5 May 2025

The latest development in tariff-centric trading policies has been on the market’s radar, with a recent retaliatory announcement by China that imposed a 34% levy on all US-imported goods. The situation has sparked risk aversion and a notable correction in global equity markets. In this note, we examine the measures more deeply and assess their impact on Greater China equities.

Despite the US reciprocal tariff rates on mainland China and Taiwan, which are higher than the market expected, we believe mainland China has multiple options for further action. For instance, on 4 April 2025, it announced a 34% retaliatory tariff on all goods imported from the US1.

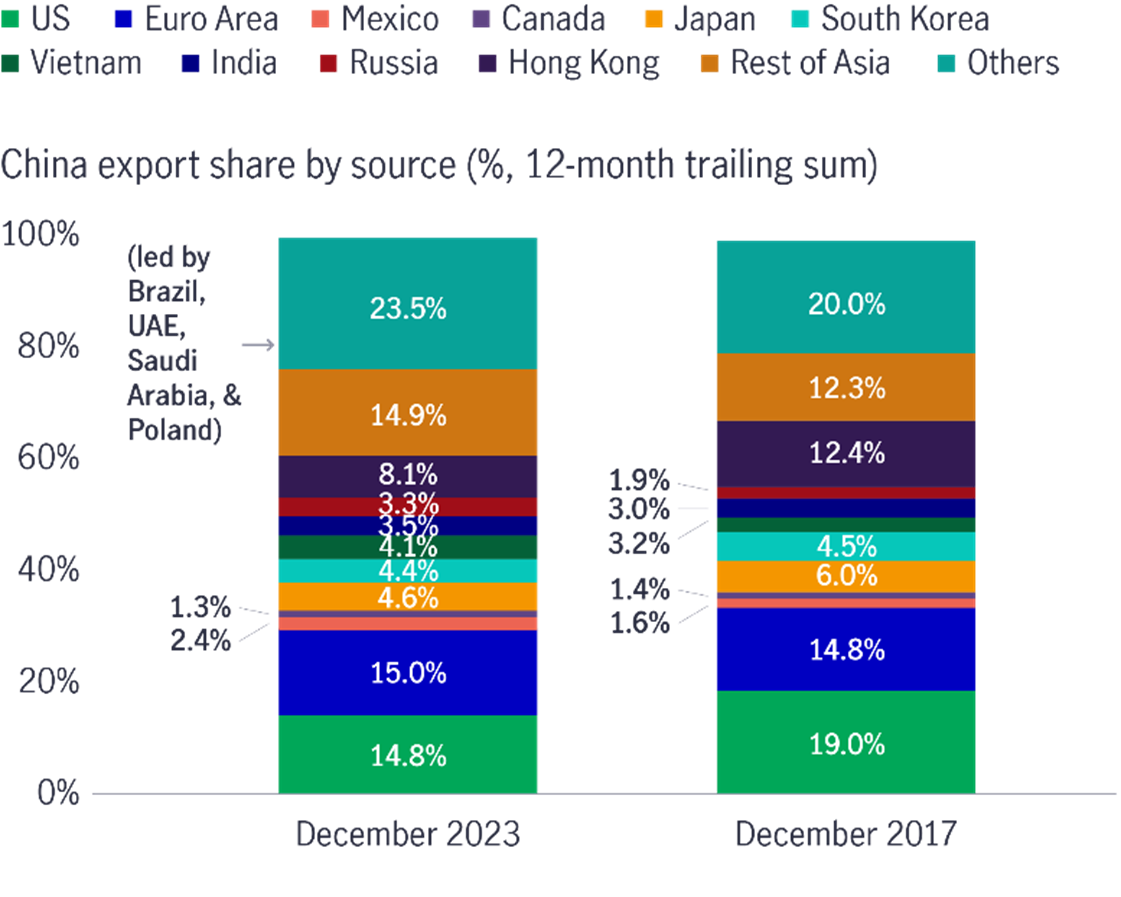

Tariffs are not new. Over the past years, mainland China’s exports to the US have declined while its exports to the rest of the world have increased. Hence, mainland China’s dependency on direct channels has been reduced. For example, mainland China’s exports to the US as a percentage of its export share was 19% in 2017. As of 2023, this had fallen to 14.8% (see Chart 1).

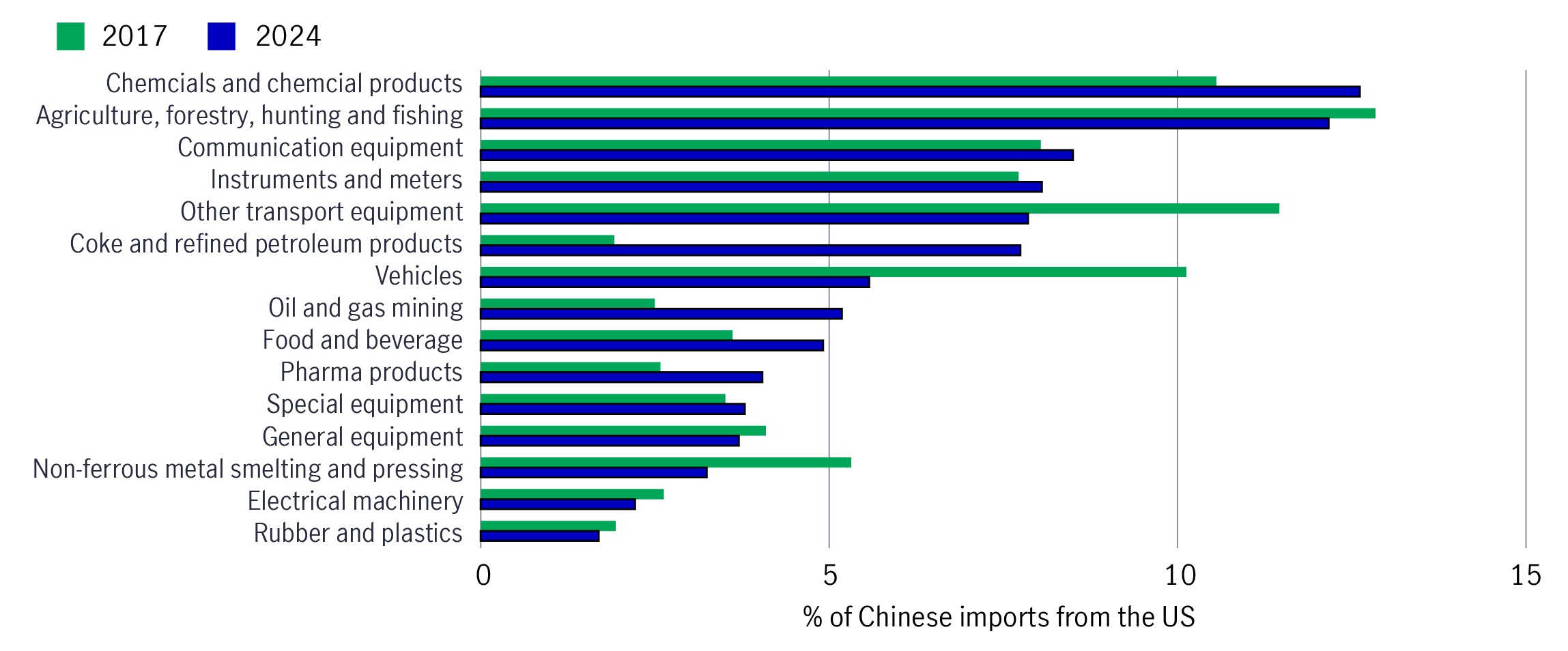

Having that said, mainland China still imports chemical, agricultural, forestry and communication equipment (top categories) from the US (see Chart 3), which, in turn, faces mainland China’s retaliatory tariffs.

Chart 1: China’s export share by source

Source: MS Research, April 2024

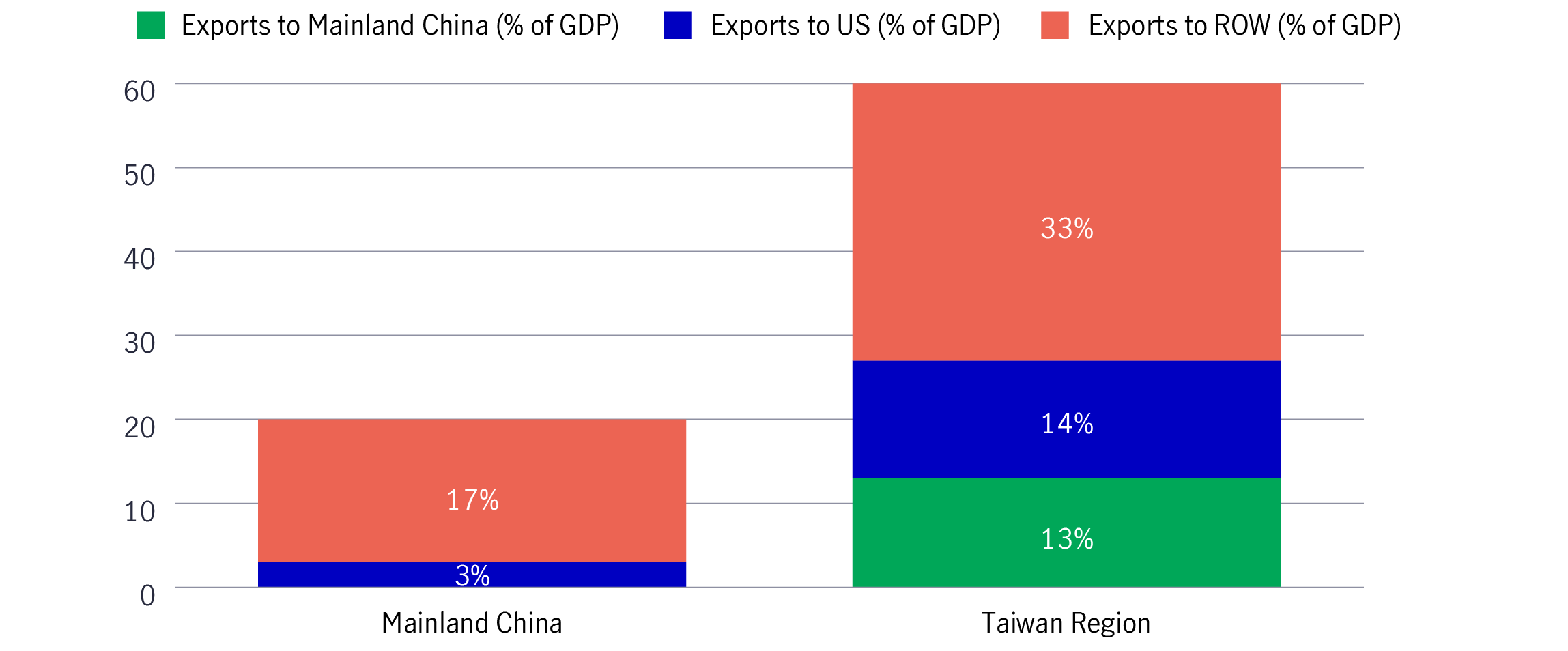

Chart 2: Goods exports to GDP (% of GDP, 12-month trailing sum)

Source: MS research, 3 April 2025

Chart 3: Top 15 Chinese imports from the US by sector (2024)

Source: GS research, April 2025

Mainland China is also ready to counter external uncertainties. During the Two Sessions plenary meetings in March 2025, it was highlighted that “the central budget has preserved sufficient policy tools and spaces to counteract domestic and external uncertainties.” Accelerated measures, such as a RMB 3 trillion increase in the government bond net issuance quota, were announced in the 2025 budget. See our previous note here.

We believe that further fiscal policies will follow, plus mainland China has room to ease monetary policies further, as highlighted during the Two Sessions.

Moreover, mainland China’s announcement on 30 March 2025 that it would allocate RMB 520 billion to shore up the capital of four domestic banks, including China Construction Bank, Bank of China, Bank of Communications and Postal Savings Bank, is positive, enabling them to provide further loan growth to support corporates and small and medium-sized enterprises (SMEs).

Over the year to date, mainland China’s technology related sectors, ranging from AI and robotics to hardware, software and autonomous driving, rallied. This came amid DeepSeek’s breakthrough, optimism surrounding mainland China’s AI and technology acceleration, as well as localisation trends as many companies embrace AI/inference. Overall, mainland China continues to advance on the home-grown technologies front, which is encouraging.

Consumption remains an essential driver of mainland China’s economy. Trade-in policies for consumer goods (e.g., electronics, home appliances, and communication equipment) have boosted domestic consumption since the fourth quarter of 2024 and into 2025. Mainland China may also provide more holistic stimulus to boost consumption (e.g., increasing incomes and wealth by supporting employment as well as raising pensions and elderly/childcare benefits).

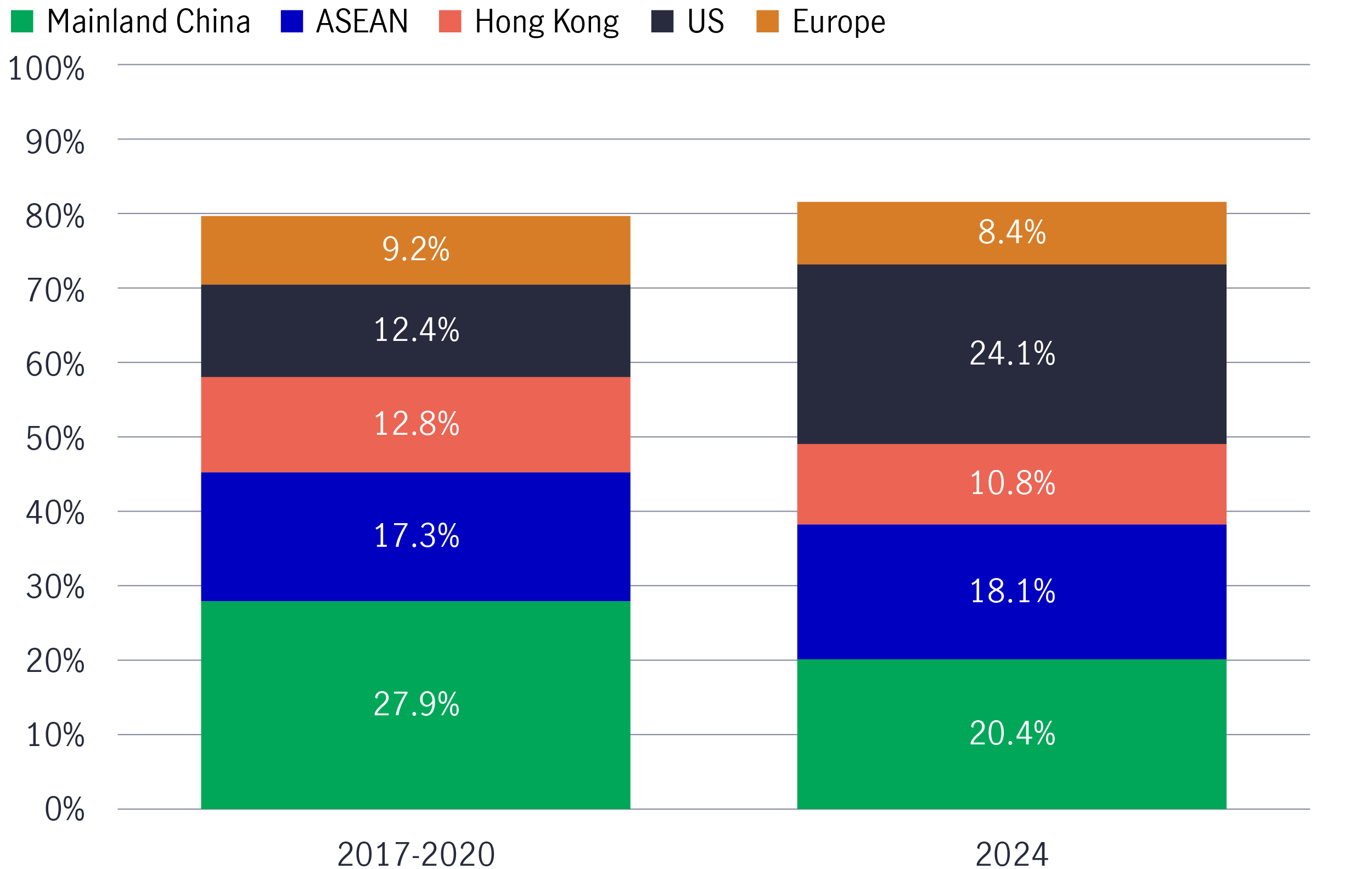

Taiwan region’s export exposure to the US increased by around 24.1% in 2024 – almost double that seen in the period 2017-2020 (see chart 4). By product type, information, communication, video/audio products, and electronic components remained the top categories. However, for now, semiconductors have been exempted from the reciprocal tariff list, which should be positive. Over the medium term, we still favour leading foundry companies.

Chart 4: Taiwan region: export to top five destinations (% share to total exports)

Source: Taiwan Ministry of Finance, MS research, April 2024

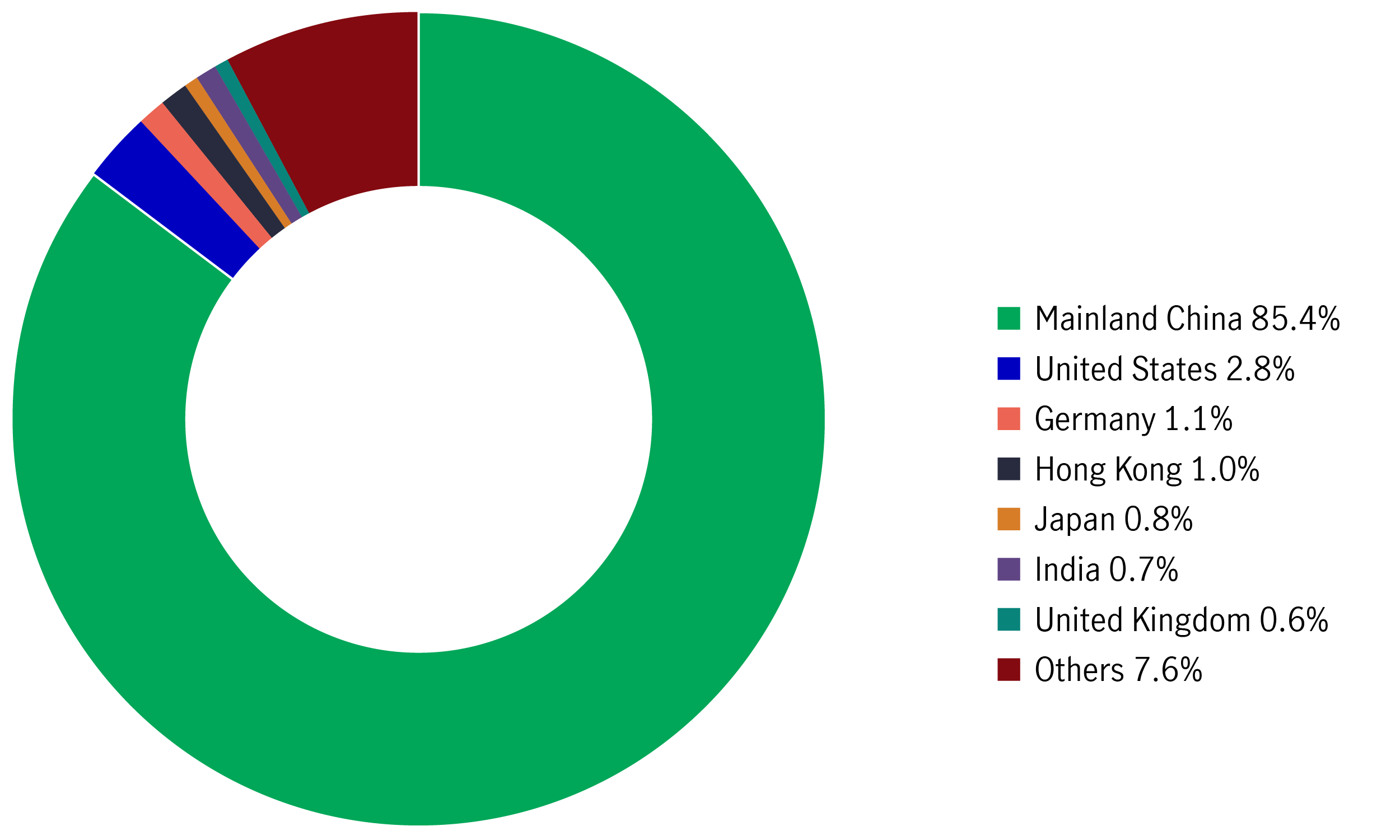

MSCI China Index only has <3% of revenue exposure to the US, which is low (see Chart 5).

Our Greater China equity strategies are defensively positioned as the investment team has recently taken partial profits on mainland China technology, media and telecommunications names as well as Taiwan IT and hardware companies. At the same time, it has added exposure to domestic-oriented areas, such as mainland China software, consumption, and healthcare names.

However, over the medium-to-long term, we continue to advanced manufacturing leaders, beneficiaries of the AI and robotics supply chain, and domestic niche consumption leaders. Mainland China continues to accelerate its technological self sufficiency with notable breakthroughs that continue to take leadership strides.

Chart 5: MSCI China last 12 months revenue breakdown by markets

Source: MS research, March 2025

1 China Ministry of Commerce, 4 April 2025.

2026 Mid-year outlook: Greater China Equities

Greater China equity markets showed divergent trends in the first half of 2026, with China A-shares and the Taiwan Taiex index registering strong gains driven by resilient technology exports amid global demand for artificial intelligence (AI). Meanwhile, the MSCI China market pulled back, weighed by commerce subsidies amid fierce competition in food delivery and rising AI capital expenditure, which we believe have already been priced in. In this mid-year Outlook, we highlight five positive drivers for China and Hong Kong equities in the second half of the year. Furthermore, the team explains why it believes the Taiwan region’s technology sector should continue to enjoy positive momentum.

2026 Mid-Year Outlook Series: Asia Equities ex-Japan

Asia equities ex-Japan continued the significant momentum from 2025 with strong performance throughout the first half of the year. Amid numerous catalysts, June Chua, Head of Asia Equities outlines in this Mid-Year Outlook why she is constructive on the asset class for the remainder of 2026. Positive drivers include: potential geopolitical resolution in the Middle East and lower energy costs, supportive earnings and valuations, and differentiated growth drivers across the region.

Asset allocation views on SpaceX IPO, Reopening of Strait of Hormuz, and the BOJ rate hike

The Multi Asset Solutions Team (MAST) provides asset allocation views on three recent developments that could influence markets in different ways: the SpaceX Initial Public Offerings (IPO), the reopening of the Strait of Hormuz, and the Bank of Japan’s (BOJ) rate hike. In our view, these events create mixed signals across growth, inflation and liquidity. Overall, the backdrop still appears uneven, and this may support a measured and selective approach to asset allocation rather than a broad increase in risk.

Real assets and the infrastructure behind AI

Artificial intelligence (AI) is often positioned as a story of models and applications, but its growth depends heavily on something far more tangible. Real assets such as data centres, power grids, and raw materials form the physical that supports AI development. As structural forces reshape the investment landscape, real assets are emerging as an enabler of the AI buildout.

AI innovation: Asia helps build many of the world’s technologies behind it

When electricity first arrived, the world built the necessary infrastructure – power plants, transmission lines – before the real transformation could take hold. A similar process is happening with artificial intelligence (AI). Today's massive investment in chips, data centres, and power grids is laying the foundation for a potential expansion in AI application that could take years to develop. In our view, the discussion is increasingly shifting from whether AI adoption will continue to how the enabling infrastructure is being built. Asia appears to be playing an important role in that development.

The engine behind AI: Semiconductors are fuelling the next era of technology

Semiconductors belong to one of the most specialised yet globally integrated industry chains. From design, equipment, and materials to manufacturing and commercialisation, the production of a smartphone chip alone spans many countries across continents, creating tremendous opportunities for companies, consumers, and investors. With semiconductors increasingly becoming the backbone of an artificial intelligence (AI) race few are prepared for, understanding this sector is key to unlocking where the next wave of technology competition is heading.

![]()

©1999 - 2026 Manulife Investment Management (M) Berhad (Registration No. 200801033087 (834424-U))