Year 2025 saw the return of Trump's 'America First' trade policy aimed at addressing persistent trade deficits and perceived unfair trade practices. This policy targeted regions where the US has significant trade deficits, starting with Canada, Mexico, and China. On February 1, President Trump made his first major trade move by imposing a 25% tariff on all imports from Canada and Mexico, along with an additional 10% tariff on Chinese goods. In retaliation, China and Canada implemented countermeasures, prompting the US to extend tariffs to more goods and markets, setting off a cycle of reciprocal tariffs and further retaliation.

Tensions escalated on April 2, a day President Trump dubbed "Liberation Day," when he announced plans for reciprocal tariffs on all trading partners, ranging from 10% to 50%. Fortunately, a 90-day pause was later declared for these tariffs, with the exception of those on China. This pause allowed for negotiations between the US and its trading partners, providing short-term relief to the impacted parties.

Focusing on US-China trade relations, after several rounds of tit-for-tat measures, US tariffs on Chinese goods soared to 145%, while Chinese tariffs on American goods climbed to 125%. This escalation marked a significant deterioration in trade relations between the world's two largest economies, amplifying fears of global supply chain disruptions, a potential trade war, and a slowdown in global economic growth.

Beyond political developments, the launch of China's low-cost AI model, DeepSeek, made headlines earlier in the year. Its success signifies not only a technological shift but also a broader challenge to Western dominance in AI research and development. The impact of DeepSeek was profound, with US tech giant NVIDIA experiencing a staggering $600 billion market value loss in a single day—the largest single-day loss in US stock market history. This development intensified tech rivalry between the US and China, as the prospect of China gaining a significant foothold in this critical sector fuelled existing tensions. Consequently, most stock market indexes faced downward pressure, with the MSCI World Index falling by 2.1% in the first quarter of 2025. In response to market volatility, investors sought refuge in safer assets, driving up gold prices by over 19% during the same period.

The Johor-Singapore Special Economic Zone (JS-SEZ) agreement was inked in 1Q 2025 to enhance cross-border connectivity, facilitate the movement of workers and tourists, and strengthen business ecosystems, with special tax incentives introduced to attract investments. Additionally, Malaysia forged a pact with British chip designer Arm Holdings, securing a USD250mil investment over 10 years for intellectual property access. This move aims to bolster Malaysia's role in the upstream semiconductor supply chain and transition into high-tech industries.

In 2024, Malaysia experienced a record RM378.5bil in approved investments1, boosting the construction, manufacturing, and services sectors. Consequently, GDP growth exceeded expectations, achieving 5% in Q4 2024 and a full-year growth of 5.1%, driven by strong domestic demand and a recovery in exports. Throughout the year, headline inflation remained stable below 2%, reflecting steady cost and demand conditions, leading BNM to keep interest rates unchanged at 3.00%, while reiterating that future decisions will remain data-dependent.

Equity market

In Q1 2025, global equities faced a challenging start with President Trump returning to office. Most developed markets began the year on a positive note, buoyed by signs of US economic strength, as the 4Q 2024 GDP grew robustly at 2.4%. Trump's pledges for deregulation and tax cuts further bolstered developed market equities. However, the landscape shifted dramatically with DeepSeek's breakthrough in creating efficient, low-cost AI models, triggering a major sell-off in US tech stocks. This development led to a $1 trillion loss in market value for US and European technology stocks, with the Nasdaq 100 dropping as much as 3.6% in a single day. Conversely, emerging markets struggled, particularly after the US announced controls on advanced chip exports. This move prompted a "sell first" approach in the market, exacerbating declines in emerging market equities.

In February, markets were rattled further by Trump's decision to impose tariffs on Canada, Mexico, and China. As more regions were added to the list, retaliatory and reciprocal tariffs were announced, escalating trade conflicts. These measures negatively impacted investor and corporate sentiment, as well as growth expectations, contributing to a decline in most major stock indices in Q1 2025.

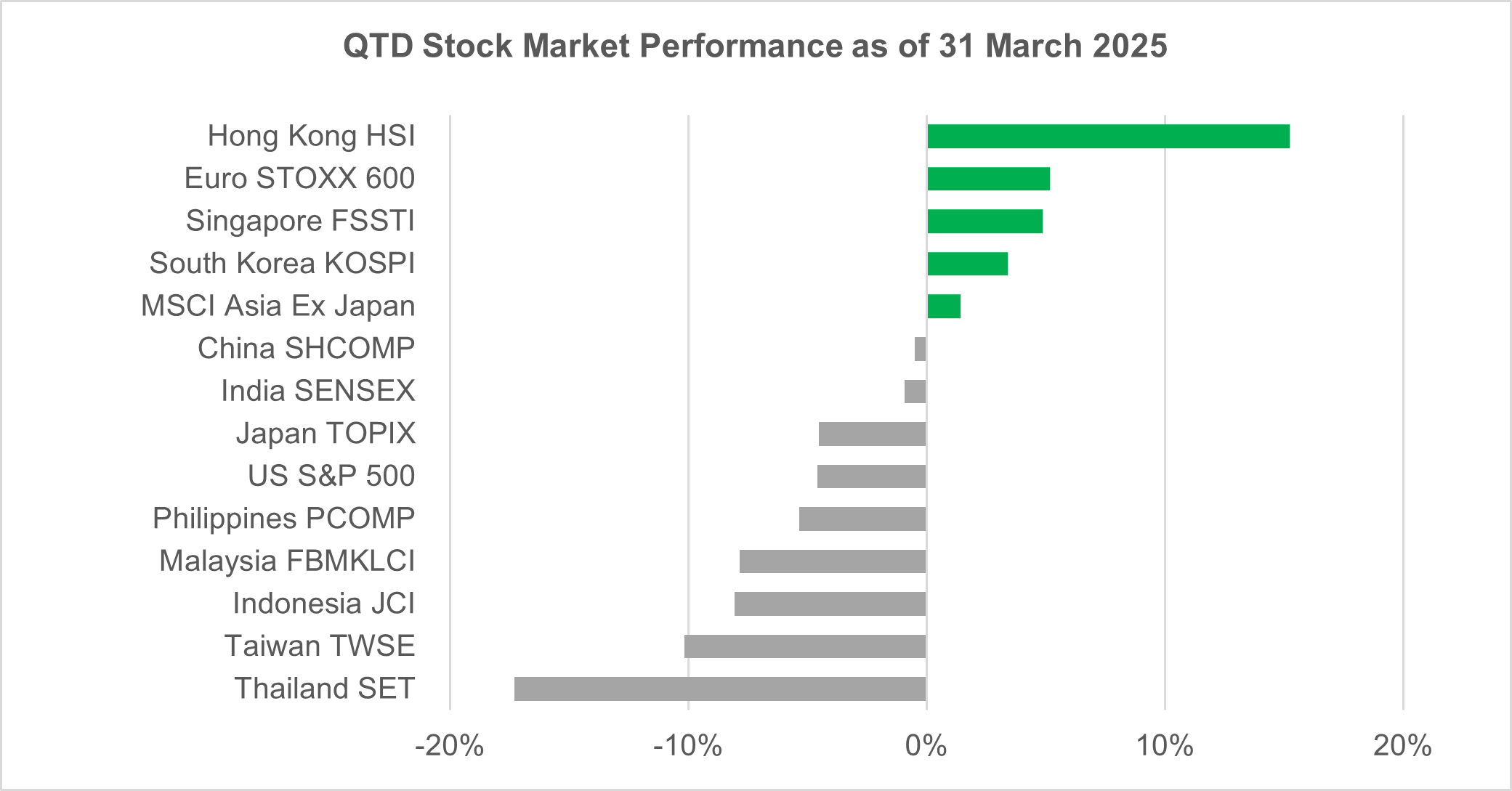

By the end of the quarter, most stock indices were in the red. However, Hong Kong's Hang Seng Index stood out as the region's top performer, achieving a 15.3% QoQ return, driven by excitement about the implications of DeepSeek, which contributed to a broader surge in Chinese technology stocks. Europe's STOXX 600 followed closely with a 5.2% QoQ gain, supported by signs of improvement in eurozone macro data, the low weighting of technology stocks in the index, and the ECB's accommodative monetary policy stance. In contrast, Thailand's SET was the region's biggest loser, returning -17.3% QoQ due to weak investor confidence stemming from its weak economic outlook and poor corporate earnings.

In Q1 2025, Malaysia's FBM KLCI experienced a 7.8% QoQ loss, aligning with the broader trend seen in global stock indices. Market sentiment was dampened by uncertainties surrounding US tariffs, which contributed to a global risk-off environment. Sector-wide declines were notable, with each sector averaging a loss of around 10% QoQ. This was underscored by a substantial net foreign fund outflow of approximately RM10bil2 during the first quarter of 2025.

Overall, the FBM KLCI's performance was in line with the broader market, as both the FBM100 Index and the FBM Small Cap Index posted QoQ declines of 9.5% and 13.3%, respectively. However, relative to the region, the FBM KLCI underperformed the MSCI Asia ex Japan Index, which posted marginal gains of 1.4% QoQ.

Looking ahead, we have adopted a cautious stance on the local equity market's near-term outlook due to external shocks and uncertainties surrounding US tariffs. Prolonged uncertainties could elevate downside risks to growth and lead to increased market volatility as trade negotiations unfold. Consequently, the current risk-off sentiment may persist for the foreseeable future. However, several factors are poised to support the local equity market in 2025. Ongoing domestic policy reforms, attractive valuations, appealing dividends, a potential strengthening of the MYR, and a recovery in domestic consumption are likely to underpin market resilience and performance.

Source: Bloomberg, as of 31 March 2025. Past performance is not necessarily indicative of future performance.

Fixed income market

The UST had a volatile start to the quarter, experiencing a sell-off in early January after a strong jobs report reinforced expectations that interest rates would remain high for longer. This raised concerns that the 10-year yields could hit 5%, a level feared to unsettle global markets. Subsequently, yields began to fall amid expectations of slower global growth and risk-off trades driven by the threat of US tariffs. As a result, UST yields declined throughout the period, with the 2-year, 5-year, and 10-year yields decreasing by 36 bps, 43 bps, and 36 bps, respectively, closing the quarter at 3.88%, 3.95%, and 4.21%.

In Malaysia, the bond market benefitted from positive sentiment in the UST market, where yields on 3-year, 5-year, and 10-year MGS fell between 4 bps to 7 bps, ending the quarter at 3.41%, 3.57%, and 3.77%, respectively.

With a dimmer growth outlook, the doors are open for BNM to consider a potential rate cut, likely in 2H 2025. This consideration would come after BNM evaluates the economic impact observed in 2Q 2025 and the outcomes of negotiations between the US and its trading partners. We will closely monitor whether domestic spending and investments can offset weaker external demand, potentially giving rise to a slightly more positive bias on the local bond market.

1Source: Malaysian Investment Development Authority (MIDA), As of 31 December 2024

2Source: MIDF, As of 28 March 2025

2026 Outlook: Clearer picture, better growth

This year’s outlook spotlights a world in flux – U.S. stimulus, Europe’s rebound, China’s policy pivots, and Japan’s innovation surge all shape a landscape full of both opportunities and challenges.

2026 Asian Fixed Income Outlook: Positive momentum poised to continue amid ample investment opportunities

Asian fixed income posted strong gains in 2025 amid myriad challenges. Entering the new year, the asset class is poised for continued momentum on the back of numerous beneficial tailwinds. In this 2026 Outlook, the Asian Fixed Income team analyses the key factors likely to propel performance and identifies opportunities for investors based on key themes and developments in three regional bond markets: China, Japan, and India.

2026 Global Macroeconomic Outlook: clearer picture, better growth

Our 2026 macro outlook highlights key themes across global economies and commodities, what we'll be watching closely in the new year, and portfolio takeaways for investors to consider.

2026 Outlook: Clearer picture, better growth

This year’s outlook spotlights a world in flux – U.S. stimulus, Europe’s rebound, China’s policy pivots, and Japan’s innovation surge all shape a landscape full of both opportunities and challenges.

2026 Asian Fixed Income Outlook: Positive momentum poised to continue amid ample investment opportunities

Asian fixed income posted strong gains in 2025 amid myriad challenges. Entering the new year, the asset class is poised for continued momentum on the back of numerous beneficial tailwinds. In this 2026 Outlook, the Asian Fixed Income team analyses the key factors likely to propel performance and identifies opportunities for investors based on key themes and developments in three regional bond markets: China, Japan, and India.

2026 Global Macroeconomic Outlook: clearer picture, better growth

Our 2026 macro outlook highlights key themes across global economies and commodities, what we'll be watching closely in the new year, and portfolio takeaways for investors to consider.

![]()

©1999 - 2026 Manulife Investment Management (M) Berhad (Registration No. 200801033087 (834424-U))