In Q1 2024, the US released a series of robust economic data, showcasing impressive job figures and a remarkable GDP print. This positive news significantly boosted market sentiment, leading to a strong start for global equity markets. As a result, all three major US stock indices soared to record-breaking new highs. Furthermore, February saw a massive rally in global technology stocks, driven by NVIDIA's outstanding earnings report. The strong economic data and labour market conditions, coupled with higher-than-expected inflation prints, reshaped market expectations on the timing and magnitude of US interest rate cuts, ultimately triggering a widespread selloff in global bond markets in the quarter.

Against this backdrop, oil prices surged to approximately $90/barrel due to OPEC+ output cuts and escalating tensions in the Middle East, heightening supply concerns. Simultaneously, the UK economy slipped into a technical recession after experiencing two consecutive quarters of negative GDP growth in the second half of 2023. In this environment of economic uncertainty, gold prices surged to new highs, marking an impressive 8.2% YTD increase by end of 1Q 2024. This upward trend was driven by gold's safe haven appeal and increased purchases by global central banks.

Over in China, Chinese Premier Li Qiang unveiled an ambitious 2024 economic growth target of around 5%, accompanied by a commitment to revamp the country's development model and mitigate risks stemming from distressed property developers and indebted cities. Meanwhile, in a bid to prop up the ailing Chinese property sector, PBoC slashed its 5-year loan prime rate by 25bps, reducing it from 4.20% to 3.95%.

In Malaysia, GDP expanded at a slower pace of 3% in Q4 2023, mainly attributed to declining exports, leading to an overall annual GDP growth of 3.7% for 2023. Looking ahead to 2024, GDP growth is expected to improve to 4% - 5%, driven by the recovery in exports and resilient domestic expenditure. Furthermore, headline inflation has remained well under 2% in both YoY January and February. Expectations for modest inflation throughout 2024 reflect stable cost and demand conditions. In Q1, Bank Negara Malaysia (BNM) maintained interest rates at 3.00%, implying that future decisions would remain data-dependent. Additionally, BNM reaffirmed its commitment to upholding the strength of the MYR and expressed readiness to intervene in response to its recent weakness against the USD.

Equity market

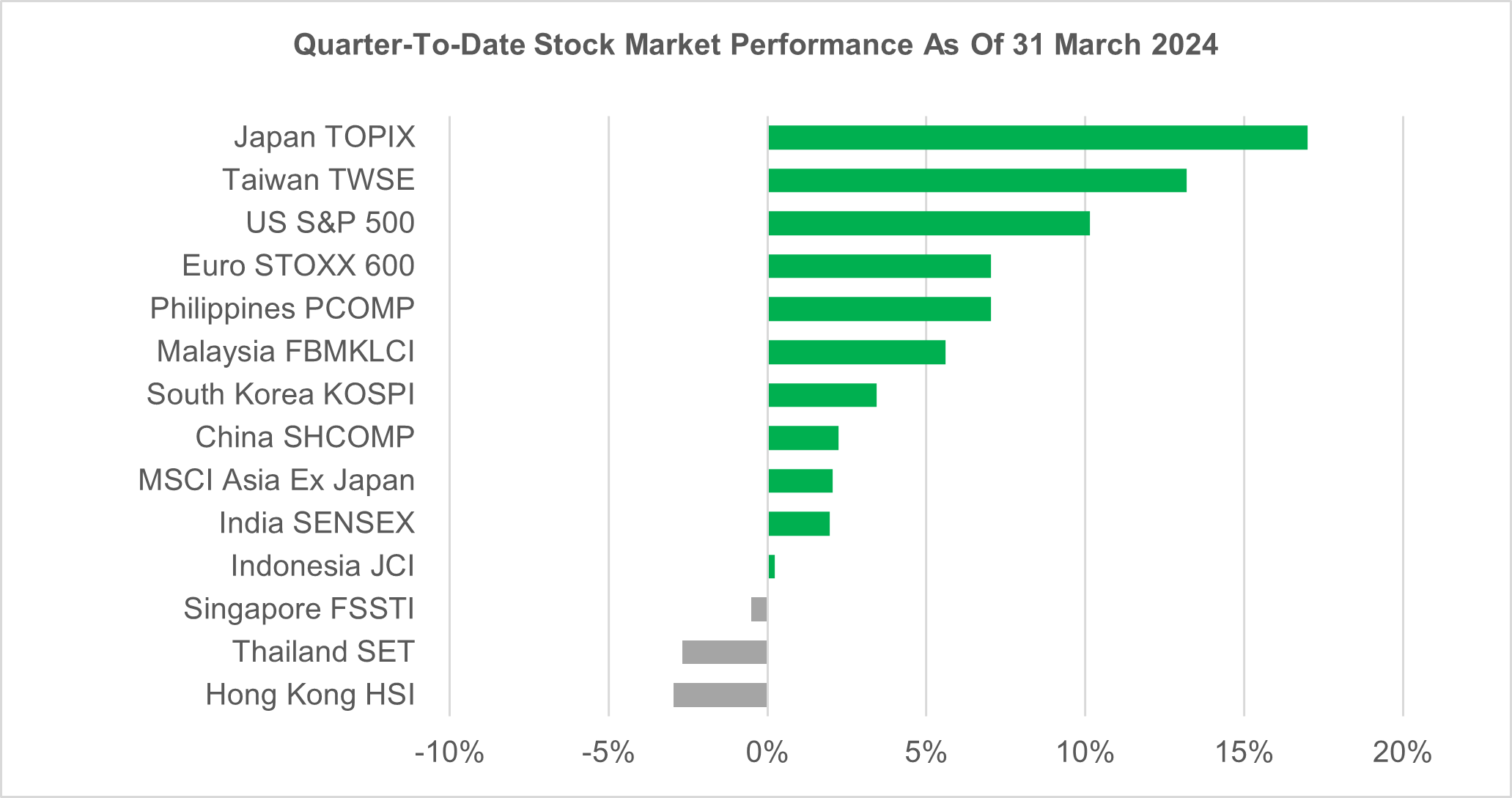

Global equities saw a strong start to the year, with developed markets leading the way. The MSCI World Index demonstrated an impressive 8.5% return in Q1 2024, while the MSCI Asia ex Japan recorded a modest 2.0% return for the quarter. This positive momentum was fuelled by encouraging economic data from the US, including robust jobs figures and a substantial 3.4% QoQ GDP growth in Q4, surpassing market expectations. Despite persistent inflation, favourable economic indicators overshadowed inflation concerns, triggering a broad market rally. Notably, all three major US stock indices – the S&P 500, the Dow Jones Industrial Average, and the Nasdaq Composite reached record highs, buoyed by a robust earnings season. In Q1 2024, Japan's TOPIX emerged as the best-performing market in the region, delivering an impressive 17.0% return, driven by a weakened Japanese Yen and the government's proactive corporate governance reforms aimed at enhancing shareholder returns. Additionally, Taiwan's technology-heavy TWSE came in second, posting an impressive 13.2% QoQ amid a global rally in technology stocks.

While numerous markets experienced gains in the quarter, some faced challenges. Hong Kong's HSI emerged as the biggest laggard in the region, returning -3.0% QoQ, as sentiment towards China soured following Beijing's announcement of a 2024 GDP target of 5%, mirroring that of 2023. China's lower target for fiscal spending and the absence of significant stimulus measures from Beijing raised concerns about its plans to boost growth to meet its GDP target. Additionally, Thailand's SET struggled, returning a flat -2.7% QoQ, as it grapples with fund outflows due to concerns over illegal naked short-selling activities.

Taking a closer look at the local equity market, Malaysia’s FBMKLCI kicked off the year strongly, emerging as one of the best-performing markets in the region with an impressive gain of +5.6% QoQ. The index's resurgence is largely attributed to the stellar performance of its top sectors, particularly the utilities and property sectors, which delivered remarkable returns of 16.9% QoQ each. The utilities sector's robust performance is credited to the government’s energy transition plans, especially as Malaysia has positioned itself as a regional hub for data center and cloud services. Additionally, utility stocks are known for their strong dividend payouts, adding to their appeal. On the other hand, positive developments such as the Johor-Singapore Special Economic Zone, Kuala Lumpur-Singapore HSR, and the easing of MM2H requirements have contributed to the favourable sentiment towards the property sector.

In the broader market, both the FBM100 Index and the FBM Small Cap Index mirrored the FBMKLCI's upward trend, returning 7.0% and 5.8% respectively.

Looking ahead, we maintain a positive outlook on the local equity market for the remainder of the year. Performance is expected to be driven by clear policy rollouts, stimulus and infrastructure projects, attractive valuations, high dividend yields, and the weakening Ringgit, which are likely to attract foreign funds. Furthermore, global growth is expected to improve further in 2024, with the anticipated normalization of interest rates in the 2H 2024 as inflation risks subside.

Source: Bloomberg, as of 31 March 2024. Past performance is not necessarily indicative of future performance.

Fixed income market

In Q1 2024, UST experienced significant volatility, driven by a widespread sell-off prompted by robust US economic data and labour market conditions, alongside higher-than-expected inflation figures. These factors prompted the market to push back on the timing of rate cuts by the US Fed while revising the number of anticipated rate cuts for 2024 from 6 to 3, resulting in a surge of UST yields. Consequently, UST yields underwent a bear flattening, with the 2-year, 5-year, and 10-year UST yields rising by +37bps, +37bps, and +32bps respectively, closing the quarter at 4.62%, 4.21%, and 4.20%.

In the local market, the MGS yield curve echoed the movements of the UST, albeit to a lesser degree. The 3-year, 5-year, and 10-year MGS yields rose by 2bps, 6bps, and 12bps, ending the quarter at 3.49%, 3.63%, and 3.86% respectively.

Against the backdrop of modest growth, manageable inflation and the need to maintain MYR’s stability, our base case is for BNM to keep OPR unchanged at 3.00% for the rest of the year. This implies unchanged OPR for the most of 2024, which should cap yields on local bonds. Anticipation of rate cuts and monetary easing in major economies, especially in 2H 2024, should also help sustain optimism for global bond markets in general. All in, we have a positive medium-term outlook for the local bond market. However, MGS movements could be volatile in the short term due to influence from UST movements and changes in global as well as regional risk sentiment.

2026 Outlook: Clearer picture, better growth

This year’s outlook spotlights a world in flux – U.S. stimulus, Europe’s rebound, China’s policy pivots, and Japan’s innovation surge all shape a landscape full of both opportunities and challenges.

2026 Asian Fixed Income Outlook: Positive momentum poised to continue amid ample investment opportunities

Asian fixed income posted strong gains in 2025 amid myriad challenges. Entering the new year, the asset class is poised for continued momentum on the back of numerous beneficial tailwinds. In this 2026 Outlook, the Asian Fixed Income team analyses the key factors likely to propel performance and identifies opportunities for investors based on key themes and developments in three regional bond markets: China, Japan, and India.

2026 Global Macroeconomic Outlook: clearer picture, better growth

Our 2026 macro outlook highlights key themes across global economies and commodities, what we'll be watching closely in the new year, and portfolio takeaways for investors to consider.

2026 Outlook: Clearer picture, better growth

This year’s outlook spotlights a world in flux – U.S. stimulus, Europe’s rebound, China’s policy pivots, and Japan’s innovation surge all shape a landscape full of both opportunities and challenges.

2026 Asian Fixed Income Outlook: Positive momentum poised to continue amid ample investment opportunities

Asian fixed income posted strong gains in 2025 amid myriad challenges. Entering the new year, the asset class is poised for continued momentum on the back of numerous beneficial tailwinds. In this 2026 Outlook, the Asian Fixed Income team analyses the key factors likely to propel performance and identifies opportunities for investors based on key themes and developments in three regional bond markets: China, Japan, and India.

2026 Global Macroeconomic Outlook: clearer picture, better growth

Our 2026 macro outlook highlights key themes across global economies and commodities, what we'll be watching closely in the new year, and portfolio takeaways for investors to consider.

![]()

©1999 - 2026 Manulife Investment Management (M) Berhad (Registration No. 200801033087 (834424-U))