14 March 2022

Sarah Lu, Senior Portfolio Manager, Multi-Asset Solutions Team, Asia

Geopolitical tensions are increasingly clouding the global growth outlook. Sarah Lu, Senior Portfolio Manager, Multi-Asset Solutions Team, Asia, gauges the potential impact on markets and shares her latest asset allocation view amid rising inflation and lower growth.

Russia’s invasion of Ukraine is one of the true black swan events of recent years, and the raft of sanctions imposed could certainly affect global economies. As our Global Chief Economist and Head of Macroeconomic strategy Frances Donald noted, there are three aspects we need to consider when assessing the macroeconomic impact of the recent geopolitical conflict:

Following the raft of sanctions imposed on Russia, interest rates futures immediately reflected the prospect of a lower-than-expected interest rate hike by the US Federal Reserve (Fed) in March, i.e., a 25-basis point rate rise became the consensus view1. In response, some European government bonds have rebounded.

Earlier this year, before the military conflict started, we had a slightly positive view on Europe for 2022 as it possesses multiple growth drivers. Indeed, the latest PMI readings in Europe fare well. However, given the raft of sanctions imposed2, we have started to look at Europe less positively.

At the time of writing, the Russia-Ukraine situation remains fluid. As such, here is our current base-case assessment:

The prospects for a more sustained stagflation shock, exacerbated by recent events, has seen adjustments in our asset-allocation positioning. As such, we believe that persistent volatility and more frequent bouts of risk aversion will occur in the first half of 2022. While the US is still on an above-trend growth path3 at this point amid the expected resumption of shale energy demand, we think the US dollar will continue to be supported, attracting capital inflow into US assets.

Within developed markets, US equities are favoured over their European counterparts. Versus other regions, we believe the US will be minimally impacted by sanctions against Russia. Within the US, the energy and defence industry should expect to see higher substitute demand. For example, the US will play a more important role given the ban on Russian oil exports, as it can provide shale energy in lieu of energy embargo from Russia.

Given weaker economic growth momentum, coupled with ongoing geopolitical uncertainty, we expect equity markets to experience heightened volatility. However, markets with significant exposure to energy and materials (as inflation hedges) and consumer staples (as a defensive play) may find some insulation thanks to higher commodity prices.

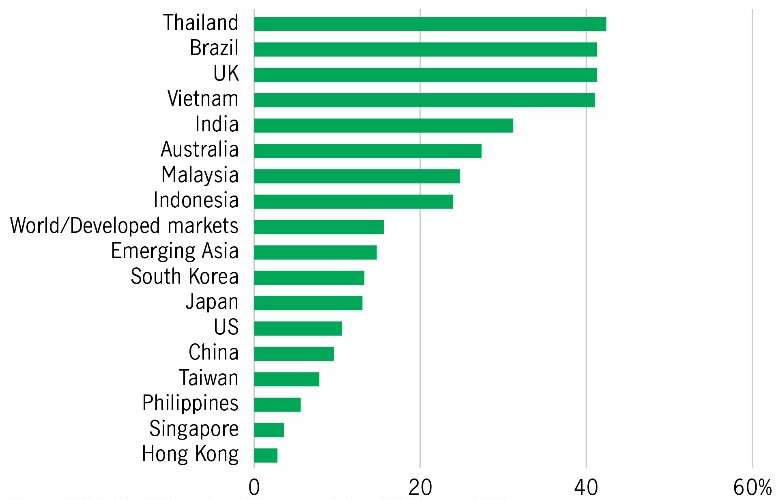

Within emerging markets, we are relatively more positive towards select Asian equities (commodity-exporting markets, such as Malaysia, Indonesia, Thailand, and the Philippines, see chart 1).

Chart 1: MSCI market exposure to materials, energy and staples

Source: MSCI, Manulife Investment Management. As of 28 February, 2022.

The prospect of aggressive rate hikes is now lower, and the Fed is expected to raise interest rates by only 25 basis points in March (50 basis points had been anticipated by the market). Also, we think that bonds look more favourable, and our overall allocation has been revised to less of an underweight.

Assuming current geopolitical events and stagflation do not lead to a severe recession, we believe the US high-yield market has the potential to deliver relatively better performance versus risk assets like equities, as it is better compensated via higher coupons under rising inflation. Also, US high yield has a lower default potential versus other regions, as these bonds have a relative greater exposure to oil and gas sectors. Although signs of financial deleveraging in the face of liquidity withdrawal by the US Fed still needs to be watched carefully.

Meanwhile, floating-rate bonds (beneficiaries of a rising rate environment), China renminbi government bonds (a stable exchange rate and higher coupon rates versus other government bonds), and preferred securities (a fixed income-like product with higher coupon rates) are also expected to be more resilient than risk assets.

Other income-generating asset classes, such as REITs, will be supported, as rate differentials (REIT yields minus government bond yields) should narrow at a slower pace than before.

We view commodities from two perspectives, both as inflation hedges and diversification tools. We expect commodity prices, such as oil and agriculture products, to remain elevated on the back of supply disruptions and geopolitical events. Commodities with inflation-hedge properties, like precious metals (gold and silver), oil, and farm products could perform better.

At the time of writing, the macro-outlook and geopolitical events are still highly fluid. The odds of slower growth and higher inflation are increasing, and we believe investors should seek active management and diversification to reshape their portfolios for an evolving investment landscape.

1 Fed Funds Futures show a 96.9% chance of a 25 basis points hike at the March Fed meeting. Upon the announcement of European Union sanctions, Germany’s 10-year government bond price rose from 97.776 on 25 February 2022 to 100.799 on 1 March 2022. Meanwhile, 10-year bond yields fell from 0.2261% to -0.0799% over the same period. 7 March 2022, Bloomberg.

2 Eurozone IHS Markit's Composite Purchasing Managers' Index climbed to a five-month high of 55.5 in February 2022. Bloomberg, 7 March 2022.On 8 March 2022, the US has banned Russian oil exports. The European Union announced a series of sanctions against Russia. These included a ban on all transactions with the Central Bank of Russia, which limits its ability to access foreign reserves. Also, seven Russian banks will be removed from the SWIFT international payments system and eurozone-based companies banned from exporting technology to Russian weapons manufacturers, pharmaceutical companies, military communications units and shipyards. Lastly, eurozone-based companies are banned from doing business with the designated state-owned companies specialising in military production. Financial Times, 4 March 2022.

3 The US economy expanded by 5.7% year-on-year in 2021, a higher- than-trend growth of 2%-3%. Bloomberg, 7 March, 2022.

Q2 2025 Malaysia Market Outlook: Trade Tensions and Market Volatility

Market Flash: Impact of US Tariffs on Malaysia

Read moreQ1 2025 Malaysia Market Outlook: Equity, Fixed Income and Economic Trends

![]()

©1999 - 2026 Manulife Investment Management (M) Berhad (Registration No. 200801033087 (834424-U))