18 January 2022

Paula Chan, Senior Portfolio Manager, Asia Fixed Income

Isaac Meng, Portfolio Manager, Asia Fixed Income

As global inflation trends higher, investors would like to look for potential hedges against the erosion of real returns. In this investment note, Paula Chan (Senior Portfolio Manager, Asia Fixed Income) and Isaac Meng (Portfolio Manager, Asia Fixed Income) outline their key observations and explain why they think China government bonds and the Chinese renminbi (CNY) have the potential to act as hedges against US inflation.

According to conventional wisdom, there is a belief that US inflationary pressures can be negative for the Chinese yuan (CNY). This is because, historically, US inflationary pressures have led the Federal Reserve to tighten monetary policy, and US Treasury yields then to move higher as investors became concerned about inflation. Consequently, the yield advantage of China’s interest rates over US Treasury yields would narrow, as the latter rises while the former remains stable. The yield advantage of China bonds has been one of the key drivers for global investors to invest in China bonds, which has helped the CNY to appreciate. Therefore, if the yield differential declines, investors could pull funds away from China bonds leading to a weaker CNY against the US dollar.

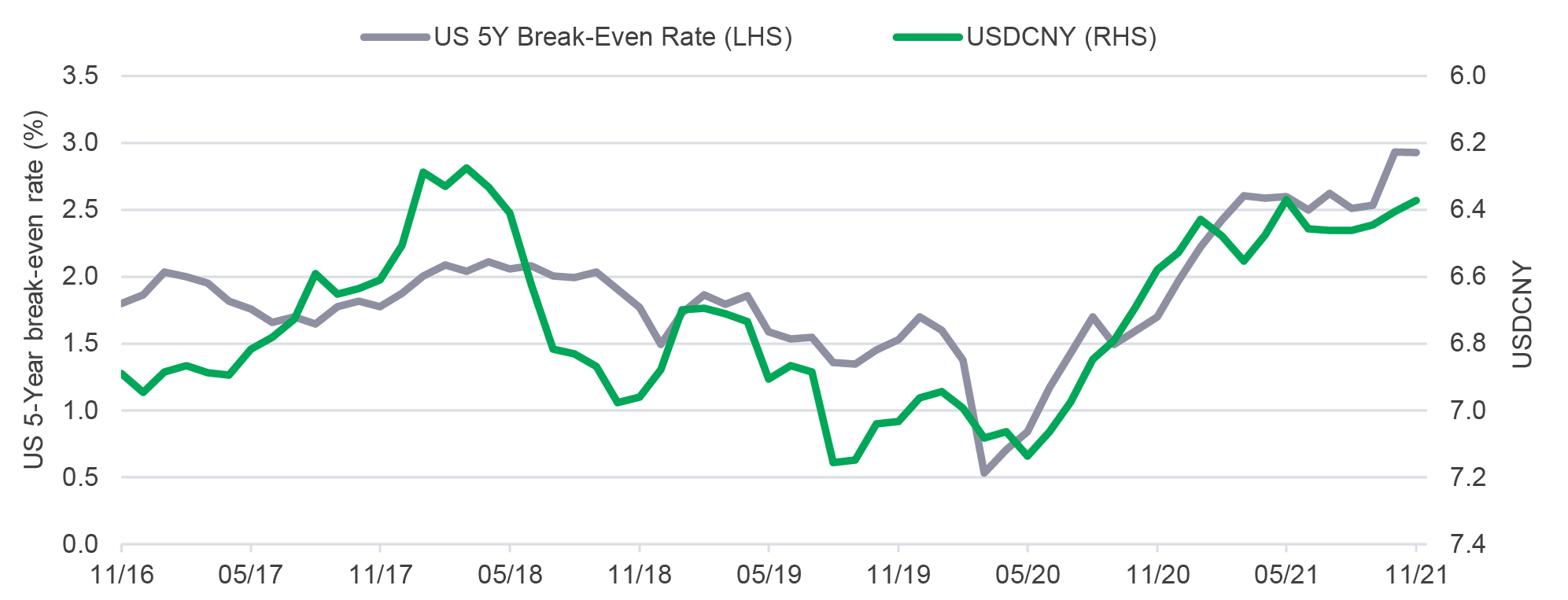

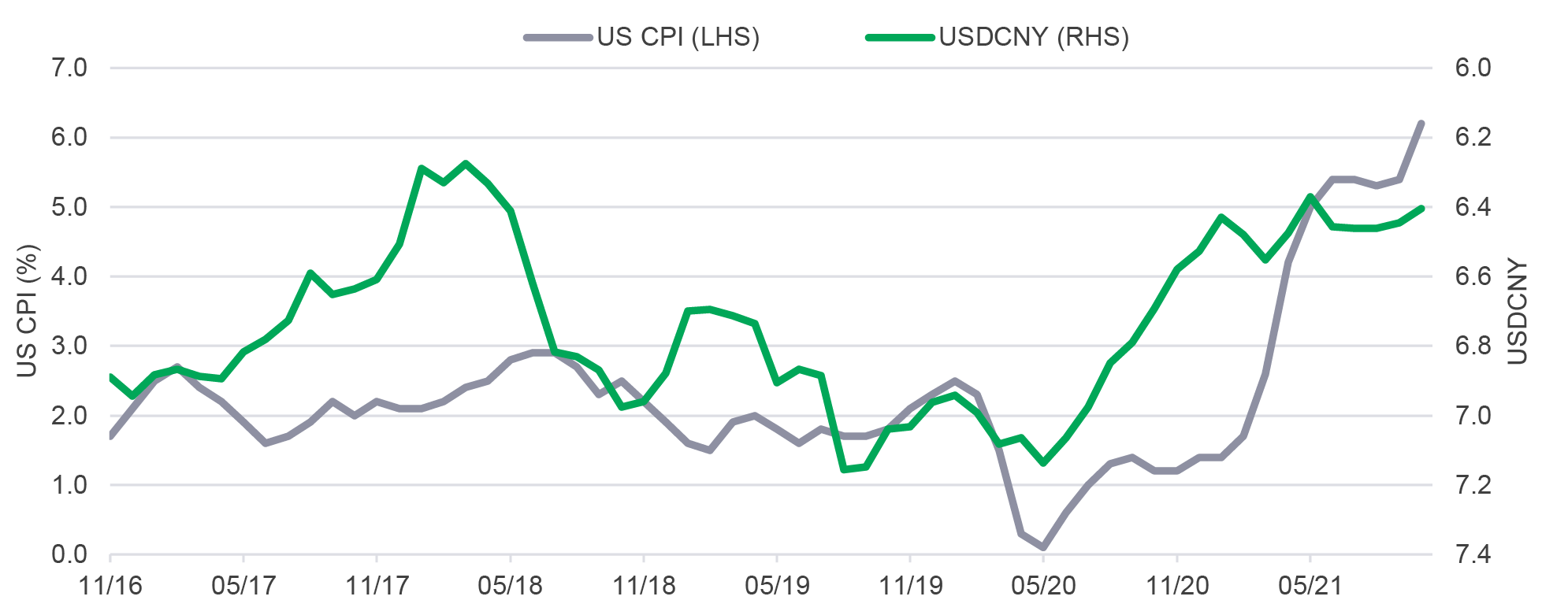

Contrary to the above expectations, we have noticed that US inflationary pressures did not necessarily lead to an underperformance in the CNY. In fact, the two charts below show that the CNY had tracked US inflationary pressures quite closely, as indicated by US 5-Year breakeven rates, which is a gauge of the market’s expectations for US inflation (Chart 1). Meanwhile, the CNY had also tracked the official annual US CPI rate on an ex-post basis (Chart 2). Both charts tell us that as US inflation ticked higher, the CNY appreciated against the US dollar during these periods.

Chart 1: CNY appreciated against USD as US inflationary expectation (US 5-year break-even rates) moved higher

Bloomberg, data as of 30 November 2021.

Chart 2: CNY appreciated against USD as US inflationary (official annual CPI) moved higher

Bloomberg, data as of 31 October 2021.

Thinking this through, we believe it could make sense for China onshore bonds (and the CNY) to be a positive-yielding hedge against inflationary pressures due to the following reasons:

In response to the global pandemic, the US Federal Reserve has been dovish and is still expanding its balance sheet well into the first quarter of 2022 despite tapering. Even with the market pricing in +0.75% in rate hikes for 2022, negative US real rates will prevail with CPI running above 5%.

We believe higher US inflation may not be transitory in nature that only reflects temporary supply shocks. Rather, higher inflation is likely a consequence of stronger US demand and goods consumption. Higher consumption and imports in the US are positive contributors to China’s trade surplus which is positive for the CNY.

With US inflation currently outpacing China inflation, the value of the CNY (in real terms) is likely to be closer to fair value compared with the US dollar. The latter is more likely to be overvalued due to its higher inflation based on the real effective exchange rate (REER). The REER is a measure of a currency’s value against those of its major trading partners after adjusting for inflation.

A market environment with higher breakeven rates and low-to-negative real yields is generally associated with a “risk-on” mode, i.e., global investors are more likely to allocate away from US Treasuries to higher-risk asset classes in this environment. Hence, on this basis, a greater allocation to CNY assets can be expected.

As inflation has ramped up in the last 12 months, we have seen US Treasury inflation-linked bonds outperform US Treasuries over this time. Similarly, China bonds (unhedged) have performed strongly and kept pace with the performance of US Treasury Inflation-linked bonds over the same period, giving support to our thesis that China bonds can provide investors with a hedge against US inflation.

Chart 3: 5-year returns of China bonds (unhedged) vs. US Treasury inflation-linked bonds

Bloomberg, data as of 30 November 2021.

We have highlighted some of our key observations and explained why we think China government bonds and the CNY Chinese renminbi have the potential to act as hedges against US inflation. China bonds are already an attractive asset class, given their higher nominal and real yields and diversification benefits due to a lower correlation with other assets. However, the potential for China bonds to be a positive-yielding asset that also hedges against rising global inflation further enhances their appeal. We believe there is now an even stronger case for considering China bonds as a key part of global investors’ portfolios.

Q2 2025 Malaysia Market Outlook: Trade Tensions and Market Volatility

Market Flash: Impact of US Tariffs on Malaysia

Read moreQ1 2025 Malaysia Market Outlook: Equity, Fixed Income and Economic Trends

Q2 2025 Malaysia Market Outlook: Trade Tensions and Market Volatility

Market Flash: Impact of US Tariffs on Malaysia

Read moreQ1 2025 Malaysia Market Outlook: Equity, Fixed Income and Economic Trends

![]()

©1999 - 2026 Manulife Investment Management (M) Berhad (Registration No. 200801033087 (834424-U))