Q4 2022 has been a turbulent quarter for the global economy, rallying with hope and optimism and slumping back down when any shred of uncertainty emerges. Concerns over recession, monetary policies, China’s zero-COVID policy and the residual impact of Russia’s invasion of Ukraine remains. Some of these concerns had begun loosening their grip, while others continue to hang on tightly to the global economy.

The battle against stubborn inflation continues as central banks across the globe went on the offensive, unleashing numerous rounds of attacks in the form of aggressive interest rate hikes. The US Fed was at the forefront of the battle once again, having raised its benchmark interest rates seven (7) times in 2022 with a staggering 425 basis points (bps) in totality, bringing its target range to the 4.25% - 4.50% by the end of the year. The US Fed is accompanied by many other central banks, each implementing their very own form of aggressive monetary policy convention.

Efforts appeared to have paid off as inflation peaked in Q3 2022; Year-on-year (YoY) headline inflation in the US moderated close to the 7% handle in October and November 2022, coming off its 40-year high of 9.1% reported in June 2022. This slowdown in inflation was a shout of joy for markets, raising speculation of a possible softening of aggressive monetary policies by central banks worldwide. Given an improving global inflation backdrop, markets were offered a short respite, bolstering optimism, and setting the stage for risk assets to rebound and bond yields to fall in November 2022. During this period, the risk-sensitive US S&P500 and the MSCI Asia Ex Japan Index rebounded by a whopping 5.4% and 18.7% month-on-month (MoM) respectively, while the UST yield curve bull flattened, with the 2-year yields changing by -17bps, 5-year and 10-year yields changing by over -40bps for the month of November 2022 itself. Contrastingly, as risk sentiment improved, the US Dollar’s relative safe-haven status was dented, with the DXY suffering a 5.0% fall within the same period.

The upturn in the market proved to be short-lived as the US Fed, in their latest December 2022 meeting made clear that interest rates are expected to lift higher in 2023, towards a terminal rate of 5.1%, likely without any reductions until 2024. Shifts in the US Fed’s tone, inflation direction and continued geopolitical tensions between Russia and Ukraine increased uncertainty and volatility in the market, while exacerbating concerns for a quickly weakening global economy that is in danger of slipping into recession. Under these circumstances, the International Monetary Fund (IMF) warned of a “tough” year ahead in 2023, with one-third of the world’s economies expected to fall in recession, while slashing global GDP forecasts to 2.7%1, representing the weakest growth profile since 20012.

Over in China, policymakers backpedalled on their strict 3-year-old zero-Covid policy after announcing a slew of easing measures. On the 8th of January 2023, Chinese authorities will officially downgrade the management of COVID-19 to a “Category B”. This crucial step permits quarantine-free travelling and home isolation for COVID patients with mild or no symptoms. At the shorter end of the stick, China’s “Great Reopening” would bring challenges to its healthcare system as COVID cases are expected to surge with increased mobility. At the time of writing, COVID is affecting roughly about 37 million people a day in China3.

For Malaysia, November 2022 set off a new beginning for the nation, coming out fresh off its 15th General Elections, resulting in the appointment of Datuk Seri Anwar Ibrahim as the 10th Prime Minister, leading a newly formed unity government. During the month of Anwar’s appointment, the MYR was one of the best performing currencies in the region, strengthening by a massive 6.0% versus the USD. Simultaneously, Malaysia’s robust domestic demand and resilient exports fuelled a remarkable Q3 2022 YoY GDP growth of 14.2% (consensus estimates: 11.7%). Headline inflation came in at 4.0% YoY in both October and November 2022, signalling easing inflation pressure relative to 2Q 2022.

Equity market

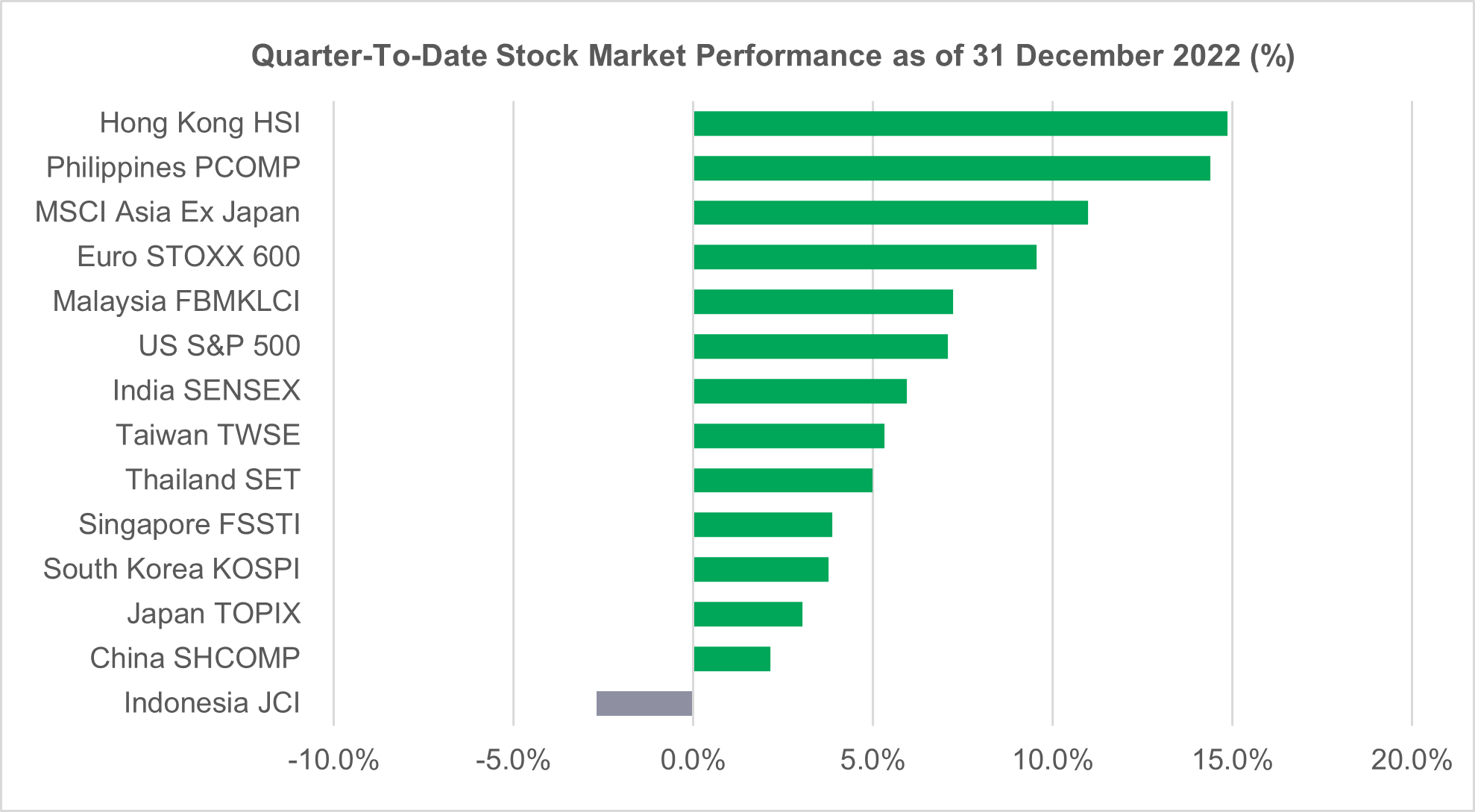

Overall, most stock indexes achieved robust gains, ending the period of Q4 2022 in positive territory. Major gains were recorded in the month of October and November 2022 as optimism over inflation reignited hopes of a possible shift towards a less hawkish rhetoric by central banks globally, moving into 2023. Hong Kong’s Hang Seng Index triumphed over the rest, returning +14.9% quarter-on-quarter (QoQ), boosted by The People’s Bank of China’s (PBoC) efforts in supporting the Chinese economy as it emerges from the crypts of COVID-19 in 2023. Finishing after them is Philippines’ PCOMP (+14.4% QoQ), attracting strong positive foreign inflows, led by bargain hunting of interest rate-sensitive sectors such as property.

Indonesia’s JCI (-2.7% QoQ) was the only index that had performed negatively in the region in Q4 2022. Losses were primarily led by energy and financial stocks, bearing the brunt of weaker energy prices and a rising interest rate environment. Finishing just above them are China’s SHCOMP (+2.1%), having erased some of its gains made in November 2022 as the region is afflicted with a fresh COVID-19 wave in December.

In the local market, performance of the FBMKLCI held up, etching up a stellar +7.2% performance in Q4 2022. Similar to its regional peers, major gains were recorded in the month of October and November 2022 sparked by expectations of a less aggressive monetary policy regime by central banks worldwide as inflation eases. Additionally, dust has also settled in Malaysia’s political arena following increasingly positive sentiment surrounding Datuk Seri Anwar Ibrahim’s appointment as Prime Minister. The Malaysian equity market finished off the year with remarkably strong foreign inflows in year 2022 –foreign investors were net buyers with total net inflows of RM4.38 billion, for 27 out of the 52 weeks of 20224.

Throughout 2022, Energy, Plantation and Financial Services sector were evidently the best performing sectors, benefiting from strong commodity prices and a rising interest rate environment – for the same reason placing the Technology sector as the main detractor of the year as its future earnings potential are derailed by rising rates.

In the broader market, the FBM 100 Index, together with the FBM Small Cap Index generated gains in line with the FBMKLCI as well – returning +7.1% QoQ and +8.8% QoQ respectively.

Moving into 2023, global markets are expected to remain volatile and will be influenced by the direction of US inflation, interest rates and geopolitical developments. Hence, we will continue to adopt a balanced portfolio in the Malaysian Equity space while looking to bottom-fish on stocks which have fallen significantly in 2022, with a preference to stocks which have secular growth potential over the long term. Our current portfolio strategy will be centred around attractively valued dividend-paying stocks with firm fundamentals.

Source: Bloomberg, as of 31 December 2022

Fixed income market

Q4 2022 was a whirlwind of a quarter for the US Treasury (UST) yields. Overall, the 2-year, 5-year and 10-year UST yields changed +15bps, -9bps and +5bps, to close at 4.43%, 4.00% and 3.87% respectively. UST yields declined after peaking in early November, dictated by both easing inflation and speculation of possible change in the US Fed’s monetary policy stance. Inversion of the 2-year and 10-year UST yields deepened to levels unseen since the 1980s.

In the Asian Dollar Bond Market, both investment grade and high yielders rallied, following PBoC’s liquidity support announcement, unveiling a 16-point plan to rescue cash-strapped property developers. Gains held on as the year ended as market braced for “The Great Chinese Reopening” in 2023. Investment grade and high yield Asian Dollar bonds returned +2.64% and +12.60%5 respectively.

For the local market, Malaysian Government Securities (MGS) yield curve bull flattened in Q4 2022; 3-year, 5-year and 10-year MGS yields changed -11bps, -23bps and -37bps respectively to close the year at 3.78%, 4.08% and 4.46%. The rally in the Malaysian bond market is widely attributed to the global expectation of a softer pace of monetary policy tightening, coupled with an improving local political landscape.

BNM raised the Overnight Policy Rates for the 4th time in 4Q 2022, bringing rates to end the year at 2.75%. Market pencilled in another 50bps rate hike in 2023 though we believe that it is near the tail end of BNM’s rate hiking cycle.

In general, we are turning more positive on the outlook of MGS as global inflation showed signs of peaking and global growth looks set to slow. That said, we still expect heightened market volatility due to uncertainty over changes to Fed’s stance, the impact of China reopening and the full extent of global slowdown. Persistent geopolitical tensions in relation to the Russia-Ukraine conflict and US-China tech war add to the growing uncertainty. To this end, we remain cautious on the market and expect choppy trading environment in the near term.

Download full PDF View key takeaways

Source:

1International Monetary Fund, “World Economic Outlook Report”, October 2022

2With the exception of the Global Financial Crisis & the acute phase of the COVID-19 pandemic

3Bloomberg News, “China Estimates COVID Surge Is Infecting 37 Million People A Day”, 23 December 2022

4MIDF Research, as of 30 December 2022

5Bloomberg, as of 31 December 2022. Based on Bloomberg Asia USD Investment Grade Bond Index & Bloomberg Asia USD High Yield Bond Index

2026 Outlook: Clearer picture, better growth

This year’s outlook spotlights a world in flux – U.S. stimulus, Europe’s rebound, China’s policy pivots, and Japan’s innovation surge all shape a landscape full of both opportunities and challenges.

2026 Asian Fixed Income Outlook: Positive momentum poised to continue amid ample investment opportunities

Asian fixed income posted strong gains in 2025 amid myriad challenges. Entering the new year, the asset class is poised for continued momentum on the back of numerous beneficial tailwinds. In this 2026 Outlook, the Asian Fixed Income team analyses the key factors likely to propel performance and identifies opportunities for investors based on key themes and developments in three regional bond markets: China, Japan, and India.

2026 Global Macroeconomic Outlook: clearer picture, better growth

Our 2026 macro outlook highlights key themes across global economies and commodities, what we'll be watching closely in the new year, and portfolio takeaways for investors to consider.

2026 Outlook: Clearer picture, better growth

This year’s outlook spotlights a world in flux – U.S. stimulus, Europe’s rebound, China’s policy pivots, and Japan’s innovation surge all shape a landscape full of both opportunities and challenges.

2026 Asian Fixed Income Outlook: Positive momentum poised to continue amid ample investment opportunities

Asian fixed income posted strong gains in 2025 amid myriad challenges. Entering the new year, the asset class is poised for continued momentum on the back of numerous beneficial tailwinds. In this 2026 Outlook, the Asian Fixed Income team analyses the key factors likely to propel performance and identifies opportunities for investors based on key themes and developments in three regional bond markets: China, Japan, and India.

2026 Global Macroeconomic Outlook: clearer picture, better growth

Our 2026 macro outlook highlights key themes across global economies and commodities, what we'll be watching closely in the new year, and portfolio takeaways for investors to consider.

![]()

©1999 - 2026 Manulife Investment Management (M) Berhad (Registration No. 200801033087 (834424-U))