Retirement today looks very different from the past. People are living longer, careers are less predictable, and retirement can now last 30 to 40 years — yet many retirement systems were designed for a very different era.*

Across Asia, people want more than just a longer life. They want financial independence, dignity, good health, and peace of mind throughout retirement. However, research shows a widening gap between these expectations and actual readiness. At the same time, we live in an increasingly uncertain world.

Geopolitical tensions and economic cycles regularly dominate headlines. Market volatility may feel unsettling especially when retirement feels more personal. At Manulife Investments, we believe shaping the future of retirement requires active partnership. Strong retirement outcomes are built through thoughtful planning, diversification, and long‑term alignment — helping individuals and advisers stay focused on long‑term objectives rather than reacting to short‑term market movements.

* Source: Manulife Financial Resilience & Longevity Asia Report 2025, Manulife Asia Care Survey 2025, Securing Retirement - Manulife Investment Management 2024

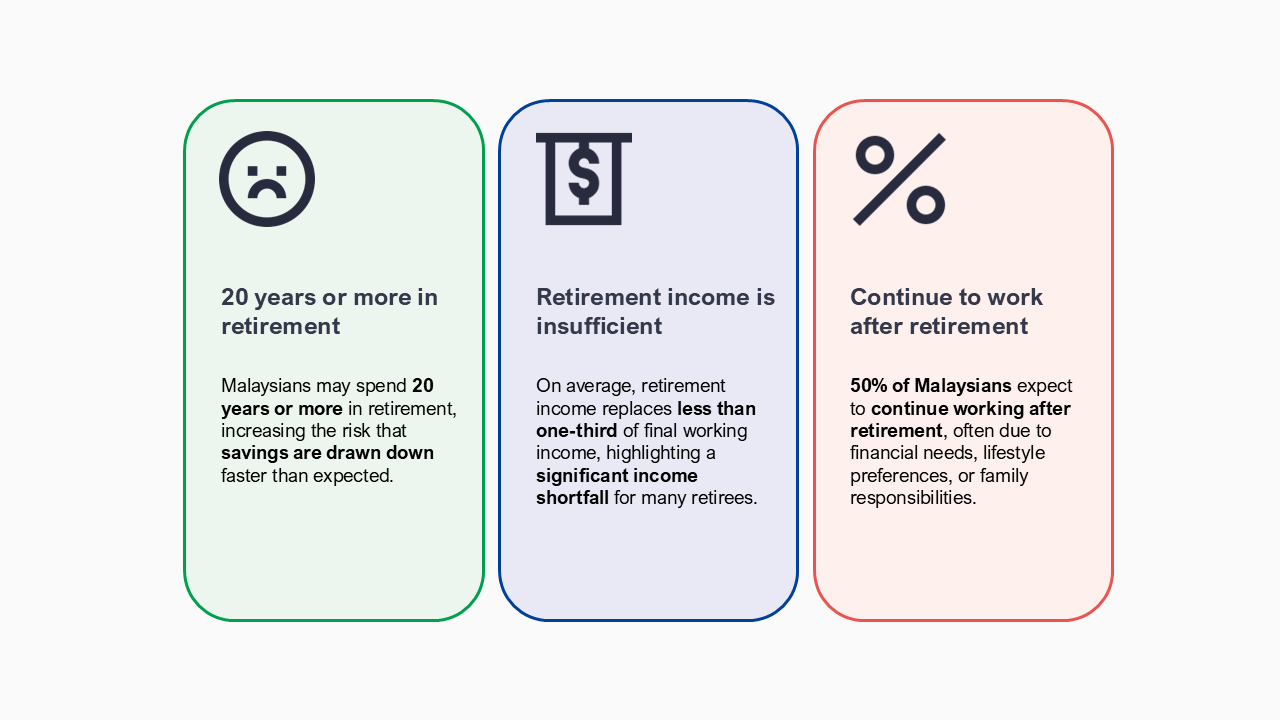

Retirement planning often focuses on how much can be accumulated by retirement. What may be overlooked is whether those savings can provide reliable income throughout retirement, which may span several decades.

Longer life expectancy means individuals may need income for much longer than anticipated, while rising living costs place additional pressure on fixed or insufficient income stream

This highlights a critical shift in retirement thinking: readiness is not only about reaching a savings target, but about whether income can be sustained over time, adapt to changing needs, and keep pace with long‑term living costs.

Source: Manulife Financial Resilience & Longevity Asia Report 2025, Diverse Asia

Malaysia’s public mandatory retirement system plays an important role in helping individuals build savings during their working years. It is designed to provide a baseline level of support, rather than to fully replace pre‑retirement income.

A more resilient approach often includes combining mandatory savings with:

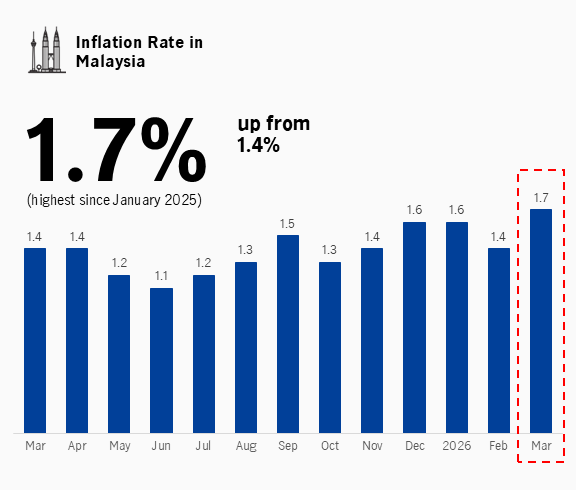

Inflation often works quietly, increasing prices gradually over time. Over a 20‑ to 40‑year retirement, even modest annual inflation can significantly reduce purchasing power. If inflation is underestimated, retirement income may support a very different standard of living than initially expected. In Malaysia, inflation has remained steady but since January 2025, headline inflation stood at 1.7%, a level that relatively moderate but still reflects ongoing increases in everyday costs.

Source: Department of Statistics, Malaysia

The inflation rate is compared between March 2021 and March 2026, with March 2021 chosen as the starting point to observe a five-year inflation trend.

Source: Department of Statistics, Malaysia

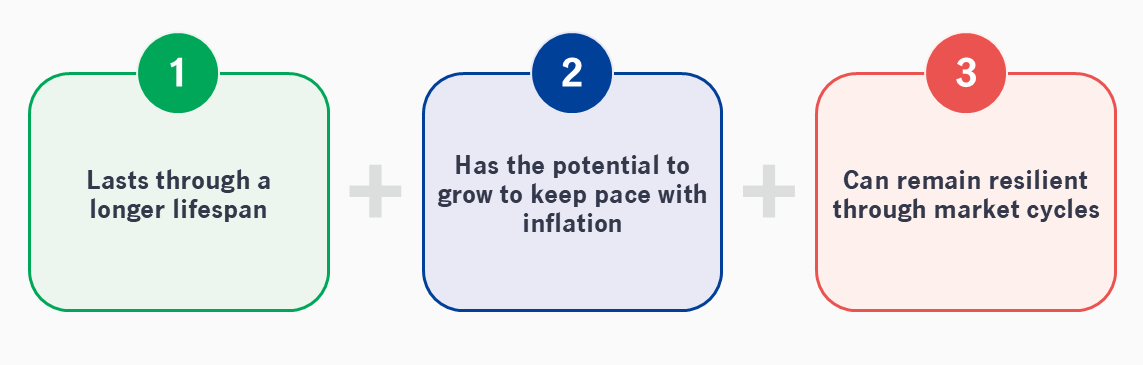

A more resilient retirement plan considers income that:

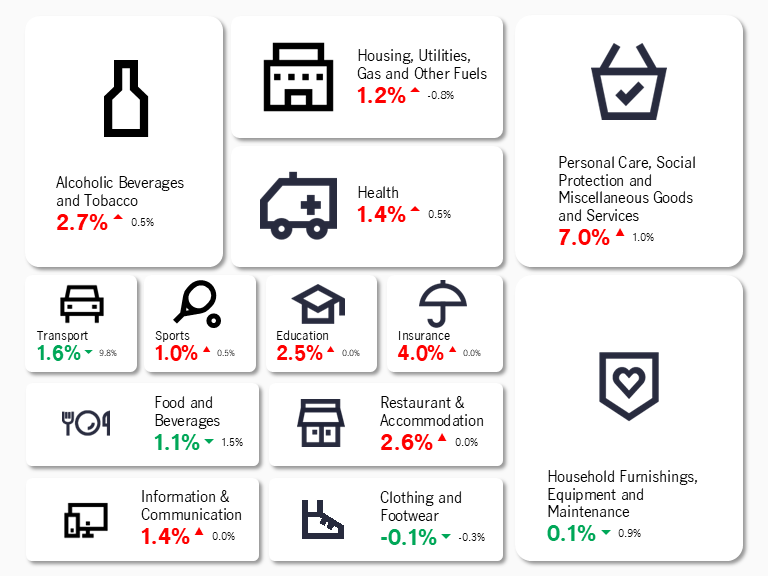

Inflation affects essential expenses where flexibility is limited — particularly food and healthcare. These costs cannot be easily postponed, especially later in life.

Even modest annual increases can compound over time, raising the cost of maintaining a similar standard of living. A comfortable retirement depends on income that lasts, grows with inflation, and holds steady through market volatility.

Source: OpenDOSM – Consumer Prices Dashboard & Monthly CPI by Division (2‑digit), Food and Health categories (page last updated 19 Feb 2026)

Education costs illustrate how long‑term inflation can accumulate. Many retirees continue to support children or grandchildren, making education a potential expense even during retirement.

Over time, education costs may increase materially, reinforcing the importance of considering intergenerational financial commitments as part of retirement planning.

Source: Trading Economics (DOSM‑sourced), CPI and Food Inflation data, Mar 2026, DOSM – Annual CPI by Division (2‑digit), Division 10: Education (2006 & 2025 indices, released 19 Feb 2026); OpenDOSM Consumer Prices Dashboard (Education YoY ~3.2% as at Dec 2025); Study Australia – Living and education cost estimates (as of 13 Mar 2026); Bank Negara Malaysia - Foreign Exchange reference rate (1 AUD = RM2.8052 on 12 Mar 2026).

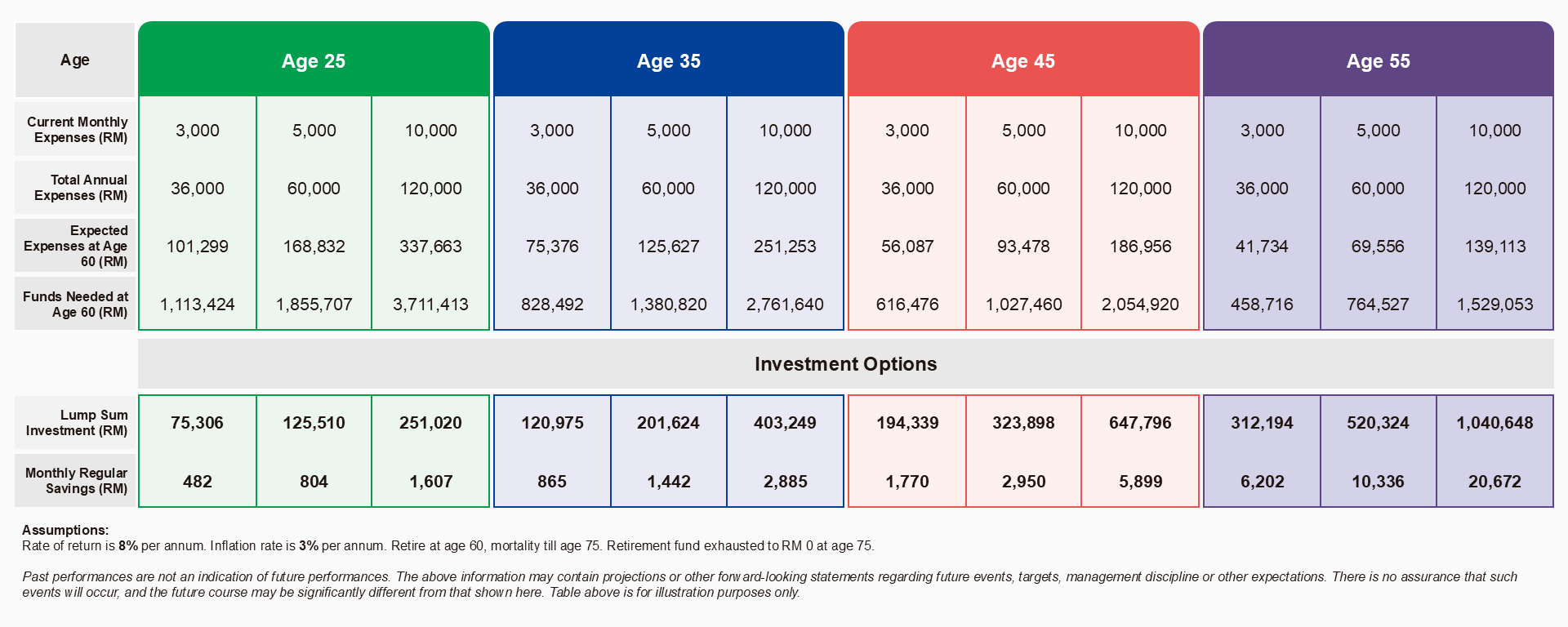

Numbers become meaningful when they reflect real life. These tools can help translate long-term concepts into more tangible insights.

This table provides a high‑level, indicative view of potential retirement income based on different starting ages, expense levels, and savings approaches. It helps surface potential income gaps early by showing the estimated fund needed and the corresponding lump‑sum or monthly savings required.

Designed purely as an educational starting point, it is not financial advice and should be used to guide initial conversations and planning rather than as a final retirement plan.

There is an imminent need for people in Malaysia to plan for retirement, and truly know how much sustainable income they will need in retirement to tackle key issues such as longevity risk, soaring living expenses, and future lifestyle and family matters.

Using our proprietary Retirement Income Forecaster tool created by the Manulife Investment Management Multi-Asset Solutions Team, you can estimate the monthly income you could have during retirement based on your current age, income, and amount of investable assets.

Compounding refers to the ability of returns to generate additional returns over time. For long‑term goals such as retirement, time and consistency may have a meaningful impact on outcomes.

Starting earlier and investing regularly, even with smaller amounts, can potentially improve long‑term results compared to starting later.

Time works in your favour

Compounding allows returns to build on previous returns, so growth increase gradually the longer money stays invested.

Small, consistent efforts can add up

Regular contributions over time may result in meaningful outcome than irregular, larger amounts invested later.

Supports longer-term goal like retirement

For goals that span decades, such as retirement, compounding helps align saving and investing with the realities of longer life expectancy.

Retirement income concerns are common, though not always openly discussed. This short‑form video series reflects everyday perspectives on cost‑of‑living pressures, savings behaviour, and long‑term preparedness. Follow the series, challenge your assumptions, and see how financially ready you really are.

Content reflects personal views and experiences and is for general informational purposes only.

Starting early and continuing to invest during all stages in life, and creating your own income stream could alleviate mental stress. These curated insights are designed to help you see the bigger picture — beyond calculations and projections.

Planning for retirement often raises questions that go beyond personal finances, from understanding cost-of-living trends to navigating longevity.

We bring together external articles that are useful for building a broader understanding of retirement. These links are curated to help you stay informed and deepen your knowledge as you plan for the years ahead.*

* Links provided are for general information and eduational purposes only.

Many retirement systems were built for shorter life spans and stable income patterns. These assumptions have evolved.

When retirement systems fall short, the effects can place strain on families and public support systems. Strong retirement systems require intentional design to support longer lives and sustainable income.

At Manulife Investments, our role extends beyond asset management to supporting more resilient retirement outcomes over time.

![]()

©1999 - 2026 Manulife Investment Management (M) Berhad (Registration No. 200801033087 (834424-U))