25 April 2022

Kai Kong Chay, Senior Portfolio Manager, Greater China Equities

On 15 April, the People’s Bank of China (PBOC), China’s central bank, announced a reduction in its reserve requirement ratio (RRR). Subsequently, the government also published 23 measures to support individual and small businesses, and stepped up its efforts to keep supply and industrial chains stable. In this investment note, Kai Kong Chay, Senior Portfolio Manager, Greater China Equities, presents an updated view of the China and Hong Kong markets. He believes that the latest measures reiterate China’s stance on economic stability and sees opportunities in China and Hong Kong equities that could benefit from these supportive policy actions.

China announced several measures to release long-term liquidity into the financial system to bolster the economy. These include:1

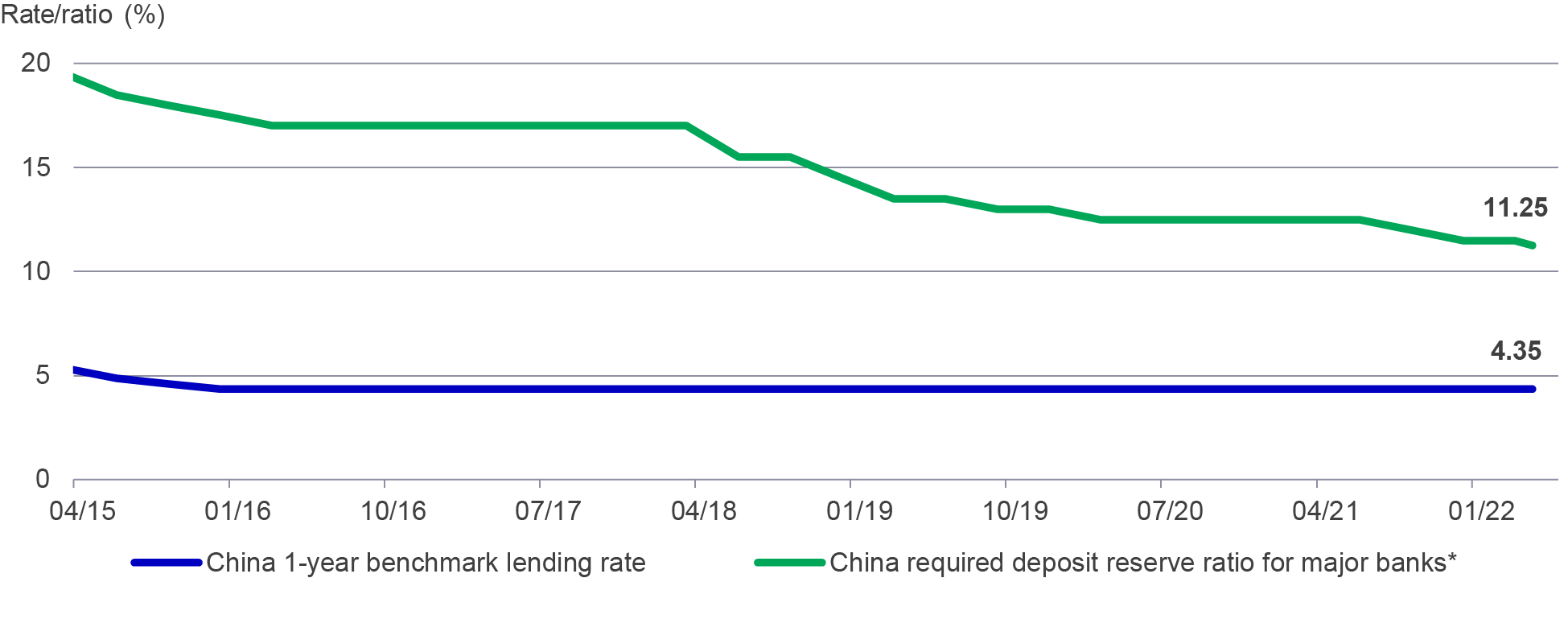

Chart 1: China’s reserve requirement ratio and lending interest rate (as of 19 April 2022)

Source: Bloomberg, 19 April 2022. *Note: The reserve requirement ratio (RRR) will be reduced to 11.25% is effective from 25 April 2022.

In addition, China’s corporates or small and medium enterprises (SMEs) may benefit after the central bank announced 23 additional measures to support the economy. Some key highlights include:3

Separately, the China Banking and Insurance Regulatory Commission vowed to increase financial resources for logistics, transportation, and courier industries and use the relending funds to lower financing costs. It will provide funding support to smaller businesses suffering from temporary difficulties due to COVID-19.

While some market participants expected a bold reduction in interest rates, we believe China has adequate policy tools other than a rate cut to support growth if needed.

Despite a near-term dampening of investor sentiment, we believe the recent measures prove that China is determined to support the local economy:

While we remain selective, we see opportunities in the sectors and key themes of China and Hong Kong equities that should benefit from China’s structural growth story. These opportunities include:

Overall, we believe China is ready to act and likely to step up policy easing should a sharper economic slowdown occur. In addition, China has the levers for fiscal support, such as further spending on investments and infrastructure, as well as tax refunds and cuts. While near-term market sentiment has been mixed, we view the latest measures as signs that China is on track to maintain its economic course.

1 Bloomberg, 19 April 2022.

2 Reuters, 18 April 2022.

3 Bloomberg, 19 April 2022.

4 Reuters, 18 February 2022.

5 South China Morning Post, 4 April 2022.

AI innovation: Asia helps build many of the world’s technologies behind it

When electricity first arrived, the world built the necessary infrastructure – power plants, transmission lines – before the real transformation could take hold. A similar process is happening with artificial intelligence (AI). Today's massive investment in chips, data centres, and power grids is laying the foundation for a potential expansion in AI application that could take years to develop. In our view, the discussion is increasingly shifting from whether AI adoption will continue to how the enabling infrastructure is being built. Asia appears to be playing an important role in that development.

The engine behind AI: Semiconductors are fuelling the next era of technology

Semiconductors belong to one of the most specialised yet globally integrated industry chains. From design, equipment, and materials to manufacturing and commercialisation, the production of a smartphone chip alone spans many countries across continents, creating tremendous opportunities for companies, consumers, and investors. With semiconductors increasingly becoming the backbone of an artificial intelligence (AI) race few are prepared for, understanding this sector is key to unlocking where the next wave of technology competition is heading.

China Fixed Income: From deflation to reflation: what comes next?

![]()

©1999 - 2026 Manulife Investment Management (M) Berhad (Registration No. 200801033087 (834424-U))