10 September, 2019

Have you ever listened to songs from your music playlist and thought, “Not again!”? If you have experienced this, you are probably showing signs of fatigue. The same analogy can be used for income-seeking investors who are exploring opportunities beyond their current portfolios, typically comprising high-yielding equities and government bonds.

With rates expected to stay low for longer, where else can investors look to generate sustainable and consistent income?

The good news is that beyond your current universe, there may be other types of income-generating investments that might potentially meet your financial goals. It is therefore an opportune time to review and refresh your income playlist.

First, let us understand what “income” really means.

Income is a return that doesn’t come from buying or selling assets. It can take the form of cash dividend, interest or coupon payments (these are the terms used for the money derived from different instruments) that you receive on a regular basis from the investments that you hold.

It is important to grasp a thorough understanding of the various sources of income, not just what you are familiar with (namely high-dividend equities and government bonds):

How to Set Smart and Effective Financial Goals

In previous episodes, we have explored creating a financial plan and establishing a budget that accounts for your current expenditure. The third step is to build a strategy that will help you accomplish either a short-term or a long-term financial goal. We will guide you on your path by providing financial goal examples and introducing SMART (specific, measurable, attainable, relevant, time-based) objectives that help clearly define what you want to achieve in the years ahead.

5 ways a budget plan can help you manage your finances

We all know approximately how much money we need each month. However, without a clear spending strategy, you could see a shortfall in savings, face a lack of day-to-day cash, or be caught off guard by unexpected costs. That’s why it’s important to have an effective budget plan that will give you control over your finances.

Portfolio Diversification: What it is and How it Works?

Dividend income from equities

Interest or coupon payment from bonds

Dividend from hybrid securities (e.g. preferred securities1 )

Dividend from Real Estate Investment Trusts (REITs), which by law must distribute their earnings to investors

Income from mutual funds in the above-mentioned instruments offering dividend distributions

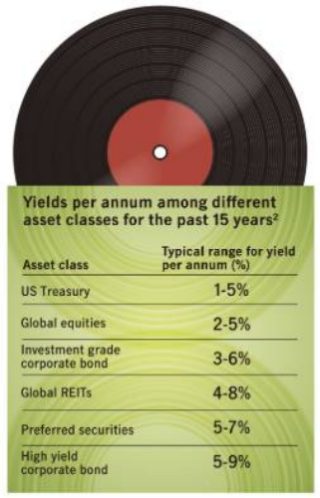

These sources of income can be obtained from multiple avenues, across both developed and emerging markets. The yield – which is essentially the annual income derived from an investment, expressed as a percentage of the investment's market value – can vary among different asset classes (see chart), depending on risk levels and the interest rate environment.

The asset classes in the chart below typically distribute income on a regular basis (either monthly, quarterly or semi-annually) during your investment holding period.

As every investment offers both risks and rewards, there is no right or wrong investment to include in your income playlist.

However, it is important to bear in mind that yields should not be the be-all-end-all criteria in your decision-making. After all, each source of income has its own risk-reward profile, and may not be suitable for everyone.

Here are some useful considerations:

Risk tolerance and income target: What is your risk appetite? Would you allocate more money to relatively more conservative investments in exchange for lower income? Or do you have a more aggressive personality to chase after higher income and take on more risks? Bear in mind that a higher yield target may increase your risk exposure.

Correlation among assets: In general, the lower the correlation between the price movements of the different assets in your portfolio, the lower the risks. A classic example is the relationship between bonds and equities which broadly tend to move in opposite directions.

Liquidity of assets: When and how quickly do you need your income?

Continuous review and timely adjustments: As yields, market conditions and your risk appetite change over time, it is important to review and rebalance your portfolio from time to time.

Regardless of your investment goals, there are always merits to keeping an updated income playlist, particularly if you are:

A retiree seeking to enhance your regular income

An investor looking to reduce your portfolio risks amidst all the market volatility

An investor targeting to generate potentially higher yields in the current low-rate environment

1 Preferred securities are a hybrid of bonds and equities with features from both asset classes. Their bond attributes include a stated par value, regular interest payments and assigned credit ratings by rating agencies. Meanwhile, their common stock characteristics mean they can be perpetual or long-dated. Preferred securities also have a lower priority in capital structure than senior debt but have a higher priority than common stock. Issuers are usually large and highly regulated institutions and/or companies with high stable cash flows such as banks, utilities, and RealEstate Investment Trusts (REITs).

2 Source: Manulife Investment Management, Bloomberg, as of March 2019. Typical yield per annum is based on historical yields for past 15 years. US Treasury refers to 10-year US Treasury; Global Equities refer to MSCI World; Investment grade corporate bond refers to JPMorgan US Investment Grade; Global REITs refer to FTSE EPRA/NAREIT; Preferred securities refer to ICE BofAML Fixed Rate Preferred Securities Index; High yield corporate bond refers to JPMorgan Global High Yield Index. A positive distribution yield does not imply a positive return.

Manulife Investment Management is the global wealth and asset management segment of Manulife Financial Corporation. The information and/or analysis contained in this material have been compiled or derived from sources believed to be reliable at the time of writing but Manulife Investment Management does not make any representation as to their accuracy, correctness, usefulness or completeness and does not accept liability for any loss arising from the use hereof or the information and/or analysis contained herein. Neither Manulife Investment Management or its affiliates, nor any of their directors, officers or employees shall assume any liability or responsibility for any direct or indirect loss or damage or any other consequence of any person acting or not acting in reliance on the information contained herein.

This material was prepared solely for educational and informational purposes and does not constitute a recommendation, professional advice, an offer, solicitation or an invitation by or on behalf of Manulife Investment Management to any person to buy or sell any security. Nothing in this material constitutes financial, investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate to your individual circumstances, or otherwise constitutes a personal recommendation to you. Past performance is not an indication of future results. Investment involves risk. In considering any investment, if you are in doubt on the action to be taken, you should consult professional advisers.

Proprietary Information – Please note that this material must not be wholly or partially reproduced, distributed, circulated, disseminated, published or disclosed, in any form and for any purpose, to any third party without prior approval from Manulife Investment Management.

These materials have not been reviewed by, are not registered with any securities or other regulatory authority, and may, where appropriate, be distributed by the following Manulife entities in their respective jurisdictions.

Malaysia: Manulife Investment Management (M) Berhad 200801033087 (834424-U). Singapore: Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration Number: 200709952G). Philippines: Manulife Asset Management and Trust Corporation. Australia, South Korea and Hong Kong: Manulife Investment Management (Hong Kong) Limited in Hong Kong and has not been reviewed by the HK Securities and Futures Commission (SFC).

Making your money work for you

Inflation: the unseen tax that gradually erodes investors’ purchasing power

How to Set Smart and Effective Financial Goals

In previous episodes, we have explored creating a financial plan and establishing a budget that accounts for your current expenditure. The third step is to build a strategy that will help you accomplish either a short-term or a long-term financial goal. We will guide you on your path by providing financial goal examples and introducing SMART (specific, measurable, attainable, relevant, time-based) objectives that help clearly define what you want to achieve in the years ahead.

5 ways a budget plan can help you manage your finances

We all know approximately how much money we need each month. However, without a clear spending strategy, you could see a shortfall in savings, face a lack of day-to-day cash, or be caught off guard by unexpected costs. That’s why it’s important to have an effective budget plan that will give you control over your finances.

![]()

©1999 - 2026 Manulife Investment Management (M) Berhad (Registration No. 200801033087 (834424-U))