28 December 2022

Hui-Min Ng, Portfolio Manager

Like all risk assets, Asia-Pacific REITs (AP REITs) experienced a volatile 2022. Higher rates globally were driven by surging energy prices and inflation, and there were concerns of cap rate expansion leading to pressure across the asset class. Moving into 2023, Hui-Min Ng, Portfolio Manager, believes that given a potentially more normalised macro landscape, investors should refocus on the region’s fundamentals, such as strong balance sheets, positive rental growth, and sustainable dividend payouts.

2022 was a challenging year for all asset classes, but AP REIT fundamentals remained resilient despite the risk-off environment. This was evidenced by their earnings results and guidance. In addition, asset values remained buoyant, driven by healthy rental growth and growth in distribution following the cessation of rental relief measures.

We believe that investors will shift their attention in the new year to the underlying fundamentals of AP REITs – as the volatile interest rates that dented overall REIT performance in 2022 begin to stabilise. In turn, this should pave the path for a more normalised market environment.

From an asset-class perspective, investors should remember that dividend returns are a central feature of the REIT asset class – when markets decline, dividends help compensate for any price losses. And regardless of the market environment over the past decade, dividend return has remained positive (See Chart 1). So, when markets move higher, dividends augment total return.

Chart 1: AP REITs total return: 2010-2022 (YTD)1

Source: Bloomberg as of 30 November 2022 Asia ex-Japan REITs are represented by FTSE EPRA/NAREIT Asia ex Japan REITs Index (capped). Performance in USD.

Worries about the impact of both higher rates and energy costs on the asset values and profitability of AP REITs characterised a challenging 2022. This translated into market uncertainty about the ability of these asset managers to maintain their distributions to investors.

As interest rates rose over the year, investor concerns persisted on potentially lower asset values due to rising cap rates. However, we felt the level of drawdown priced into AP REITs, due to higher rates, was not indicative of their underlying operational performance (See Chart 2).

Chart 2: AP REITs total return by market, December 2021-Nov 20222

Additionally, the re-opening tailwinds in Asia over the year provided some ballast for the asset class, but these are expected to fade (except for Hong Kong SAR and mainland China) heading into 2023.

From a geographic perspective:

Moving into 2023, the US Federal Reserve is likely to gradually reduce the quantum of rate hikes and should pause as upward inflationary pressures decelerate. However, the risk of persistent sticky inflation and lower growth in the US and abroad still exists, particularly in the second half of next year. Any potential easing of global inflation and labour markets (rising wage pressure) could offer central bankers more monetary room to balance growth versus inflation.

Although the impact of higher rates and energy costs should still be felt in 2023, the impact has been well communicated by corporates.

Indeed, as interest-rate volatility starts to normalise, it may provide a better environment for risk assets, including REITs. As such, we believe the incremental impact of higher rates on interest costs should subside and investors can focus more on AP REITs’ operational performance and underlying fundamentals.

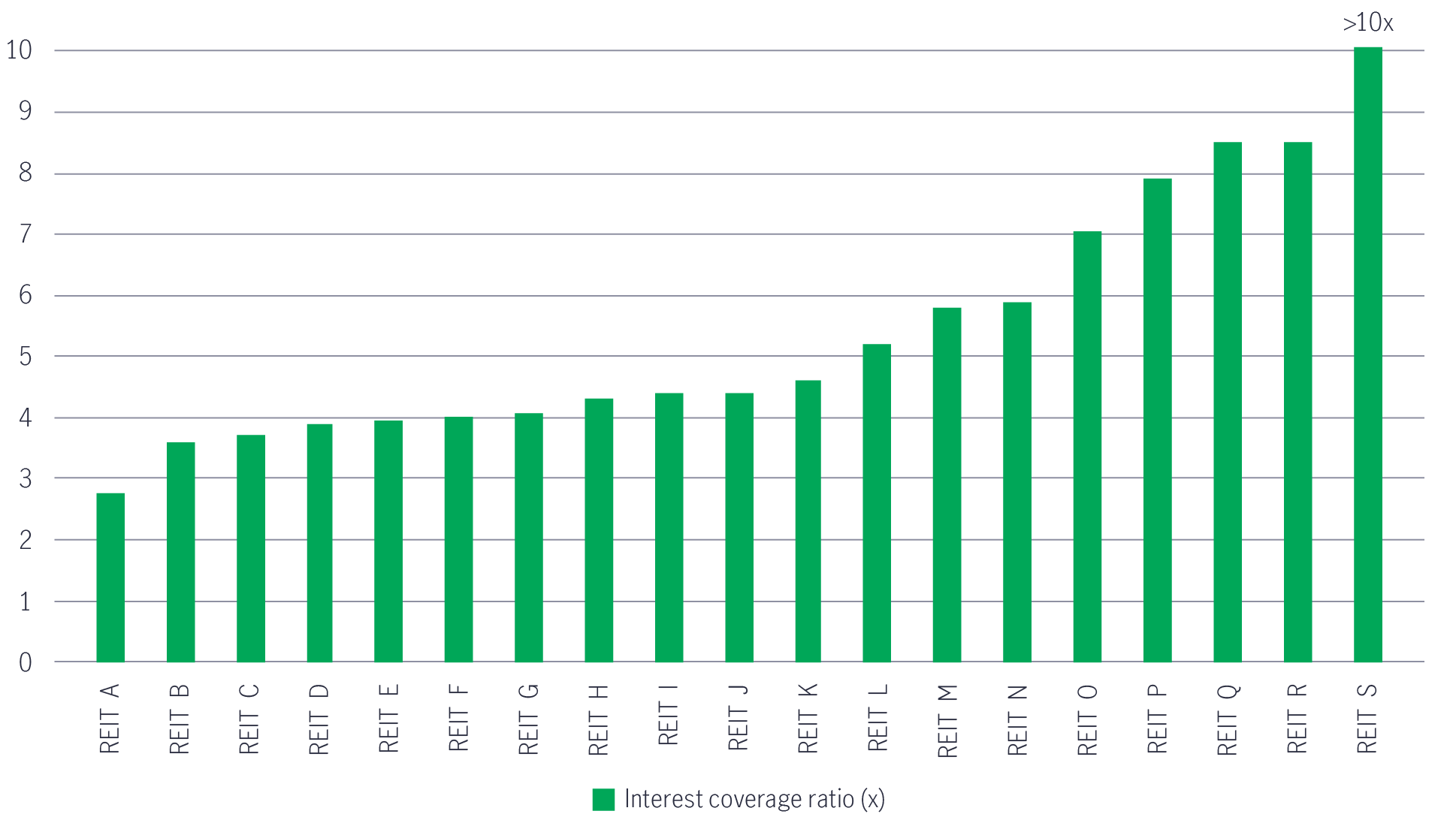

We currently do not see balance sheet or liquidity risk for AP REITs given healthy levels of leverage and, more importantly, the ability to service debt. As highlighted in Chart 3, current interest coverage ratios (ICR) for key Singapore REITs are well above the typical minimum threshold (Adjusted EBITDA 2 times interest payments).

Chart 3: Interest coverage ratio for key Singapore REITs3

Even if we factor in the possibility of higher interest rates, refinancing risks are staggered over a few years. Additionally, rising net property income would help mitigate the overall impact of higher rates on ICR4.

Further, rental reversions are likely to be positive in the industrial, hospitality, and retail sectors in 2023. Given the high occupancy and continued demand in e-commerce and logistics warehousing, we could see continued positive rental reversions, which should help partially mitigate the impact on asset values from cap rate expansion.

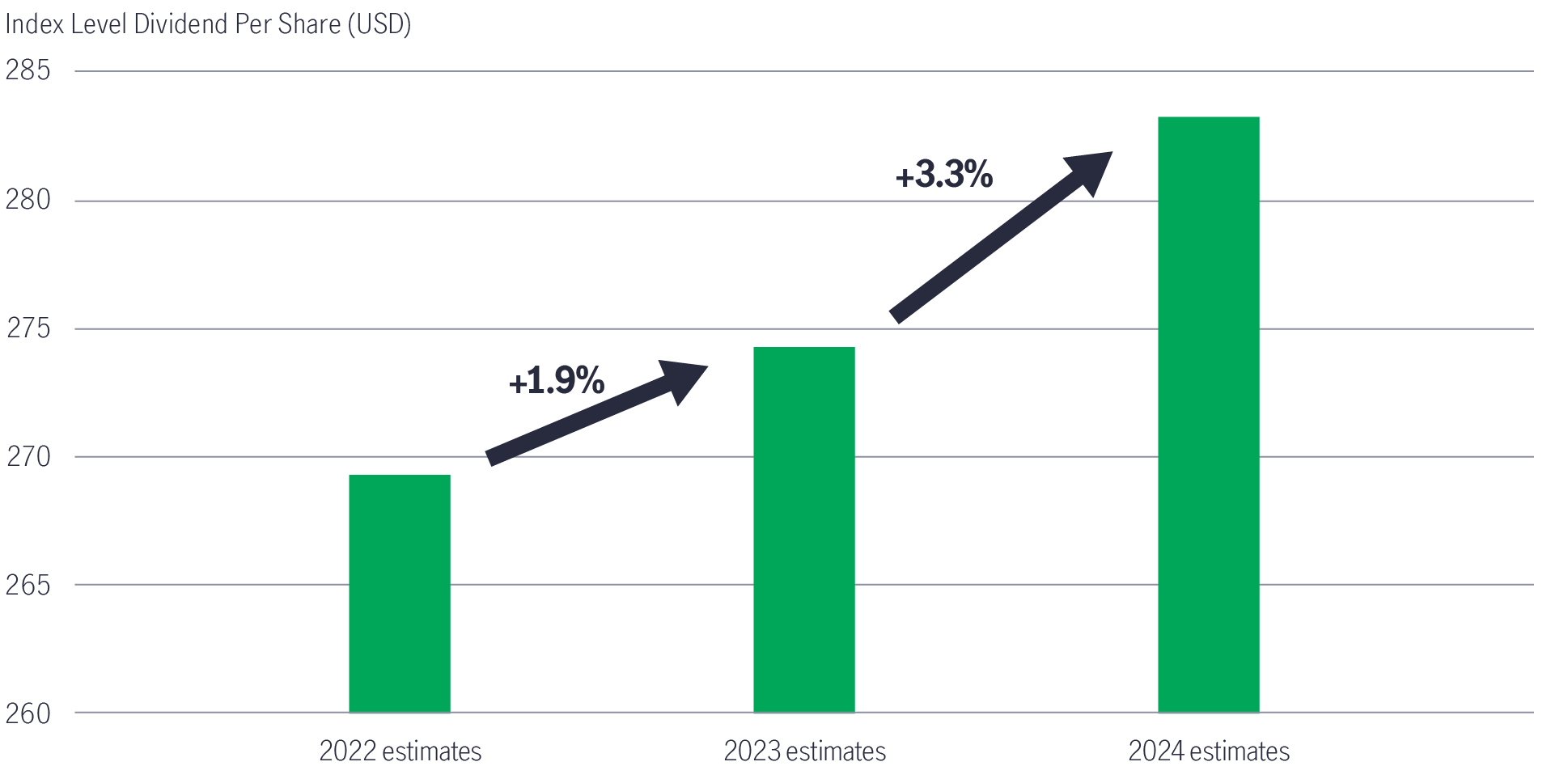

Finally, we also expect dividend growth to continue. After downward revisions in analyst expectations, given some of the challenges mentioned, there are still expectations for DPU growth through 2024 (see Chart 4).

Chart 4: Dividend growth tapped to increase5

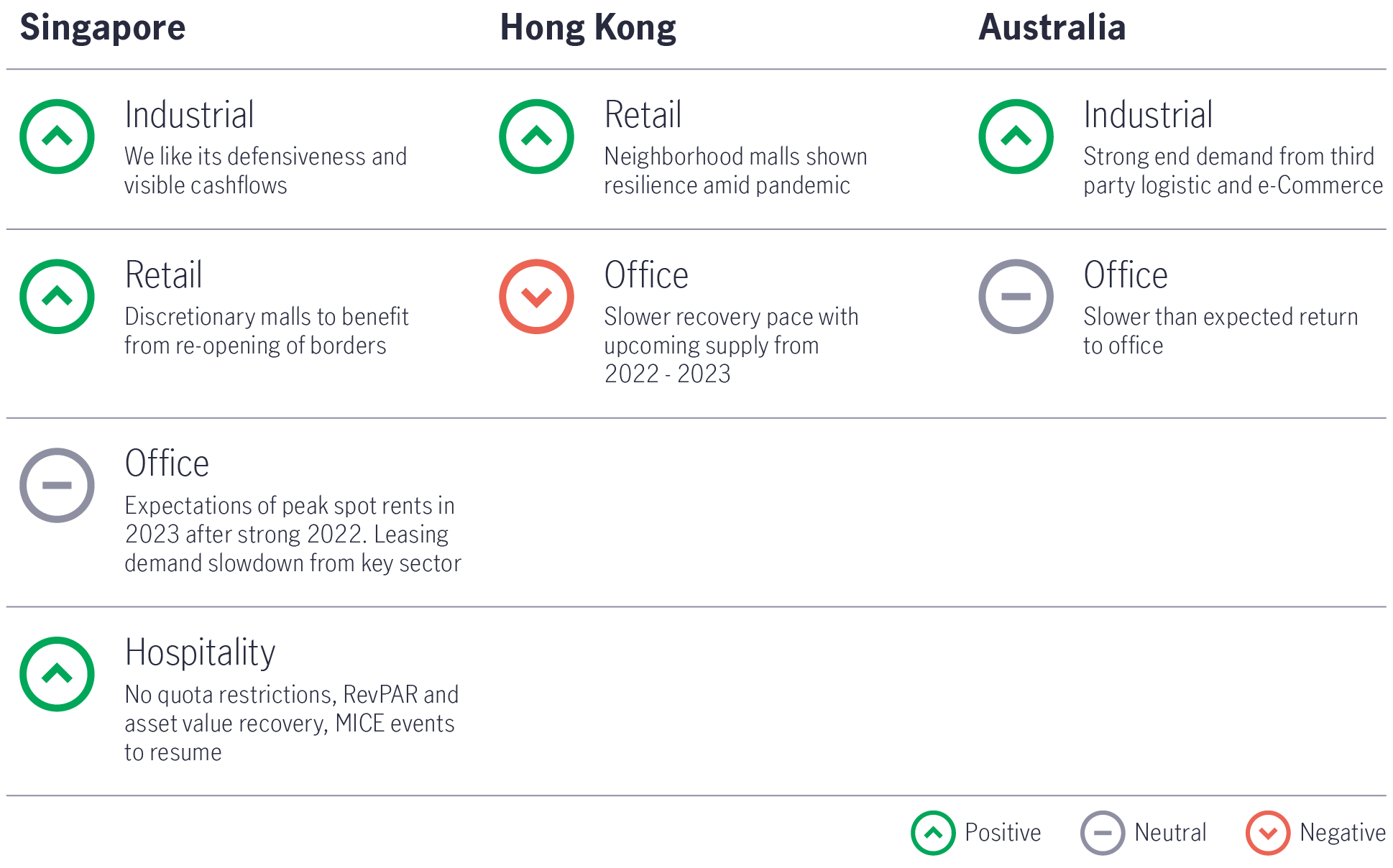

We are more constructive on industrials and retail than offices in 2023 (see Chart 5).

Chart 5: 2023 AP REIT segment outlook6

After a difficult 2022, investors in AP REITs should likely look at the asset class’s robust underlying fundamentals in the new year, which we consider as core earnings and cashflow strength, strong capital management, and quality real estate which generally provides greater resilience to rental rates during times of economic uncertainty – all factors which provide support to sustainable dividend payouts.

1 Source: Bloomberg as of 30 November 2022 Asia ex-Japan REITs are represented by FTSE EPRA/NAREIT Asia ex Japan REITs Index (capped). Performance in USD.

2 Source: Bloomberg, 30 Nov 2022. Singapore REITs measured by FTSE ST Real Estate Investment Trusts Total Return Index, Hong Kong REITs measured by Hang Seng REITs index; Australia REITs measured by S&P/ASX 200 A-REIT Total Return Index. USD, total return.

3 Source: Bloomberg, as of 30 November 2022.

4 Source: Manulife Asset Management Analysis and company reports.

5 Source: Bloomberg consensus estimate, as of 24 October 2022. Asia REITs measured by FTSE/EPRA Nareit Asia ex Japan index (capped).

6 Source: Manulife Asset Management analysis. RevPAR = revenue per available room. MICE = meetings, incentives, conferences, and exhibitions.

2026 Global healthcare equities outlook: Innovation supports healthcare’s long term case

Global healthcare equities showed resilience amid 2025 volatility. The defensive characteristics, coupled with remarkable therapeutic innovations in the biopharmaceutical, MedTech, and tools sub-segments of this sector, will continue to be rewarded with capital appreciation over a full market cycle. Current valuations relative to the broader market make for an attractive entry point today, and periods like this tend to lead to outperformance for healthcare stocks over the long term.

Semiconductors poised for long-term growth amid AI boom

The global semiconductor industry remains strong – arguably the most robust we have seen in over three decades. This strength is supported by cutting-edge innovation, rising revenues and robust capital spending. While risks remain, the outlook for 2026 appears constructive, with demand for artificial intelligence (AI) applications showing few signs of slowing. Beyond AI, the non-AI markets could be poised for positive revisions as cyclical recovery gains traction after several years of consolidation.

2026 Outlook Series: Manulife Global Multi-Asset Diversified Income Fund

In 2026, a clearer macroeconomic outlook is expected as momentum improves following strong 2025 drivers such as AI growth, energy transition, anticipated Fed rate cuts, and wider fiscal support. While the US Federal Reserve is likely to continue easing policy, diverse income opportunities remain across global markets, extending beyond traditional government bonds to high yield assets and option writing. Within this environment, the Manulife Global Fund – Global Multi‑Asset Diversified Income Fund (GMADI) remains with a clear and heightened focus towards income generation. The Fund seeks to deliver a high and consistent distribution income while maintaining exposure to long term capital growth opportunities.

![]()

©1999 - 2026 Manulife Investment Management (M) Berhad (Registration No. 200801033087 (834424-U))