of numerous beneficial tailwinds. In this 2026 Outlook, the Asian Fixed Income team analyses the key factors likely to propel performance and identifies opportunities for investors based on key themes and developments in three regional bond markets: China, Japan, and India.

2026 Global Macroeconomic Outlook: clearer picture, better growth

Our 2026 macro outlook highlights key themes across global economies and commodities, what we'll be watching closely in the new year, and portfolio takeaways for investors to consider.

![]()

©1999 - 2026 Manulife Investment Management (M) Berhad (Registration No. 200801033087 (834424-U))