Macroeconomic Strategy Team

10 January 2023

As we consider the year ahead, we expect to see a game of two halves, where challenging conditions will prevail in the first half before improving through the second half. The aggressive pace of monetary tightening and its associated lagged effects should drive a synchronised global growth downturn in the first half.

We expect global growth to slow materially and come in substantially lower than the below 3% threshold that the International Monetary Fund uses to define global recessions. A downturn of this magnitude—excluding the COVID-19 shock and the global financial crisis—could make 2023 the worst year for global growth since the 1980s. We expect the economic slump to become more apparent in the first half of the year, with a cyclical bottom only occurring in Q2/Q3.

Our analysis shows that most advanced economies are likely to experience a recession in the year ahead. Given that the U.S. Federal Reserve (Fed) has been hiking rates at the fastest pace in decades, the U.S. economy will be facing the lingering effects of substantial policy tightening, with real rates rising while inflation eases gradually.

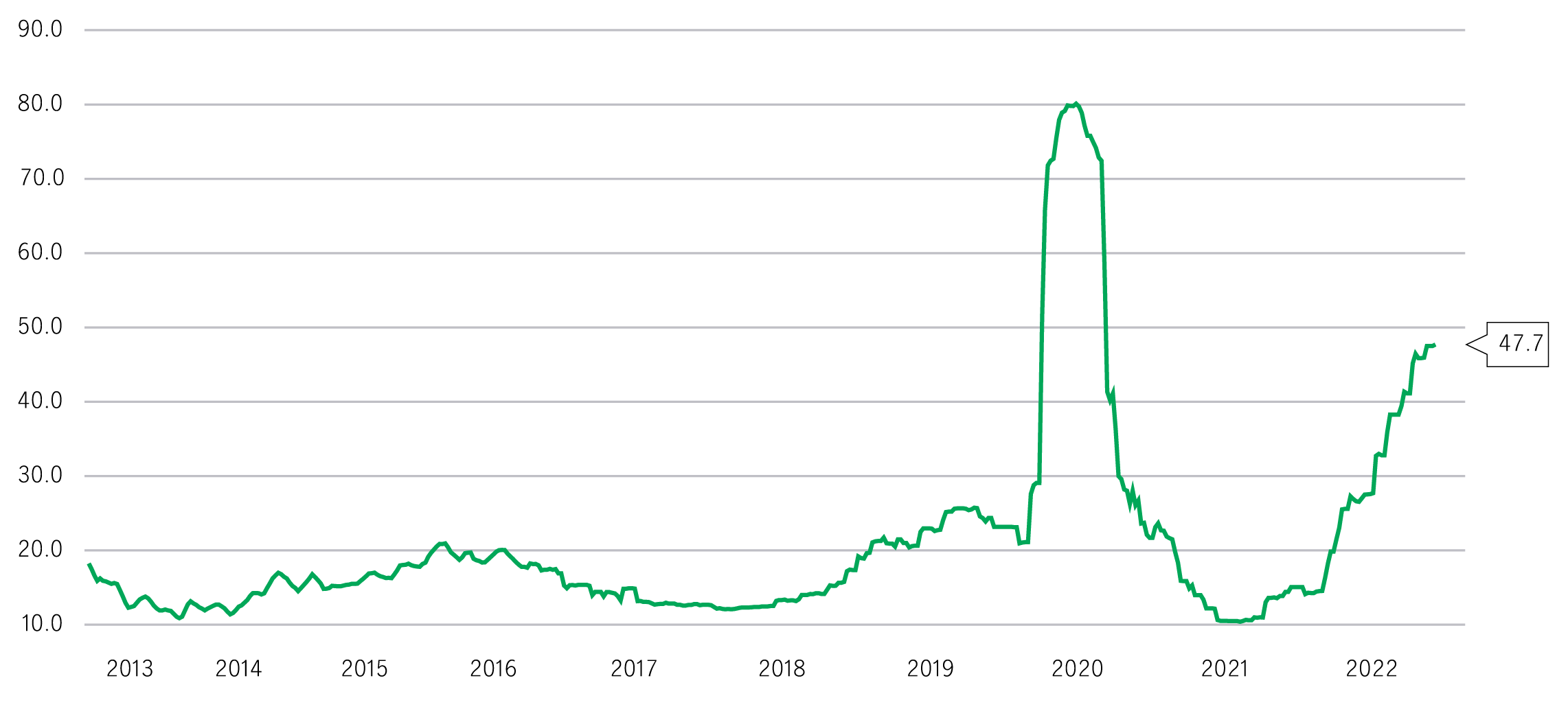

Market’s view on the probability of a global recession (%)

Source: Bloomberg, Macrobond, Manulife Investment Management, as of 13 December, 2022.

Economic weakness will be particularly pronounced in interest-rate-sensitive economies such as Canada, Australia, New Zealand, and the United Kingdom—these economies would almost certainly be confronting downside risks as a result of spillovers from their respective weaker housing markets. In Continental Europe, the growth drag will predominantly stem from particularly large negative terms-of-trade shocks.

Meanwhile, slowing final demand from advanced economies, elevated inflation, and a still-strong U.S. dollar (USD) will likely morph into material headwinds for growth in emerging markets (EM). In mainland China, a bumpy exit from zero-COVID policy, weak external demand, a still struggling property sector, and insufficient policy support look set to extend the country’s below-trend GDP into 2024. That said, the prospects for the rest of Asia’s economies are a little more mixed: We expect weak foreign demand to weigh on export growth, but North Asia is particularly vulnerable in light of a likely inventory overhang. On the other hand, weakness in ASEAN countries will likely be cushioned by a strong reopening bounce and relatively healthy household balance sheets.

Amid a macro backdrop characterized by elevated global inflation, uncertainty over when Fed rates might peak, and rising odds of a global recession, the first half of 2023 could bear witness to a series of sharper—and longer—bouts of market volatility. Thankfully, the picture does brighten slightly in the second half, during which these headwinds are likely to moderate, ushering in more conducive conditions for financial markets.

2026 Mid-year outlook: Greater China Equities

Greater China equity markets showed divergent trends in the first half of 2026, with China A-shares and the Taiwan Taiex index registering strong gains driven by resilient technology exports amid global demand for artificial intelligence (AI). Meanwhile, the MSCI China market pulled back, weighed by commerce subsidies amid fierce competition in food delivery and rising AI capital expenditure, which we believe have already been priced in. In this mid-year Outlook, we highlight five positive drivers for China and Hong Kong equities in the second half of the year. Furthermore, the team explains why it believes the Taiwan region’s technology sector should continue to enjoy positive momentum.

2026 Mid-Year Outlook Series: Asia Equities ex-Japan

Asia equities ex-Japan continued the significant momentum from 2025 with strong performance throughout the first half of the year. Amid numerous catalysts, June Chua, Head of Asia Equities outlines in this Mid-Year Outlook why she is constructive on the asset class for the remainder of 2026. Positive drivers include: potential geopolitical resolution in the Middle East and lower energy costs, supportive earnings and valuations, and differentiated growth drivers across the region.

2026 Global healthcare equities outlook: Innovation supports healthcare’s long term case

Global healthcare equities showed resilience amid 2025 volatility. The defensive characteristics, coupled with remarkable therapeutic innovations in the biopharmaceutical, MedTech, and tools sub-segments of this sector, will continue to be rewarded with capital appreciation over a full market cycle. Current valuations relative to the broader market make for an attractive entry point today, and periods like this tend to lead to outperformance for healthcare stocks over the long term.

2026 Mid-year outlook: Asian Fixed Income

In this Mid-Year Outlook, the Asian Fixed Income team explains this important change in monetary policy expectations, and why the asset class is well positioned to capitalise on it.

2026 Mid-Year Outlook Series: Asia Equities ex-Japan

Asia equities ex-Japan continued the significant momentum from 2025 with strong performance throughout the first half of the year. Amid numerous catalysts, June Chua, Head of Asia Equities outlines in this Mid-Year Outlook why she is constructive on the asset class for the remainder of 2026. Positive drivers include: potential geopolitical resolution in the Middle East and lower energy costs, supportive earnings and valuations, and differentiated growth drivers across the region.

2026 Mid-year outlook: Greater China Equities

Greater China equity markets showed divergent trends in the first half of 2026, with China A-shares and the Taiwan Taiex index registering strong gains driven by resilient technology exports amid global demand for artificial intelligence (AI). Meanwhile, the MSCI China market pulled back, weighed by commerce subsidies amid fierce competition in food delivery and rising AI capital expenditure, which we believe have already been priced in. In this mid-year Outlook, we highlight five positive drivers for China and Hong Kong equities in the second half of the year. Furthermore, the team explains why it believes the Taiwan region’s technology sector should continue to enjoy positive momentum.

![]()

©1999 - 2026 Manulife Investment Management (M) Berhad (Registration No. 200801033087 (834424-U))