19 April 2023

Diana Racanelli, CFA, Senior Portfolio Manager, Capital Appreciation

Craig Bethune, CFA, Senior Portfolio Manager, Capital Appreciation

Well-intentioned, climate-oriented investors are using a variety of approaches to align their capital with the future they want to see. One approach is to move capital away from today’s high emissions sectors—but ironically, it’s these same sectors that hold the key to a low-carbon future. In this article, we explore why a strategic and proactive approach might be more effective in both combating climate change and capturing value from industries leading the low-carbon transition.

We explain the four investment pillars—low-carbon energy, transition materials, electrification and efficiency, and resource security—that together can result in the biggest positive climate impact.

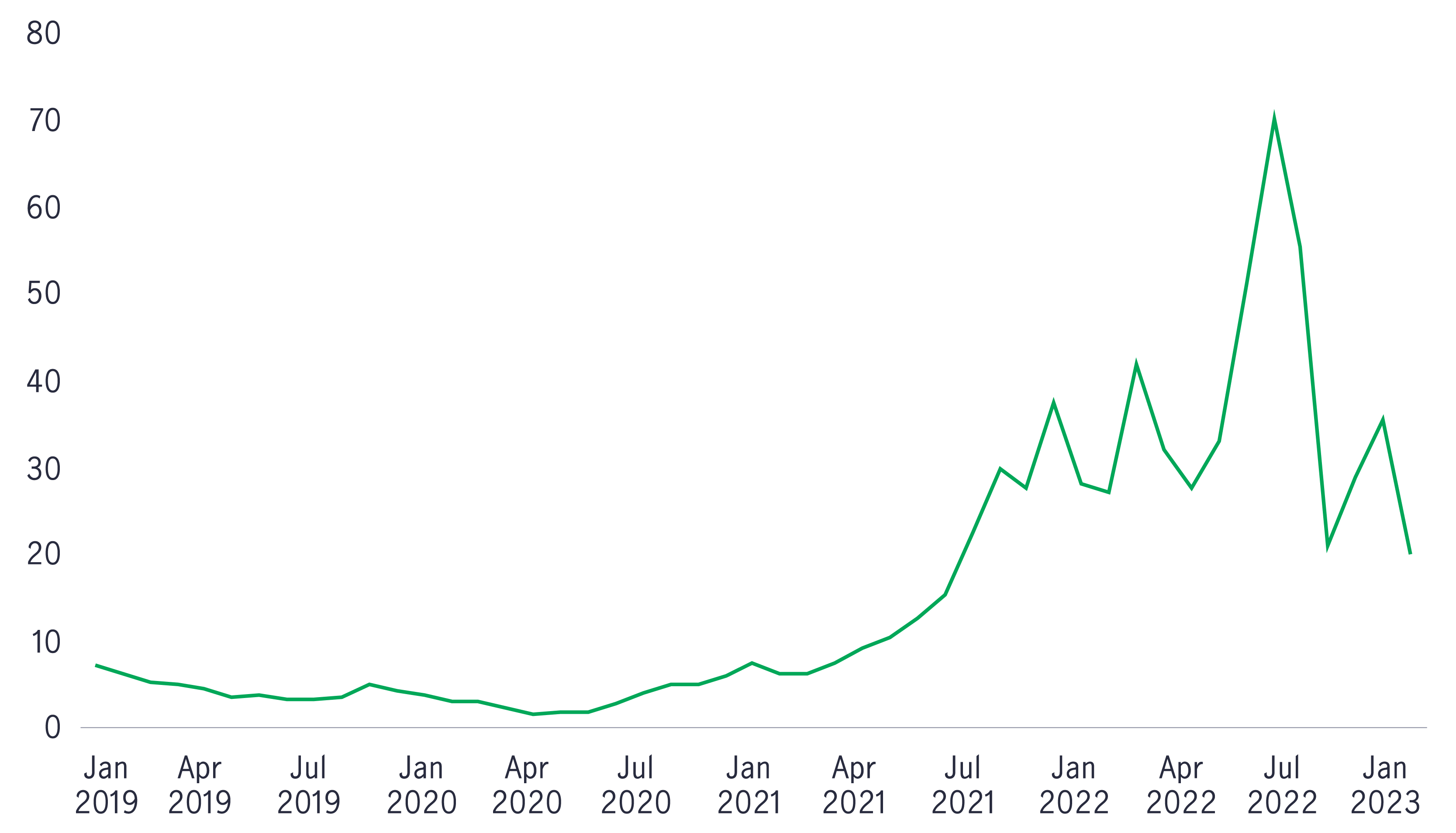

Sanctions imposed on Russia’s oil and gas exports in 2022 created historic energy shortages in Europe, putting the region’s energy security and affordability into a critical state. Fortunately, warmer-than-average winter temperatures helped build back natural gas inventories, bring prices down from record highs, and reduce the risk of a full-blown energy crisis.

Although the situation in Europe seems to have stabilized for now, this situation highlights once again our world’s dependence on fossil fuels: We’re not yet able to significantly reduce or even completely eliminate fossil fuels in the short term, and attempts to do so without clear alternatives can lead to disorderly markets. It’s important to note that Europe is an early adopter and strong advocate of sustainable energy—with about 40% of its electricity production coming from renewable energy sources—and yet was heavily affected by oil and gas supply disruptions. The reality is that transitioning to a sustainable future is complex, and fossil fuels, along with some other carbon-intensive industries such as mining, will have a role to play in it.

The Russia-Ukraine conflict has created great volatility in energy markets

Natural gas prices in the European Union (USD per million metric British thermal unit)

Source: Manulife Investment Management, FRED, as of January 2023.

Generally, climate-oriented investors avoid heavy polluters altogether through negative screening. While we understand the idea of not supporting companies that are damaging the environment, we believe that investors who focus only on low-emissions companies aren’t leveraging the opportunities that the low-carbon transition offers over US$7 trillion annually is expected to be spent to help the world decarbonize, and investors will be well served to invest in the companies providing those solutions and that are therefore on the front lines of climate change mitigation. As such, for investors to help combat climate change in the most effective way, we believe there are four key investment themes to consider:

As a society, we embarked on a massive energy shift toward renewable energy a long time ago, with hydroelectric and nuclear sources first increasing in prominence in the middle of the 20th century. Despite this, fossil fuels still represent more than 80% of the global energy supply. Ramping up renewables can’t happen overnight, but if the transition began so long ago, why do we have so little progress to show?

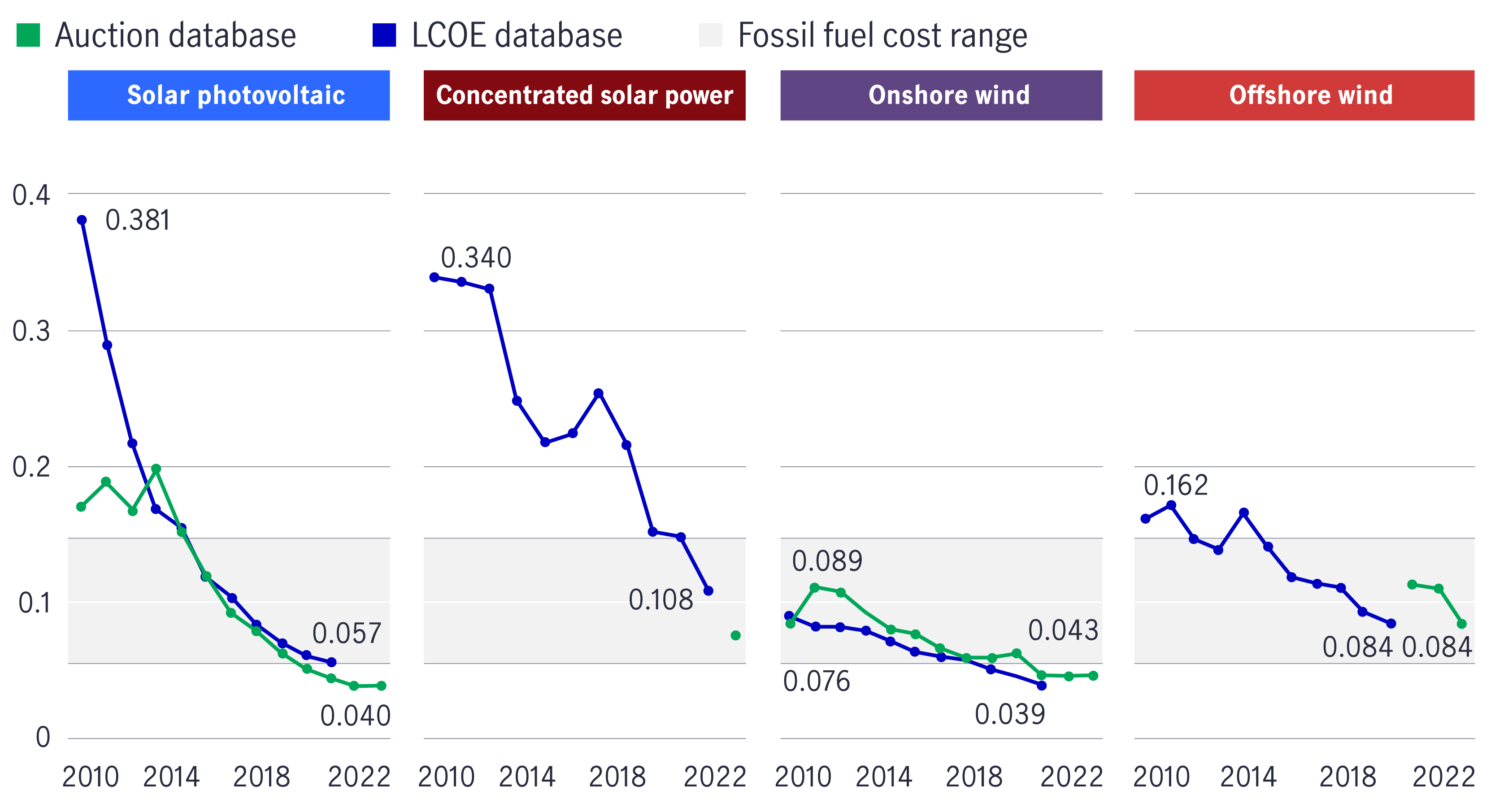

The reality is that fossil fuels are rooted in our consumption habits as a widely available, cost-effective energy source. To replace fossil fuels, we therefore need a technology that is better not only from an environmental standpoint but also from a cost perspective, while being broadly available. We believe that we’ve finally reached this point with solar and wind.

Thanks to new technologies, the global weighted average levelized cost of electricity (LCOE, or the total cost of building and operating a power plant over its lifetime divided by its energy production) for wind and solar has decreased significantly since 2010. Specifically, the LCOE from photovoltaic solar projects decreased by 85%, concentrated solar power by 68%, onshore wind by 56%, and offshore wind by 48%. In fact, it’s now even cheaper to produce electricity with wind and solar than with fossil fuels over the long term, with the main caveat being that the power from wind and solar is intermittent.

Renewables-based electricity is now a cheaper option than fossil fuels

Global weighted average levelized cost of electricity (USD/kWh)

Source: International Renewable Energy Agency, World Energy Transitions Outlook, 2022.

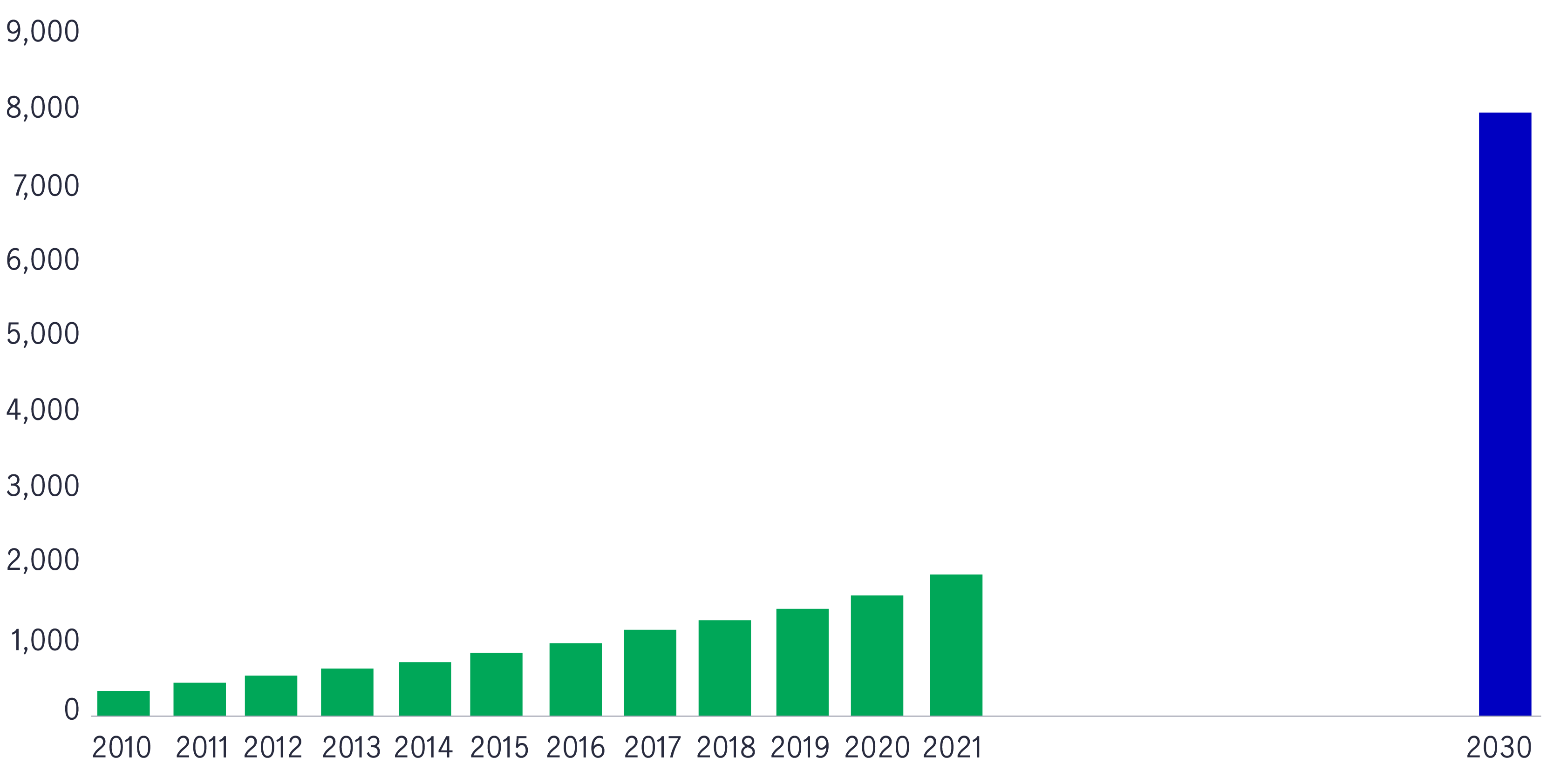

With solar and wind energy production having become less expensive, we’re seeing a steep acceleration of the ongoing energy transition. Wind and solar power generation grew 14% and 23% in 2021, respectively, while fossil fuel power generation increased 6%. Massive investments, however, will be needed to keep fueling that exponential growth, and private investors will have a crucial role to play in closing this funding gap.

Wind power generation needs to grow even faster to reach net zero

Wind power generation (TWh)

Source: IEA, September 2022.

Although low-carbon energy companies are, as a whole, beneficial for the planet, fundamental analysis and security selection are still critical within that sector to invest in companies that are superior from both an environmental and commercial standpoint.

For example, a company we particularly like in the wind power industry has not only dominant market share and a strong balance sheet but also stands out from an environmental standpoint—its carbon intensity is 7% lower than the industry average.1 The company also pledged to become carbon neutral by 2030 and invested more than 20% of its gross profit in R&D in 2021 to continue to increase its turbines’ productivity and efficiency.2 These actions indicate to us that this company isn’t only well positioned commercially but also committed to have a significant environmental impact today and tomorrow.

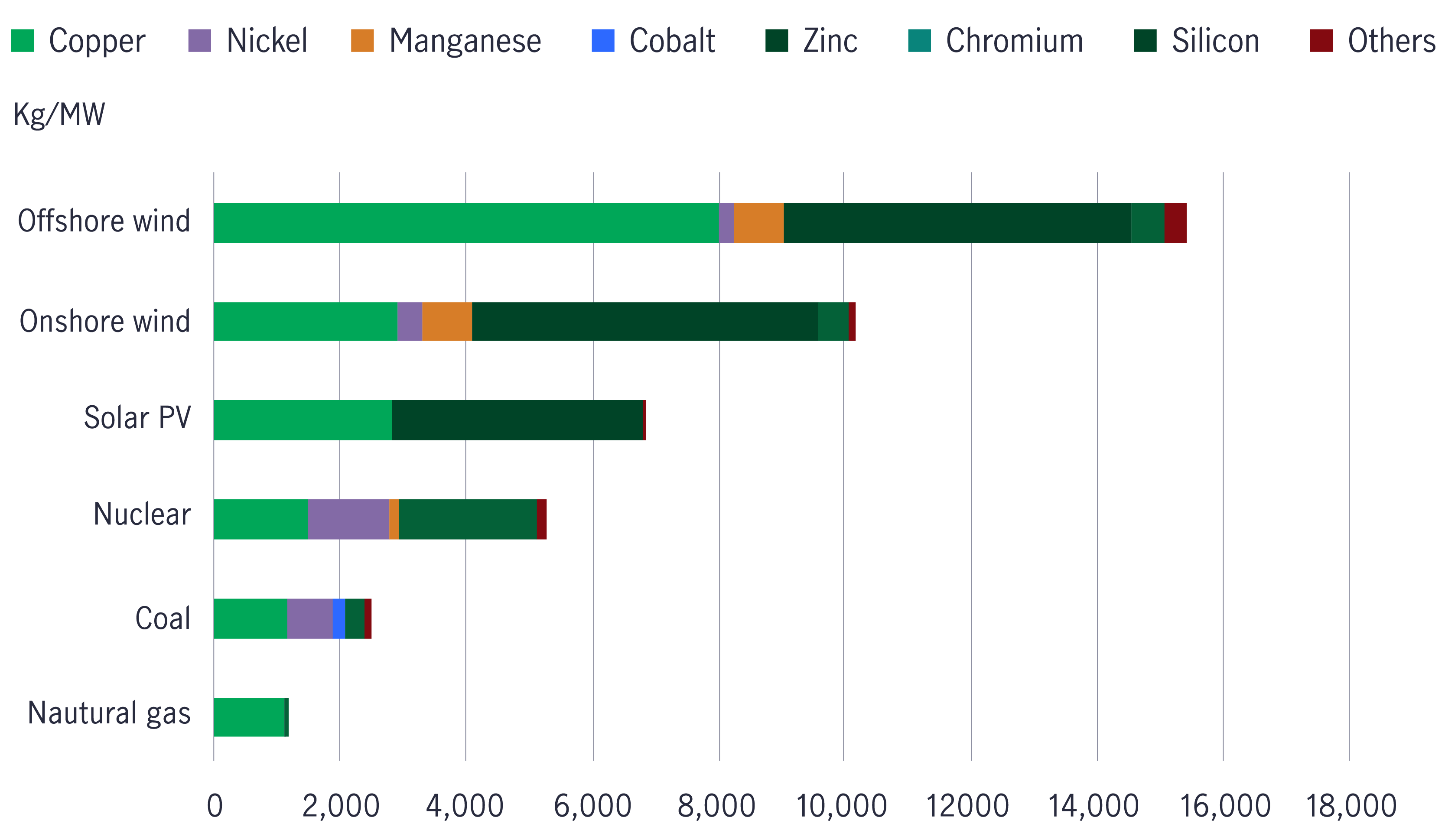

To fuel the ongoing green transition and reach net zero by 2050, the International Energy Agency (IEA) estimates that global investments in clean energy will need to triple by 2030 to around US$4 trillion. But there’s also no transition without the world mining more minerals.

Renewable power plants are usually in remote areas—offshore wind farms, for example, that can be miles away from shore—and bringing this power to populated centers will therefore require new and more copper transmission cables. Moreover, electric vehicles (EVs) require up to six times more minerals than conventional gasoline and diesel cars. In fact, according to the IEA, the market size of critical transition materials such as copper, cobalt, lithium, and nickel needs to grow almost sevenfold by 2030 to have a fighting chance of reaching net zero by 2050.

Clean energy technologies rely more heavily on minerals

Minerals used in cars and selected power generation sources

Source: IEA, 2022. Steel and aluminum not included. The values for vehicles are for the entire vehicle, including batteries, motors, and glider.

It’s no secret that extracting minerals produces greenhouse gas (GHG) emissions—the mining sector is responsible for 4% to 7% of GHG emissions globally. We therefore believe that while increased revenue stemming from growing demand for minerals will most likely create opportunities for mining companies to expand their operations and contribute to the green transition by providing more minerals, companies that will also focus on how they extract and operate to reduce their carbon footprint through the value chain will have the biggest positive climate impact.

Producing GHG emissions is inevitable for most mining companies. But from a climate-oriented investor’s perspective, transparency and having an action plan to control and reduce GHG emissions are the most important things in this carbon-intensive sector. For example, one of our holdings produced more than 4 million tonnes of carbon dioxide equivalent (Mt CO2e) in 2020,3 which is the equivalent of about 800,000 gasoline cars driven for a year. There’s no denying—the company has historically been a heavy polluter.

However, by extracting copper, nickel, and cobalt, the company is significantly contributing to the energy transition, and it does so with a carbon intensity 40% lower than the industry average.1 Moreover, the company is one of the first in its industry to publish a report that is aligned with the Task Force on Climate-related Financial Disclosures on its climate practices (transparency) and set aggressive GHG emissions reduction targets of 30% by 2025 and 50% by 2030 (action plan).

Producing cleaner energy and extracting more transition materials are critical to the green transition, but are also just one part of the story—how we use them is also key. To make the biggest climate impact, decarbonizing areas of the real economy that are dependent on fossil fuels such as transport and heating should also be prioritized.

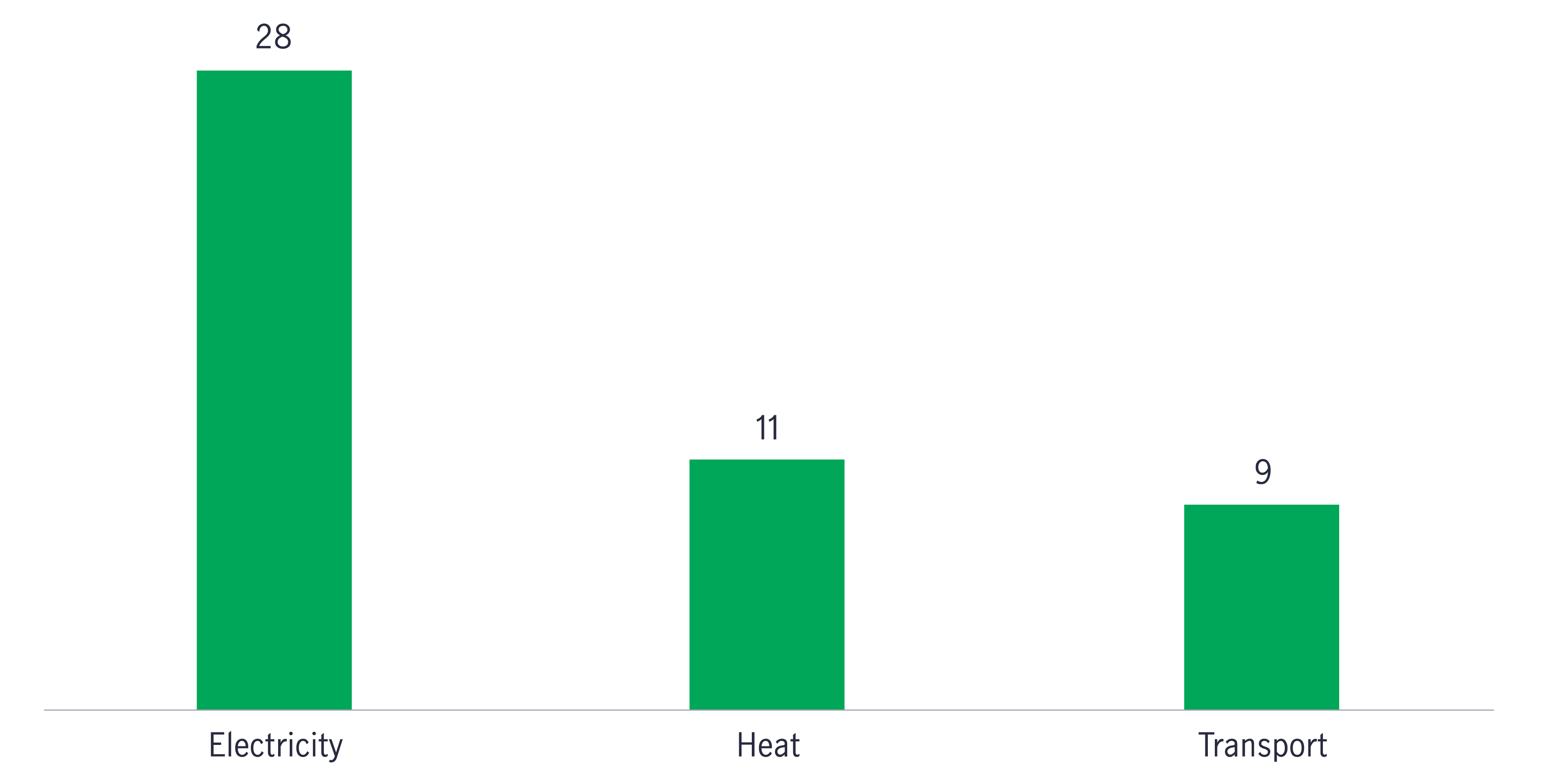

Transport and heating account for nearly 25% and 40% of global energy-related carbon dioxide (CO2) emissions, respectively, which is mainly explained by a low penetration of renewables in these two sectors. To reduce GHG emissions and reach a more sustainable future, these two sectors need significant investment in modernization and retrofitting.

There’s a large difference between the energy mix for electricity versus transport and heating

Share of energy from low-carbon sources (%)

Source: Manulife Investment Management, IEA, Renewables 2022.

Moving away from fossil fuels in these industries, however, is no easy task, since the infrastructure and the systems built over the past many decades were primarily designed to be powered by fossil fuels. Adapting to and integrating electricity technologies will therefore take time and capital, especially in these two sectors.

Moreover, there are areas where it’s structurally difficult to replace fossil fuels and where technology isn’t there yet. For example, the furnaces producing steel and cement need to operate at extremely high heat—more than 1,000ºC—and such a high temperature is hard to achieve without burning fossil fuels.

Electrification will go as far as technology takes it, and investors can help companies push the boundaries of innovation. We believe companies that have products or services that provide society with more efficient, and less carbon-intensive ways to operate, will continue to see sustainable demand from investors over the long term.

When we think about electrification, especially in the transport sector, EVs are usually top of mind. But there’s so much more work to be done in this sector. It’s widely acknowledged that to succeed in combating climate change, electrification must spread beyond cars and buses and extend to ships, trains, and long-haul trucks, which pose a bigger challenge than cars and buses, as they carry heavier loads on longer distances.

One of our current portfolio companies has made a step in that direction, developing the necessary technology to electrify ferries. Crossing times of the ferries haven’t changed and it only takes a few minutes to charge them when they reach the shore, but they save about 28,000 tonnes of CO2 per year. Moreover, the company doesn’t build ferries; it provides the battery technology to transform existing diesel ferries into electric-powered ones, thereby limiting its environmental impact.

We’re still far from being able to cross the Atlantic, as the current route for these ferries is only a few kilometers, but the company is an agent of innovation in areas that are critical to the green transition.

While the first three investment pillars—low-carbon energy, transition materials, and electrification and efficiency—mainly aim to reduce long-term global GHG emissions and limit the temperature rise of our planet to less than 2ºC above preindustrial levels, the main goal of the resource security pillar is to help address the consequences of rising temperatures.

From changing weather patterns and rising sea levels to more frequent and intense climate events such as prolonged droughts and torrential floodings, rising temperatures will increasingly challenge our already fragile ecosystem over the next decades. This threat is particularly important for food and water security, as the impacts of climate change are often first felt through water and land. We live in a world with finite resources to feed a growing population with rising standards of living, and we can’t really afford to lose arable lands and drinking water sources due to climate change. But the reality is that it’s a very real possibility.

“… the world will need to increase food production by more than 50 percent to feed nearly 10 billion people adequately in 2050.”

“By 2050, over half of the world’s population and half of global grain production will be exposed to severe water scarcity.”

—United Nations Convention to Combat Desertification

We believe, however, this is both a challenge and an opportunity: Investors who are mindful of the different forces at play to reach a more sustainable future can help solve these key issues by investing in companies that are contributing to stronger global food and water supply chains.

A company we consider to be a strong contributor to the green transition is a leader in the manufacturing of agricultural and other equipment. Its flagship products today are largely diesel-fueled, which produce a large amount of GHG emissions when used. Due to this large carbon footprint, the company may not make it through some negative screenings. The company, however, uses a large part of its revenue to invest in precision agriculture and to develop new technologies to lessen both emissions and the need for fertilizers.

By providing farmers with the tools they need to become more efficient in every aspect of their production process, from increasing crop yields to improving water management, this company is helping them feed a growing population and make the most of our world’s finite resources.

While the green transition is accelerating, we still have a long way to go before reaching net zero, and investors’ capital will certainly be key for companies to continue increasing renewable energy capacity, develop new technologies, and decarbonize their operations. We believe that investors who want to have the biggest impact on climate change shouldn’t limit their investments to only low-emissions companies, but rather companies that help the world reduce its carbon emissions and deal with the cascading effects of climate change.

We believe companies that extract transition materials, play a big role in our evolution to a lower carbon energy mix, are an agent of innovation and electrification, and/or help provide resource security for a growing population should also be considered when building climate-focused portfolios. Ironically, reaching a more sustainable future, in our view, is hardly achievable should investors decide to avoid the problem and filter out heavy polluters altogether from their portfolios, as that is where significant investment is needed to reduce emissions.

For us, being part of the climate change solution and investing effectively in the green transition means applying a thorough security selection process that looks beyond simple environmental metrics such as GHG emissions today and encompasses our four key investment pillars to assess future competitiveness and contribution to the low-carbon transition.

1 Manulife Investment Management, 2022.

2 The company’s 2021 annual report.

3 The company’s 2021 annual report.

Asset allocation views on SpaceX IPO, Reopening of Strait of Hormuz, and the BOJ rate hike

The Multi Asset Solutions Team (MAST) provides asset allocation views on three recent developments that could influence markets in different ways: the SpaceX Initial Public Offerings (IPO), the reopening of the Strait of Hormuz, and the Bank of Japan’s (BOJ) rate hike. In our view, these events create mixed signals across growth, inflation and liquidity. Overall, the backdrop still appears uneven, and this may support a measured and selective approach to asset allocation rather than a broad increase in risk.

Not another bubble: How semiconductors are powering a real future

Semiconductors sit behind almost every modern experience – from smartphones and cars to cloud computing and today’s AI tools – yet they remain largely invisible to most people. They are more than chips only, and the demand is being supported by several long-term forces. We believe that today’s semiconductor excitement is not a repeat of the dot-com bubble, as investment is tied to real infrastructure and revenue-generating services. And the opportunity is broader than a handful of headline AI names.

Global tech and semiconductors: what’s been driving returns and what to watch next

Semiconductors have been one of the strongest parts of global equity markets so far in 2026, with performance supported by a powerful mix of demand and improving fundamentals. The headlines have focused on artificial intelligence (AI), but the opportunity set is broader than a single theme or a handful of companies. As AI infrastructure expands, it is driving investment not only in high-performance computing chips, but also in the networking and power technologies that keep modern data centres running. At the same time, parts of the industry outside AI are showing early signs of stabilisation and recovery.

![]()

©1999 - 2026 Manulife Investment Management (M) Berhad (Registration No. 200801033087 (834424-U))