The past quarter has been a wild ride for the global economy, evoking emotions akin to those experienced on a rollercoaster - from tumultuous to thrilling to terrifying. The economy has been plagued by painful fluctuations between high and low points, caused by severe shifts in market volatility. As Q1 2023 unfolds, it presents a dynamic and challenging period for the global economy, defined by a series of risk events that carry substantial implications for future interest rate trends. These events have sparked alternating waves of optimism and uncertainty, leading to substantial volatility in the market.

One such risk is inflation, which remains a key concern for central banks. Although markets responded positively to the drop in January's inflation figures, the unexpectedly high US inflation in February triggered a negative market reaction. While inflation has since moderated, it remains elevated, prompting the US Fed to raise the Fed Funds Rate by 25 basis points (bps) twice in Q1 2023. Interest rate hikes are expected to continue unless data shows a sustained downward trend towards the 2% target.

Another major risk event that has roiled the market is the spate of bank failures in the US. The collapse of Silvergate Bank, followed by Silicon Valley Bank and Signature Bank, sent shockwaves across the banking sector, affecting both major and regional banks as investors lost confidence. To mitigate this, the US Fed announced a new facility that will provide short-term loans to banks facing liquidity crunches. However, concerns soon spread to Europe, where troubled Credit Suisse saw its shares plummeted, despite assurances of liquidity support from Swiss authorities. To prevent the contagion from spreading, UBS intervened and bought over Credit Suisse for CHF3bil, with additional support from Swiss authorities. While swift actions from these central banks have contained the risks, the banking turmoil has rattled market confidence, leading to a significant scaling back of rate hike expectations amid concerns about tighter financial conditions in the aftermath, which then elicited a rally in the bond market.

While the collapse of several banks in the US has sent shockwaves through the global banking sector, China’s growth momentum improved as a result of its economic reopening. With the reopening of its international borders since January 2023, China is on its way to achieving its economic goals for the year, including a 5% gross domestic product (GDP) growth, maintaining a 3% consumer price index (CPI), and creating 12 million urban jobs, with focus on domestic demand. The Chinese government is also taking measures to prevent any disorderly expansion in the real estate sector, while supporting the balance sheets of high-quality developers. Despite concerns about financial stability, China's robust economic rebound presents a glimmer of hope for the global economy. According to International Monetary Fund Chief Kristalina Georgieva, every 1 percentage point increase in China's GDP translates to a 0.3 percentage point increase in the GDP of other Asian economies, underscoring China's significance as an economic engine in the region.

For Malaysia, Budget 2023 was re-tabled on February 24, 2023. While there were no major changes, fiscal deficit targets were tightened by rebalancing personal tax rates, broadening indirect taxes, reducing spending, and aiming for higher growth. Thanks to the recovery of private spending and investment, a strong labour market, and MYR’s strength, Malaysia's GDP grew remarkably by 8.7% in 2022. Headline inflation for the first two months of the year has also eased to 3.7%, well within the targeted range of 2.8% - 3.8%. This has prompted Bank Negara Malaysia (BNM) to keep policy rates unchanged at 2.75% in 1Q 2023, but implied future decisions would be data dependent.

Equity market

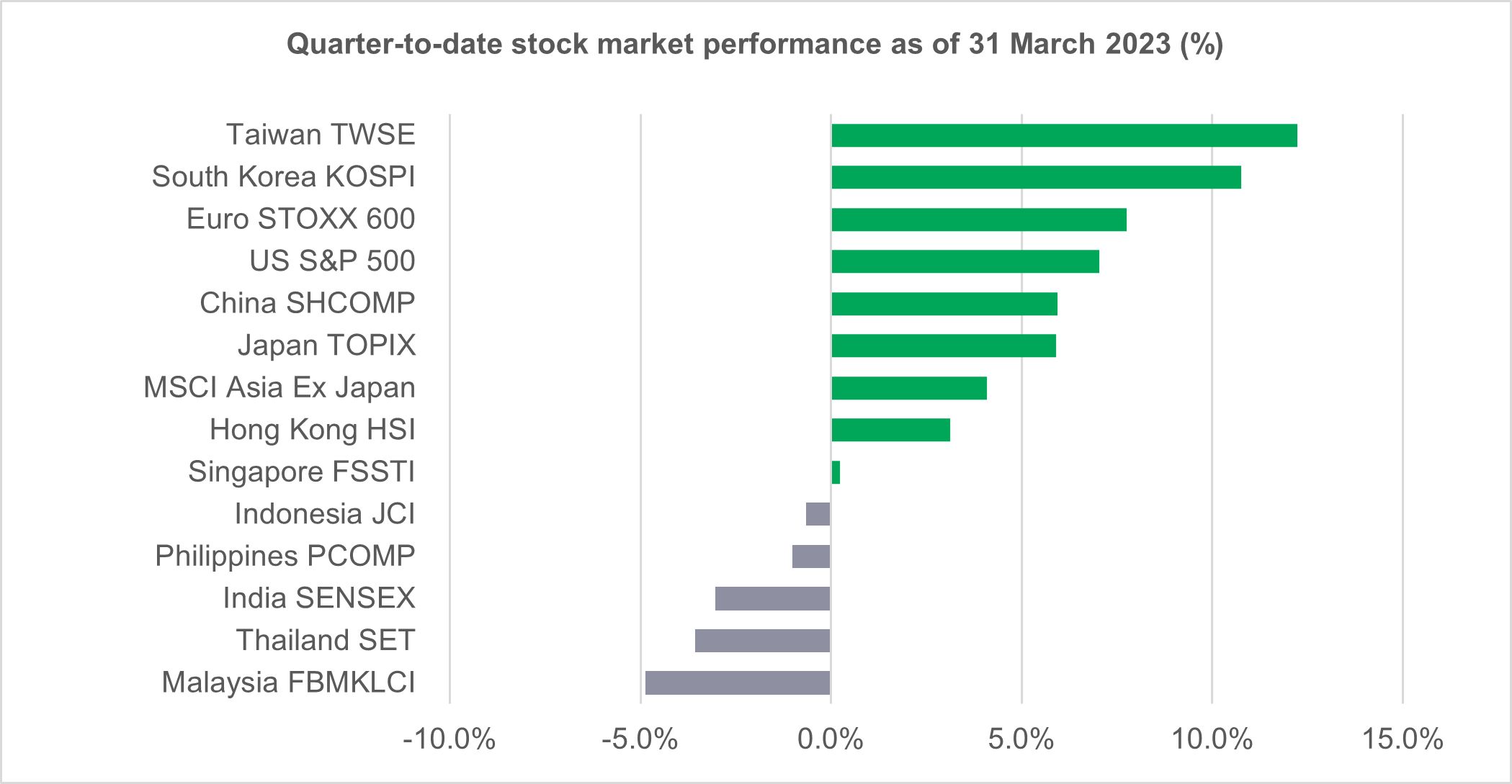

In Q1 2023, the global stock market witnessed a mixed bag of ups and downs. January began with an optimistic note as China's reopening and inflation expectations fuelled positivity across the markets, causing most stock indexes to end on a high with robust gains. The MSCI All Country World Index soared by a remarkable 7% for the month alone. However, the subsequent months of February and March posed challenges as higher-than-anticipated inflation and a banking crisis in the US and Europe resulted in disruptions and losses across many indexes. Despite this, lowered expectations of further interest rate hikes and a decline in bond yields allowed most rate-sensitive, technology-heavy indexes to finish in green, with Taiwan's TWSE leading with a triumphant finish of 12.2% quarter-on-quarter (QoQ), followed closely by the South Korean KOSPI, Euro STOXX 600, and the US S&P 500.

Despite most developed market indexes finishing positively in Q1 2023, performance was more lacklustre for some regional Asian indexes, which suffered from strong net foreign outflows due to risk-off trades following the recent banking turmoil. Malaysia's FBMKLCI and Thailand's SET finished at the bottom of the barrel for the quarter, with returns of -4.9% QoQ and -3.6% QoQ, respectively.

In January, the FBMKLCI saw a slight dip as investors became concerned about corporate earnings risks. However, this was just the beginning of a downward trend that continued through February and March. During these months, the local bourse fell in line with its regional peers, slipping by 4.3% for both months. Year-to-date March 2023, net foreign outflow for the Malaysian stock market totalled RM1.87bil1.

Throughout Q1 2023, the Energy and Property sectors emerged as the best performing sectors, driven by increased oil and gas activities and higher foot traffic from tourist arrivals in retail and hotel spaces, respectively.

In the broader market, the FBM 100 Index returned -2.9% QoQ, following the same downward trend as the FBMKLCI. On the other hand, FBM Small Cap Index generated a slight positive return of +2.2% QoQ as it has less exposure to financial stocks, which fared worse amid the US/Europe banking turmoil.

Looking ahead to 2Q23, global equity markets are expected to remain highly volatile due to several factors, including a possible mild recession in the US, elevated global inflation, and geopolitical tensions. However, there is cautious optimism for the equity market in 2H 2023. Hence, our current portfolio strategy will be centred around attractively valued dividend-paying stocks with firm fundamentals.

Source: Bloomberg, as of 31 March 2023. Past performance is not necessarily indicative of future performance.

Fixed income market

Q1 2023 was a whirlwind of a quarter for the US Treasury (UST) yields. Overall, the 2-year, 5-year and 10-year UST yields changed -40bps, -43bps and +41bps, to close at 4.03%, 3.57% and 3.47% respectively. UST yields declined after peaking in early March, attributed to the risk-off sentiment emanating from the collapse of multiple banks in the U.S. and Switzerland. The 2-year and 10-year UST yields remains inverted to this end.

For the local market, Malaysian Government Securities (MGS) yield curve shifted down in Q1 2023; 3-year, 5-year and 10-year MGS yields changed -32bps, -32bps and -19bps respectively to close the quarter at 3.35%, 3.54% and 3.90%. Movement of MGS tracked the selling direction of the global bond market.

BNM had again kept the Overnight Policy Rate (OPR) unchanged at 2.75% in March’s Monetary Policy Committee meeting. BNM’s tone was largely neutral, while appearing to keep its options open. BNM did acknowledge though that external development had increased both growth risks and inflationary pressure domestically. We think BNM is at the end of its rate hike cycle and expect either no hike or one more OPR hike in 2023.

In general, we continue to hold a positive outlook for MGS, driven by expectations of subdued economic growth, manageable inflation levels, and the anticipated end of BNM's rate hiking cycle this year. However, we are expecting high volatility in the short term, given the uncertainty surrounding the trajectory of rate hikes amid evolving economic and geopolitical conditions. Concerns such as contagion risks from the recent bank turmoil, Russia-Ukraine conflict, and the US-China tech war may pose further headwinds to both markets. Therefore, we remain cautious and closely monitor global developments to gauge market reactions to this end.

Download full PDF View key takeaways

Source:

1MIDF Research, as of 31 March 2023

2026 Outlook: Clearer picture, better growth

This year’s outlook spotlights a world in flux – U.S. stimulus, Europe’s rebound, China’s policy pivots, and Japan’s innovation surge all shape a landscape full of both opportunities and challenges.

2026 Asian Fixed Income Outlook: Positive momentum poised to continue amid ample investment opportunities

Asian fixed income posted strong gains in 2025 amid myriad challenges. Entering the new year, the asset class is poised for continued momentum on the back of numerous beneficial tailwinds. In this 2026 Outlook, the Asian Fixed Income team analyses the key factors likely to propel performance and identifies opportunities for investors based on key themes and developments in three regional bond markets: China, Japan, and India.

2026 Global Macroeconomic Outlook: clearer picture, better growth

Our 2026 macro outlook highlights key themes across global economies and commodities, what we'll be watching closely in the new year, and portfolio takeaways for investors to consider.

2026 Outlook: Clearer picture, better growth

This year’s outlook spotlights a world in flux – U.S. stimulus, Europe’s rebound, China’s policy pivots, and Japan’s innovation surge all shape a landscape full of both opportunities and challenges.

2026 Asian Fixed Income Outlook: Positive momentum poised to continue amid ample investment opportunities

Asian fixed income posted strong gains in 2025 amid myriad challenges. Entering the new year, the asset class is poised for continued momentum on the back of numerous beneficial tailwinds. In this 2026 Outlook, the Asian Fixed Income team analyses the key factors likely to propel performance and identifies opportunities for investors based on key themes and developments in three regional bond markets: China, Japan, and India.

2026 Global Macroeconomic Outlook: clearer picture, better growth

Our 2026 macro outlook highlights key themes across global economies and commodities, what we'll be watching closely in the new year, and portfolio takeaways for investors to consider.

![]()

©1999 - 2026 Manulife Investment Management (M) Berhad (Registration No. 200801033087 (834424-U))