15 May 2023

Judy Kwok, Head of Greater China Fixed Income Research

Jack Ko, Director, Greater China Fixed Income Research

Recent market volatility has focused attention on the health of the global banking sector. Regional bank failures in the US, coupled with a government-brokered merger and the writing down of Additional Tier 1 instruments (AT1s) in Switzerland, have led investors to wonder about the implications of these events for Asia (ex-Japan) banks. Judy Kwok, Head of Greater China Fixed Income Research, and Jack Ko, Director, Greater China Fixed Income Research, explain in this investment note that near-term volatility in the global banking sector should persist. However, they also point out that Asia’s banks are differentiated and potentially well positioned compared to their global peers, with selective opportunities available among the stronger regional AT1 issuers.

Investor concern over the banking sector has centred on recent developments in the US and Europe.

In the US, Silicon Valley Bank and Signature Bank went into federal receivership in mid-March. Shortly after, First Republic Bank initially received deposits from larger peers after fears of contagion grew; however, J.P. Morgan ultimately purchased most of the bank’s assets in early May after it entered receivership.

The bank failures in the US were a unique combination of macroeconomic and idiosyncratic factors: a rapidly rising interest-rate environment put pressure on banks, particularly smaller ones, that had significant unhedged long-duration investments.

At the same time, the rapid withdrawal of deposits from banks with concentrated deposit bases to capture higher-yielding investments (such as money market funds) meant that liquidity concerns ultimately transformed into solvency issues for a few select financial institutions.

In Europe, the dynamics were less systemic in nature and more contained. In Switzerland, UBS acquired Credit Suisse in mid-March when concerns about the latter’s solvency, which were not new, re-emerged.

As part of a government-brokered acquisition, FINMA, the Swiss financial regulator, ordered Credit Suisse to write down the company’s AT1s (See the appendix for a brief introduction) to zero. In contrast, the bank’s equity holders retained the value of their shares, a controversial arrangement as most investors expect a seniority hierarchy that places hybrid bank capital instruments above shares.

While the possible write-down of AT1s has always existed – indeed, it had occurred for other banks, such as Spain’s Banco Popular in 2017, the lack of such a public, widely-held, and influential precedent in the asset class shook investors’ confidence globally.

The tremors from the Swiss AT1 write-down were inevitably felt in Asia, although they were arguably more muted.

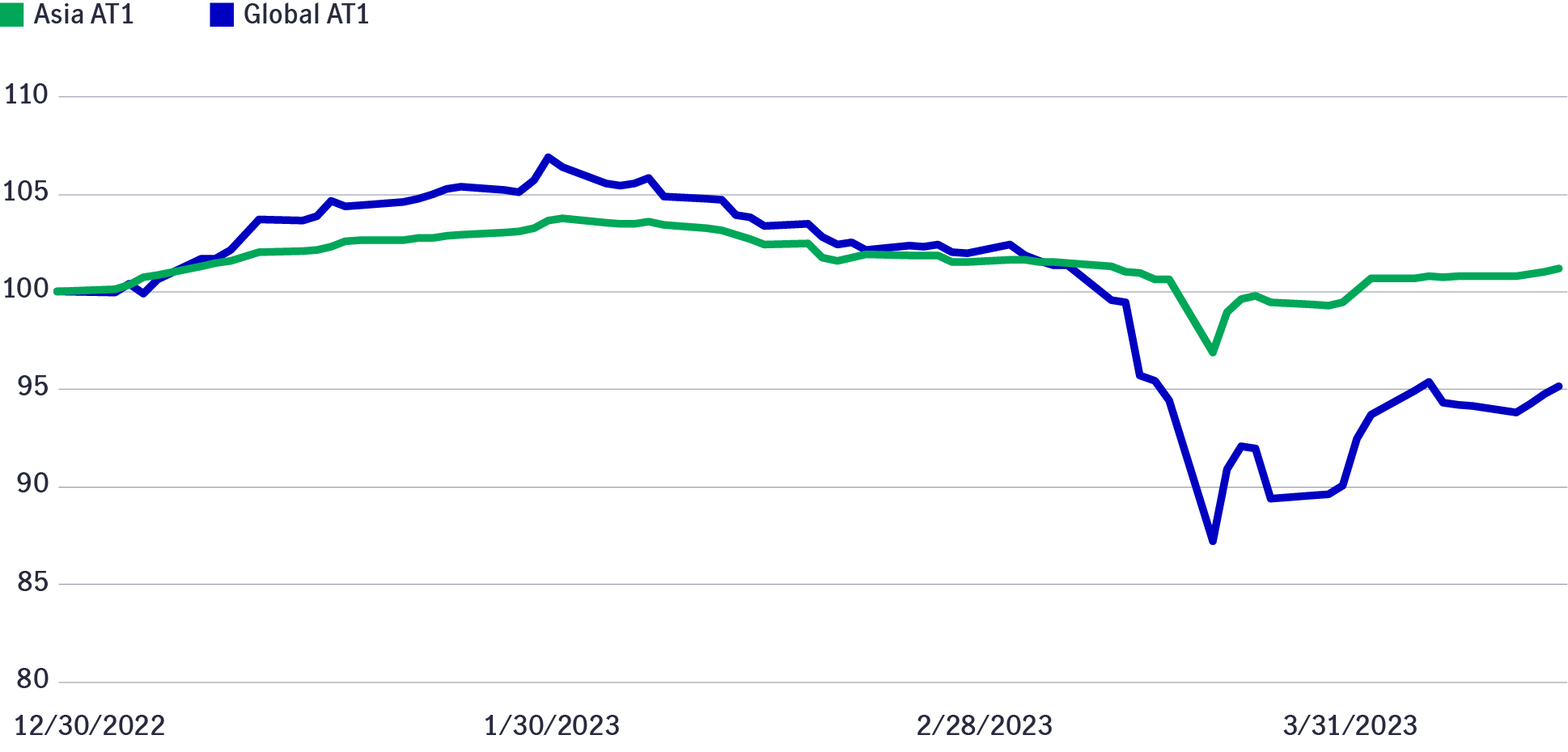

The total return of AT1s issued in the region initially declined alongside their global counterparts (See Chart 1). However, decline in AT1 prices in Asia was less severe compared to other markets, and retraced to pre-Swiss write-down levels, while global AT1s remain below. Regionally, Chinese banks’ AT1s showed the most resilience among issuers.

Chart 1: Global and Asia AT1 total return performance (year-to-date)

Source: Bloomberg, as of 3/31/2023. Rebased to a value of 100.

Overall, we believe that volatility in the Asia AT1 market may persist in the short term given the uncertainties regarding the depth and the second-order effects of banking stresses in the US and Europe. Any further intimation of bank distress could send the sector into another period of amplified volatility.

For AT1s, non-call events1 could also negatively impact market sentiment towards the asset class. We believe the announcement of new-issuance activities should help to alleviate investors’ concerns. Over the short-term, there could still be opportunities for strong Asian banks AT1s where price recovery lags their peers after recent market action.

Although Asia was inevitably affected by recent ructions in the sector, we believe the factors underlying recent instability are less prevalent in the region. Indeed, taking a longer-term view, Asia’s banks are potentially better positioned to navigate volatility compared to Western peers, providing selective investment opportunities in AT1s.

Although Asia’s banks encompass diverse economies amid varying development levels, the region generally boasts a higher level of state ownership in banks than the US and Europe.

Indeed, assets owned by state-owned institutions, or government sponsored, in Asia’s larger economies are greater than global peers. The level of state ownership coupled with potential policy support helps bolster the overall stability of the sector in Asia, including proactive policies to mitigate contagion risks.

The operating models of the region’s banks also differ from those in the US and Europe. Asian banks generally boast more conservative liquidity management, which is built on a significant base of household deposits and healthy liquidity ratios. In addition, major Asian economies have introduced some level of deposit insurance, which should protect the vast majority of depositors and potentially mitigate large-scale withdrawals.

Further, Asia’s banks may be more protected from sizable losses related to fixed income investments. Banks in the region generally hold a lower proportion of fixed income to loans as assets on their books than their Western counterparts. Additionally, most Asian banks’ unrealised losses from available-for-sale assets are accounted for in the Core Tier I capital ratio under IFRS accounting guidelines, which provides higher transparency of genuine capital strength.

The region has also pursued a more gradual interest rate hiking strategy. Indeed, China has broadly adopted countercyclical monetary policy (a topic addressed in the next section); central banks in India, Indonesia, Singapore, and South Korea have all effectively paused their rate hiking cycles awaiting further signs of persistent inflation.

The differences in policy support and bank management may offer opportunities among stronger banks in the region’s burgeoning AT1 market.

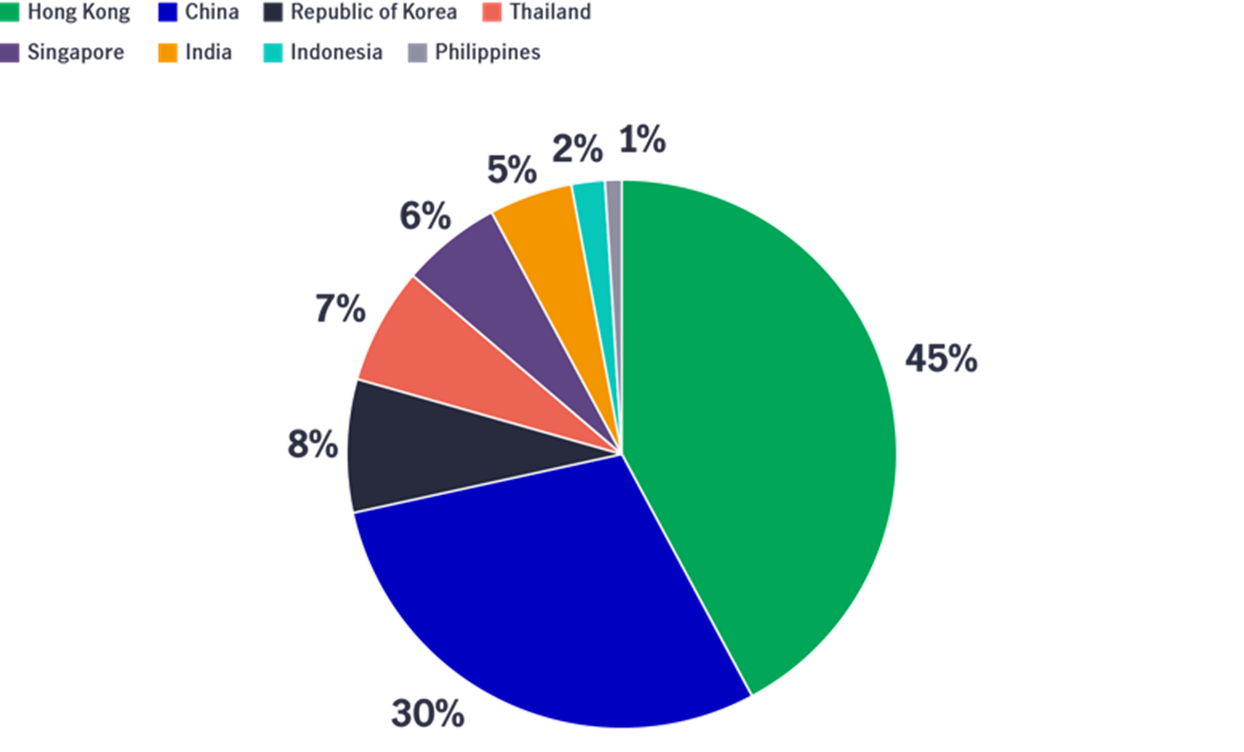

Although Europe’s banks account for a vast majority of global AT1 issuance, Asia’s banks have been actively issuing the instruments to meet their US-dollar funding needs and Basel III capital requirements. Looking at Chart 2, Hong Kong and China issuers account for roughly 75% of the region’s outstanding AT1 instruments by market value.

Mainland China banks likely represent a majority of regional (ex-Japan) issuance as they issue onshore in China, as well as offshore in Hong Kong (along with global and local banks). Indeed, China state-owned banks have been the leading international issuers totalling US$42 billion in AT1s over the past 18 months.

With China’s unique policy environment and cyclical economic position, the market may provide pockets of opportunity for long-term investors of AT1s.

Chart 2: Outstanding issuance of Asia financial sector’s AT1s (market value)

Source: J.P. Morgan Asia Credit Index junior subordinated bonds market value as of 31 March 2023.

For several reasons, we believe that China banks may be potentially more shielded from the current global volatility.

First, state-owned banks, the largest domestic issuers of AT1s, potentially benefit from policy support due to their status. China’s "Big Four" state-owned banks have been classified as global systemically important banks (G-SIBs) by the People’s Bank of China (PBOC) and the Financial Stability Board. They also play a pivotal role in the country’s economic development and credit allocation. As a result, they are likely to receive some level of government financial support, particularly during times of increased market volatility or economic turmoil.

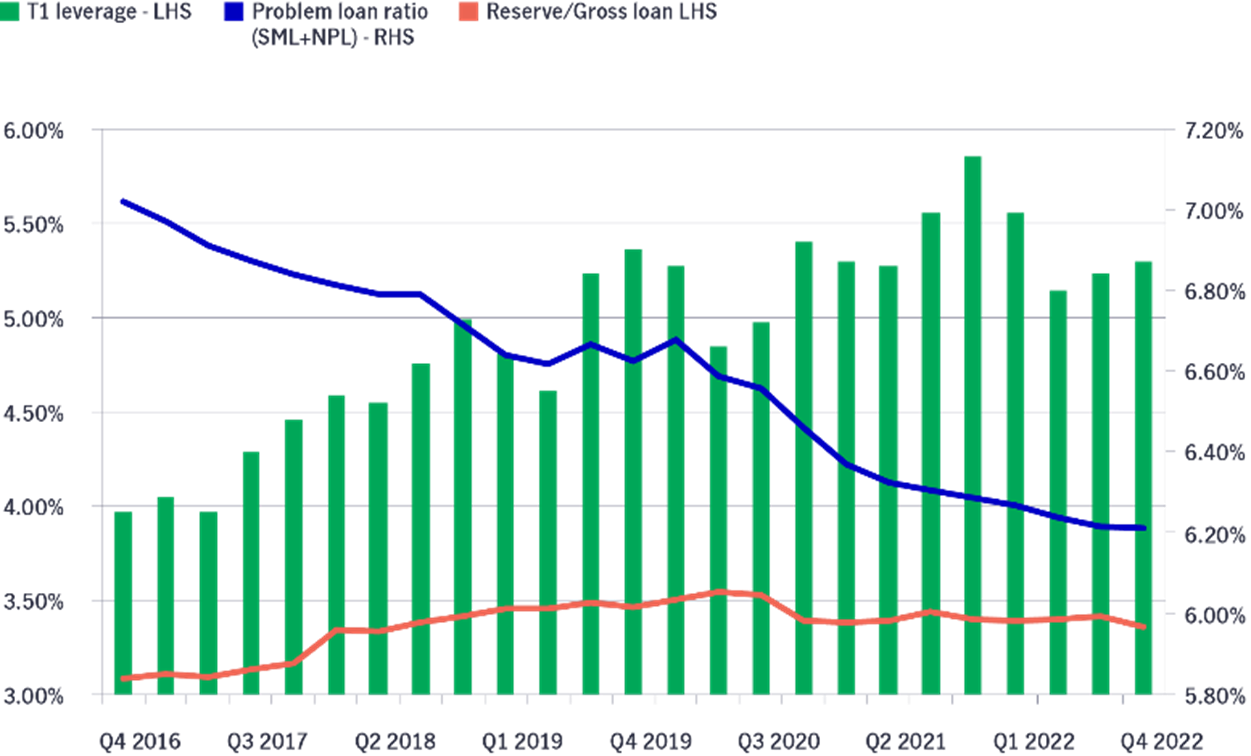

They have also shown improved operational performance over time. As seen in Chart 3, the problem loan ratio, which is the sum of the special mention loan ratio and non-performing loan ratio, has declined over the past five years. At the same time, their Tier 1 leverage ratio (Tier 1 capital as a percentage on and off the balance sheet) is trending at a historically high level.

Finally, China banks will likely benefit from cyclical policy support amid the current volatility. China has adopted a countercyclical monetary policy due to its belated economic reopening from COVID-19, evidenced by the recent cut in the banks’ reserve requirement ratio in March.

Overall, the PBOC is expected to pursue a more accommodative path due to lower inflation and the continuing challenges of stoking domestic demand and reviving the country’s property sector over the near-term.

Chart 3: China banks’ improving operating performance

Source: CBRC, CEIC data, and Manulife Asset Management analysis.

The recent volatility in the banking sector reminds investors of the critical importance of robust credit research and selection. Although some Asian banks potentially benefit from government support, this may not extend to all subordinated instruments. This is particularly true for AT1s designed to "bail in" investors and protect taxpayers and depositors.

Indeed, two recent precedents exist in Asia. In 2019, a bank in China was offered government support but AT1 investors did not receive their promised coupon payments. In 2020, the AT1s of Yes Bank in India were fully written down at the directive of the Indian government.

In addition to "bail in" risk, AT1 investors also face non-call risk, where bank issuers may not redeem AT1 instruments when they become redeemable, effectively lengthening the tenor of the instruments, potentially into perpetuity. A "non-call" event could cause a price drop of AT1s in addition to other risks investors are taking.

Overall, we view banks' profitability as a critical factor for investors to assess the credit quality of AT1s. AT1s behave like equities during economic downturns because of their perpetual and discretionary coupon skip features. In other words, banks may skip AT1 coupon payments, or their call dates, when they experience net losses.

The general AT1 market may see greater volatility when there are increasing risks of a coupon skip or non-call event. In a more adverse scenario, net losses may trigger a confidence crisis, or even a bank run, which could quickly erode banks’ capital or liquidity buffers, and lead to increasing risk of AT1s being completely written off.

Volatility in the global banking sector is likely to continue over the short term as high interest rates and slowing economic growth dominate the macroeconomic landscape. Over the medium term, Asia’s banks are generally better positioned due to stronger government support and more stable fundamental profiles, such as Singapore’s major banks. We see selective opportunities available for AT1s of banks with more stable deposit bases, improving profitability, and that have AT1s prices recovery which still lag their peers after recent market volatility.

AT1s have a brief history. They emerged after the 2007-2008 Global Financial Crisis as a hybrid security meant to bolster banks’ capital reserves. The motivation was to expose investors in banks to losses, rather than governments and taxpayers who bailed out banks in the GFC, through a "bail-in"- or potential loss of capital.

AT1s have become popular instruments to help banks meet capital requirements under the Basel III agreement. They are counted as part of a bank’s Additional Tier 1 Capital.

1 ‘’Non-call’ risk exists when issuers do not redeem a bond at its call date, such as Banco Santander’s non-call decision that upended markets in 2019.

Asset allocation views on SpaceX IPO, Reopening of Strait of Hormuz, and the BOJ rate hike

The Multi Asset Solutions Team (MAST) provides asset allocation views on three recent developments that could influence markets in different ways: the SpaceX Initial Public Offerings (IPO), the reopening of the Strait of Hormuz, and the Bank of Japan’s (BOJ) rate hike. In our view, these events create mixed signals across growth, inflation and liquidity. Overall, the backdrop still appears uneven, and this may support a measured and selective approach to asset allocation rather than a broad increase in risk.

Not another bubble: How semiconductors are powering a real future

Semiconductors sit behind almost every modern experience – from smartphones and cars to cloud computing and today’s AI tools – yet they remain largely invisible to most people. They are more than chips only, and the demand is being supported by several long-term forces. We believe that today’s semiconductor excitement is not a repeat of the dot-com bubble, as investment is tied to real infrastructure and revenue-generating services. And the opportunity is broader than a handful of headline AI names.

Global tech and semiconductors: what’s been driving returns and what to watch next

Semiconductors have been one of the strongest parts of global equity markets so far in 2026, with performance supported by a powerful mix of demand and improving fundamentals. The headlines have focused on artificial intelligence (AI), but the opportunity set is broader than a single theme or a handful of companies. As AI infrastructure expands, it is driving investment not only in high-performance computing chips, but also in the networking and power technologies that keep modern data centres running. At the same time, parts of the industry outside AI are showing early signs of stabilisation and recovery.

![]()

©1999 - 2026 Manulife Investment Management (M) Berhad (Registration No. 200801033087 (834424-U))