15 June 2023

Kai Kong Chay, Senior Portfolio Manager, Greater China Equities

Greater China stock markets experienced an impressive rebound on cyclical drivers such as China’s reopening and economic re-acceleration. In this Q&A, Kai Kong Chay, Senior Portfolio Manager, Greater China Equities, highlights the secular growth themes and puts some top-of-mind queries into perspective.

As we highlighted earlier this year, the service sector's recovery should be the most significant development to emerge from China’s reopening. As it evolves, consumption-related plays are fuelled by recovery and reopening dynamics across sectors1. Before the government’s official announcement in Q4 2022, as active managers, we were already positioned in a variety of sub-sectors that went on to benefit from China’s re-opening, including i) online platform companies, ii) hospitality (online travel agencies and hotels), iii) healthcare names (medical devices and equipment). These investments delivered positive returns in the Q1 2023 rally. We also selectively took profits in some consumer names, e.g., luxury retailers, Macau gaming, and duty-free companies.

We continue to believe that various consumption-related sectors, e.g., e-commerce, hospitality, and domestic sportswear brands, may ride on a potentially sustainable recovery into the second half of this year on the back of higher demand, better pricing, and volume growth.

We had also expected that a strong rebound in consumption would trigger investment appetite. In fact, the reopening accelerates the pace of digitalisation of traditional industries, and our positions in innovation-related themes, such as application software, semiconductors, and online gaming, are well supported in this rally.

Global manufacturing GDP of around US$14.2 trillion in 2021 was underpinned by thousands of companies in traditional industries2. Nowadays, goods are not merely from traditional industries; they could include electric vehicles (EVs), semiconductor products and innovative software/hardware products that call for a new and diversified supply chain.

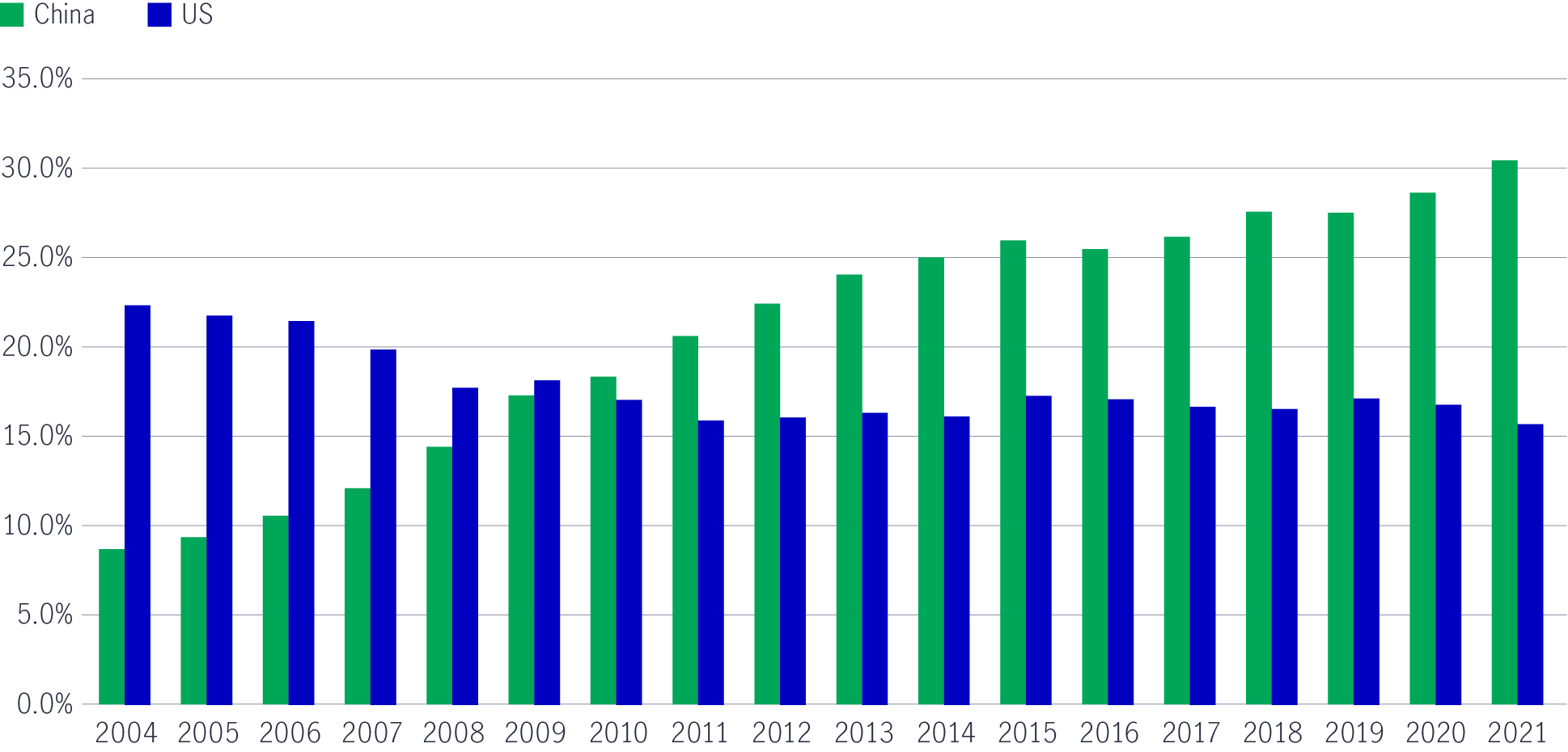

China’s approximately US$4.9 trillion manufacturing economy ranked the largest (over 30%) globally in 2021, vs US and Europe (about 16% each). Despite China’s sheer size and dominance, its manufacturing GDP (in local-currency terms) still showed growth momentum, which rose by 9.8% YoY and 7.0% YoY in 2020-21/2021-22, respectively3.

Besides, when we look at China, it is now emerging as the single largest market for industrial original equipment manufacturers (OEMs)4, as these companies grow their presence in China not only because of its manufacturing capabilities but also due to market proximity and onshore customer needs. We believe the linkages between China’s manufacturing supply chain and the rest of the world are still strong.

We acknowledge the scenario whereby more supply chains were moving out or finding a replacement for China in the past few years due to geopolitical tensions, COVID-19 disruption, and rising labour costs. Indeed, multi-national companies (MNCs) have been rethinking the two-decade production models (“Made in China”) and advocate the “China+1” model to avoid overconcentration in China’s production lines, to diversify business lines and reduce risk.

Besides MNCs, we see Chinese exporters becoming more internationalised by forging the same path as Japanese and South Korean companies: they are building plants and shifting production bases offshore5 to hedge against rising local labour/environmental costs and growing geopolitical risks so clients can place orders in a third country. For example, it’s reported that furniture companies are moving to Mexico, as are large home appliance and car manufacturers, in order to serve customers in the United States and take advantage of a 2020 North American trade deal6. Ultimately, these Chinese exporters’ goods (“Made by China”) will be labelled as “Made in Mexico”.

Another example is consumer electronics. An international smartphone operator expanded its production lines to India via its Chinese contract manufacturers under India’s Production Linked Incentive (PLI) Scheme. These smartphones are made by Chinese manufacturers in India and will be labelled as “Made in India”.

As highlighted in our 2023 outlook, China has focused on supply chains that drive technology innovation/localisation and manufacturing upgrades. In fact, China had not lost any ground in global manufacturing as of 2021 (refer to Chart 1). China may lose market share in the supply chains of low-tech industries like textiles and footwear to Vietnam and Thailand while gaining a larger share of more sophisticated sectors such as EV and batteries exports.

Chart 1: China’s global manufacturing share still shows growth momentum

Source: World Bank Data, Morgan Stanley Research, as of 1 May 2023. Percentage figure represents China and US’s contribution to global manufacturing GDP.

Furthermore, China is adapting to supply-chain changes by moving up the quality scale in EV production. The country is self-reliant in the EV battery supply chain, and it’s estimated that China-made EV battery volume is more than double that of every other country combined7. China’s complete EV supply chain spans mining rare raw materials (cobalt, nickel), processing and refining (with government support in the form of cheaper land and labour), component manufacturing and battery assembly. Most global companies would need to partner with Chinese component manufacturers to enter or expand in the EV industry.

As mentioned earlier, businesses such as international OEMs, are unlikely to move their entire supply chains out of China, given the country is often their single largest market. Instead, they need to maintain access and strike a balance between customer proximity and manufacturing location. The manufacturing universe is also highly interconnected, and logistics must be managed to control costs. For example, around 45%8 of car parts and components used by auto firms in the US and Europe have, at some stage, moved in and out of China.

We also believe that technology-savvy domestic auto suppliers will likely gain market share on the back of localisation efforts in China. Instead of sourcing their components elsewhere, international OEMs may need to increase their reliance on China-based suppliers.

In addition to boosting middle-class consumption and becoming more self-reliant, China must focus on business-model innovation, technology localisation and advanced manufacturing. Our team has identified opportunities in the automation and artificial intelligence (AI) space:

1) Automation is a fast-growing area that rides on the trend of labour replacement owing to i) rising wages and labour shortages on ageing populations, and ii) the rapid expansion of emerging end markets such as consumer electronics, automobiles, batteries, solar/semiconductors.

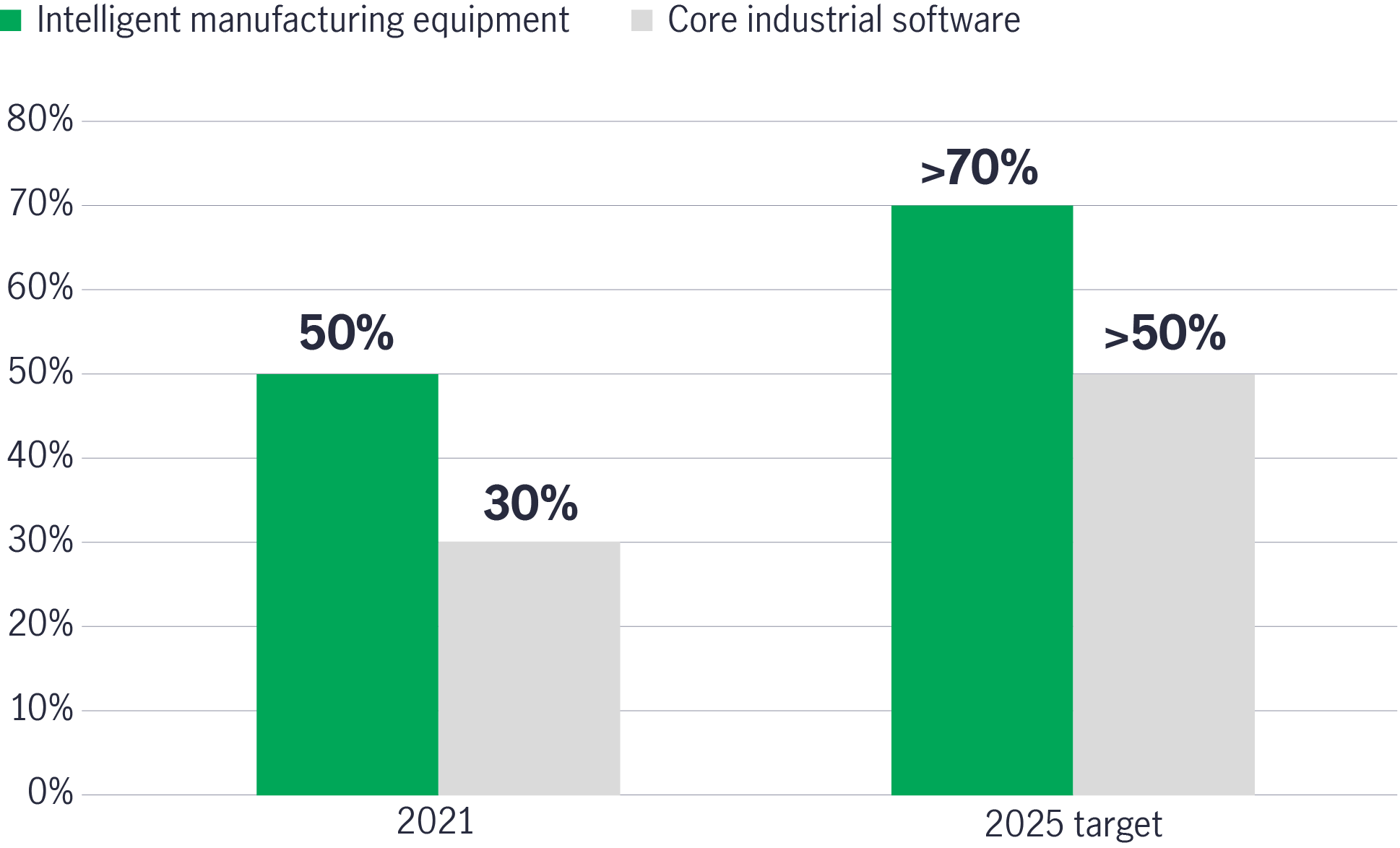

Chart 2: China’s self-sufficiency rate in automation products (2021 vs. 2025)

Source: Ministry of Industry and Information Technology, as of August 2022.

Amid the push for greater technological self-sufficiency, China has set a goal of doubling industrial robot density from 2020 to 2025. We expect domestic leaders in industrial robots to benefit from the trend as they possess the industry know-how in local markets and understand import substitution demand from customers in China.

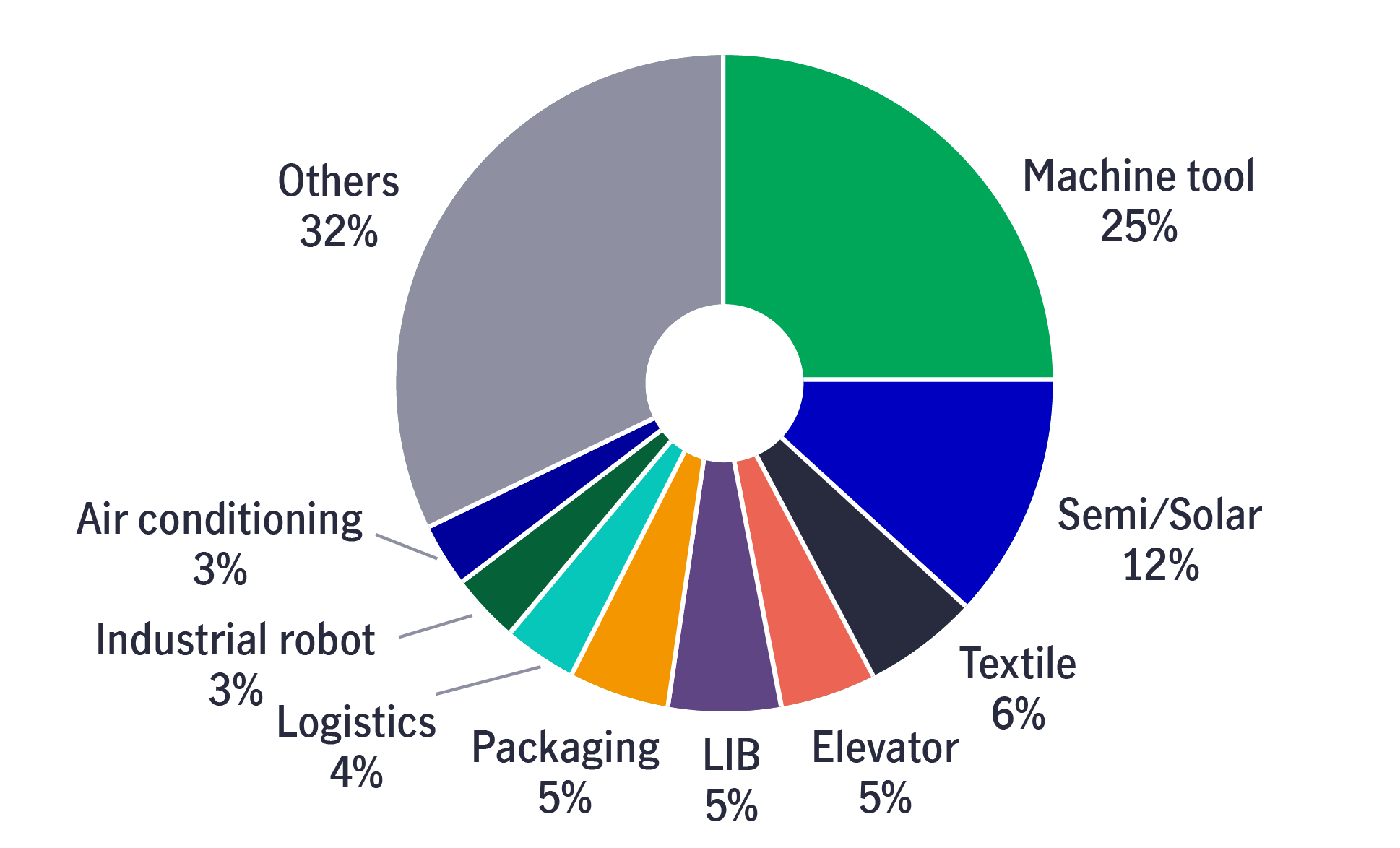

In a broad sense, automation can be sub-categorised into factory and process automation. Within China, 41% of the automation market is factory automation9 (also known as discrete automation), whereas process automation represents the remainder, i.e., 59%.

Chart 3: China’s factory automation sales by downstream area (2021)

Source: MIR Databank, HSBC Qianhai Securities, as of August 2022.

In terms of the sales breakdown (by industry) for factory automation in 2021, machine tools represented 25% of the total, followed by semiconductor & solar (12%), textiles (6%), elevators (5%), and lithium batteries (LIB) (5%).

We believe that industrial robotic manufacturers with leading market positioning, vertical integration capabilities, and margin improvement potential for localised components could outperform. We expect improving new-order flows as industrial capex picks up.

2) AI: According to International Data Corporation (IDC), global revenue for the AI market, including software, hardware, and service sales, is expected to increase at a CAGR (2022-2026) of 19% to reach US$900 billion by 2026. China’s AI investment is expected to reach US$26.69 billion by 202610, accounting for 8.9% of global investment.

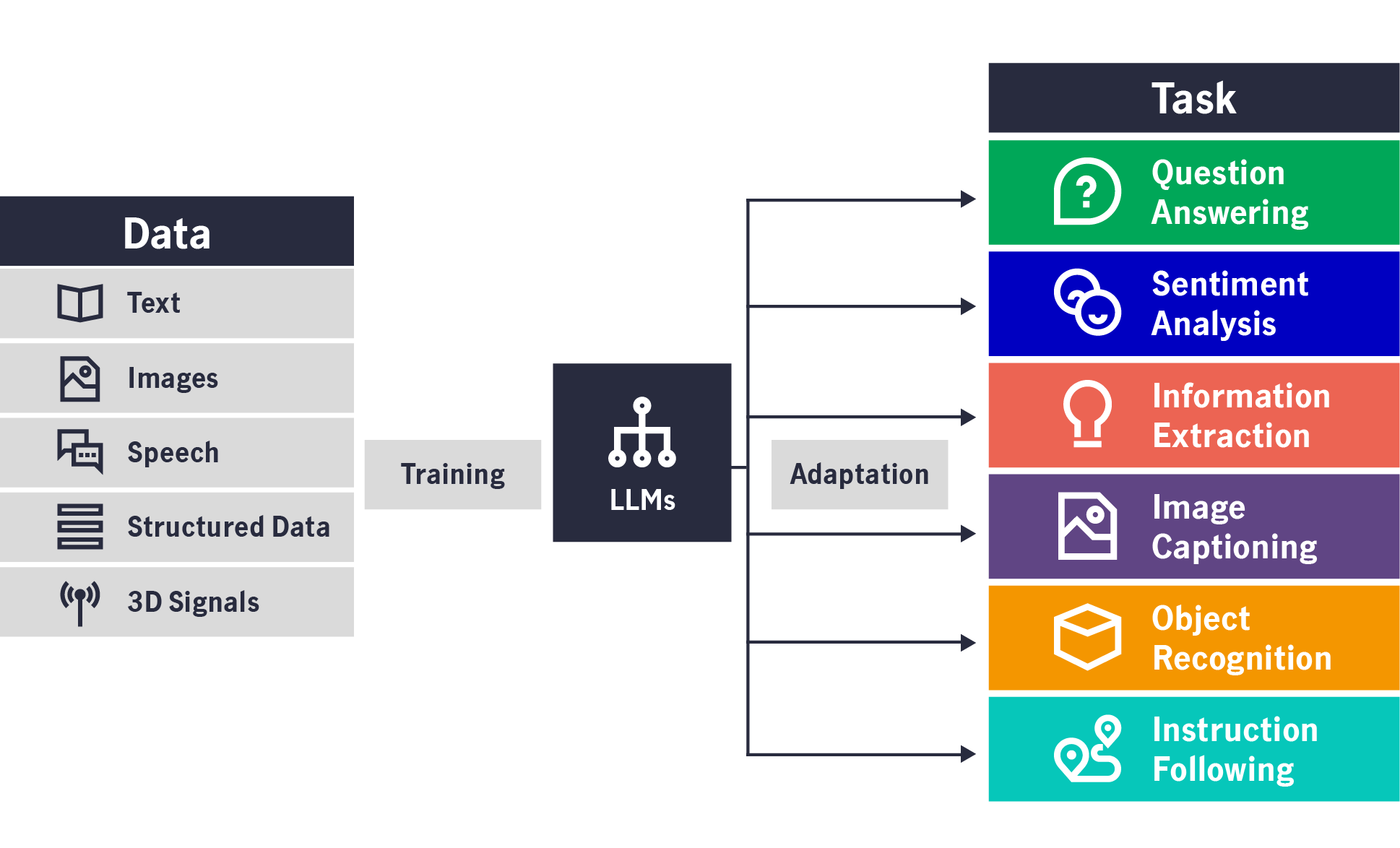

Large language models (LLMs) (also known as Foundation Models) use deep learning in natural language processing (NLP). An LLM is a transformer-based neural network that predicts the text that is likely to come next. The development of LLMs is significant as it can adapt to a wide range of tasks.

On the regulatory front, the Cyberspace Administration of China (CAC) drafted measures to manage generative AI services and encourage the use of safe and reliable software, tools and data resources11. This echoes President Xi Jinping’s call to develop AI technology amid the race with the US and reflects the government’s objective of building its own governance universe.

Within the AI supply chain, we believe that Mainland China hardware and software companies as well as Taiwanese hardware firms exposed to AI infrastructure, components and applications could benefit.

In terms of hardware requirements, semiconductors and networking infrastructure are expecting a boom from AI training and interface perspectives. Major components required for a machine learning model include i) logic processors (i.e., to perform parallel computations), ii) memory (especially with DRAM with high bandwidth), and iii) networking equipment (e.g., switches and routers to link servers to cloud/edge devices). For software, China’s internet giants and start-ups have started to develop homegrown OpenAI capabilities, e.g., the integration of AI into web browsers, customer messaging tools, education software, industrial software for the retail and finance industries, and online gaming.

We believe that software leaders with significant customer bases could benefit from subscription-based revenues derived from future AI applications. Content creators and advertising platforms have already started using AI to improve efficiency and lower development costs.

Chart 4: LLMs (Foundation Models): what are they good for?

Source: Center for Research on Foundation Models (CRFN), Stanford University Institute for Human Cantered Artificial Intelligence. LLMs can centralize information from several data modalities to adapt to a wide range of tasks from answering questions, to extracting information and identifying images. For illustrative purposes only.

Overall, we expect China’s service-led economic recovery to continue throughout 2023. We also believe that i) improving retail sales, ii) property market stabilisation, and iii) reducing regulatory headwinds for sub-sectors (e.g., online gaming), the promotion of AI development and support for the platform economy are all encouraging.

China is adapting to supply-chain changes and moving up the manufacturing quality scale. With rising demand for advanced manufacturing, domestic automation suppliers will likely gain market share.

The technology localisation trend remains intact. We believe, AI/software, semiconductor equipment, and hardware technology companies with strong R&D capability should thrive and gain market share. Selective gaming companies should see better top-line growth on the back of gaming approvals.

1 National Bureau of Statistics in China, Bloomberg, as of 18 April 2023: domestic demand for goods and services rebounded and drove up retail sales; Ministry of Culture and Tourism, as of 6 April 2023: domestic tourism (leisure and business) has rebounded to over 80% of 2019 levels.

2 Morgan Stanley. Traditional industries include automotive, aerospace, energy, food & beverage through to consumer appliances, furniture, and textiles.

3 Morgan Stanley Research.

4 Morgan Stanley Research.

5 China’s Ministry of Commerce. As of end-2020, the foreign direct investment (FDI) from China in Mexico totally amounted to approximately US$1.17 billion.

6 U.S. – Mexico – Canada Agreement (USMCA), 15 May 2023.

7 Estimates from Benchmark Minerals, a consulting group.

8 Morgan Stanley Research.

9 HSBC Qianhai Securities, data as of 2021. Process automation refers to the product of a continuous stream of products, e.g., chemicals, power, steel, refineries, etc. which typically needs more software than factory automation given the data analysis required. Both factory automation and process automation will require control systems. Also, process automation is typically project-based whereas factory automation is usually OEM-based.

10 IDC CHINA –2023 China AI Market Spending forecast, 29 March 2023.

11 Reuters, 11 April 2023.

Asset allocation views on SpaceX IPO, Reopening of Strait of Hormuz, and the BOJ rate hike

The Multi Asset Solutions Team (MAST) provides asset allocation views on three recent developments that could influence markets in different ways: the SpaceX Initial Public Offerings (IPO), the reopening of the Strait of Hormuz, and the Bank of Japan’s (BOJ) rate hike. In our view, these events create mixed signals across growth, inflation and liquidity. Overall, the backdrop still appears uneven, and this may support a measured and selective approach to asset allocation rather than a broad increase in risk.

Not another bubble: How semiconductors are powering a real future

Semiconductors sit behind almost every modern experience – from smartphones and cars to cloud computing and today’s AI tools – yet they remain largely invisible to most people. They are more than chips only, and the demand is being supported by several long-term forces. We believe that today’s semiconductor excitement is not a repeat of the dot-com bubble, as investment is tied to real infrastructure and revenue-generating services. And the opportunity is broader than a handful of headline AI names.

Global tech and semiconductors: what’s been driving returns and what to watch next

Semiconductors have been one of the strongest parts of global equity markets so far in 2026, with performance supported by a powerful mix of demand and improving fundamentals. The headlines have focused on artificial intelligence (AI), but the opportunity set is broader than a single theme or a handful of companies. As AI infrastructure expands, it is driving investment not only in high-performance computing chips, but also in the networking and power technologies that keep modern data centres running. At the same time, parts of the industry outside AI are showing early signs of stabilisation and recovery.

![]()

©1999 - 2026 Manulife Investment Management (M) Berhad (Registration No. 200801033087 (834424-U))