31 December 2025

Paula Chan, Head of Hong Kong Fixed Income, Senior Portfolio Manager

Isaac Meng, Portfolio Manager

Despite early challenges and persistent deflation, China’s fixed income market held steady throughout this year, demonstrating resiliency. In this 2026 Outlook, the China Fixed Income team analyses the fundamentals and trajectory of the asset class, advocating for a moderate overweight duration position to take advantage of further monetary easing. Additionally, the team favours high-quality offshore Chinese renminbi (CNH) corporate bonds for their yield and diversification benefits.

At the beginning of 2025, investors had numerous concerns about the outlook for the Chinese Mainland economy, including persistent deflation, high unemployment, ongoing weakness in the property sector, and uncertainty around Sino-US relations.

Despite disruption to global trade relations between the US and other geographicals following the announcement of sweeping US tariff measures in early April, the impact on China’s trade so far has been contained.

Indeed, China’s exports have continued to grow throughout the year, while the People’s Bank of China (PBOC) cut its policy rate by 10 basis points (bps) to 1.40% in May.

Earlier in the year, as the 10-year China Government Bond (CGB) yield reached an all-time low of 1.6% amid expectations for further monetary easing, the PBOC temporarily suspended CGB buying for a period of 10 months.

This resulted in the yield curve adjusting higher by 10–20 bps as bullish investors repositioned for reflation and added to their risk exposure.

Chinese Mainland equity markets also surged during the first half of the year, led by the technology sector, while economic growth held up well. GDP growth for the third quarter posted at 4.8% (year on year), broadly in line with the government’s 5% annual growth target. Onshore interest rates have remained generally stable throughout the year.

Regarding currency, the renminbi (RMB) appreciated by 3.8% to 7.07 against the US dollar, in contrast with the depreciation and outflows seen during trade tensions of President Trump’s first term.

The rally in the RMB followed the unwinding of the elevated geopolitical risk premium for China. Five rounds of tough Sino-US trade negotiations led to a 12-month truce following the meetings between President Xi and President Trump held on the sidelines of the APEC Summit in late October.

Some market observers have even suggested that China is now better placed in trade negotiations, having closed the gap with the US on competition in both technology and industrial supply chains.

On the domestic front, we see robust fiscal stimulus as a decisive driver to support economic growth.

The 2025 fiscal impulse has reached 3.5–4.0% of GDP, providing support to domestic consumption, private capital expenditure, and technology upgrades. The deployment of sovereign and PBOC liquidity remains key to anchoring stock market volatility. Recent supply-side industrial policies have also been targeted to mitigate overcapacity and the ongoing downward spiral in industrial prices.

China approved its 15th Five-Year Plan (2026-2030) on 28 October. This timeframe is a critical stage of China’s 2035 goal of “basically achieving socialist modernisation”.

To achieve a doubling of its GDP by 2035 compared with 2020, this implies an average GDP growth rate of 4.4% annually from 2026 to 2030.

The core priorities of the 15th Five-Year Plan will involve developing “new productive forces”, including shifting from speed to higher-quality, sustainable growth.

China will also focus on developing a modern industrial system whilst achieving technological self-reliance by investing in semiconductors, artificial intelligence (AI), quantum technology, and 6G, as well as advancing green and low-carbon energy.

More fiscal and financial policies will also be needed to support household consumption and end deflation.

Heading into 2026, we will closely monitor the following macroeconomic dynamics:

Will members of Congress be able to sustain or even accelerate fiscal support in 2026?

Over the first three quarters of 2025, government financing – including CGB, Local Government Bonds (LGB) and Policy Bank issuance – increased by RMB 4.9 trillion, helping boost the fiscal impulse to nearly 3.7 percentage points of GDP (Chart 1).

Chart 1: China’s fiscal impulse: annual change of CGB, LGB, policy banks’ net financing1

Maintaining a high level of fiscal spending will be critical to support consumption, stabilise the property market and provide a backstop against external uncertainties.

In September, the Ministry of Finance brought forward the implementation of its planned government spending programme for 2026, totalling RMB 1.0 trillion, and approved RMB 500 billion in policy bank stimulus facilities.

If the external environment deteriorates and progress towards domestic recovery and reflation stalls, we see ample room for authorities to dial up fiscal support by another RMB 1–2 trillion or around 1.5 percentage points of GDP.

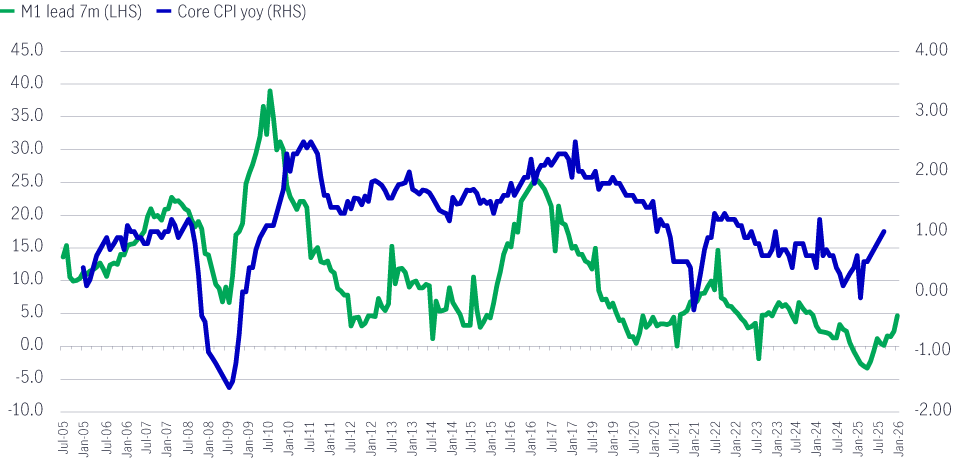

Given the PBOC has only cut policy rates by 10 bps to 1.40% in early May of this year at the peak of trade tensions, we believe China’s real policy rate remains restrictive at 1.50–2.00%, particularly given prevailing deflationary pressures.

To prevent deflation from becoming entrenched and to sustain tentative progress toward reflation, further monetary policy easing is required (Chart 2 and 3).

Chart 2: PBOC’s policy rate corridor2

Chart 3: China’s money supply (M1) and core CPI3

We expect the PBOC to cut rates by a further 20 bps to 1.20%. This would also avoid the appreciation in the RMB from overshooting as the US Federal Reserve (Fed) will likely cut rates in early 2026.

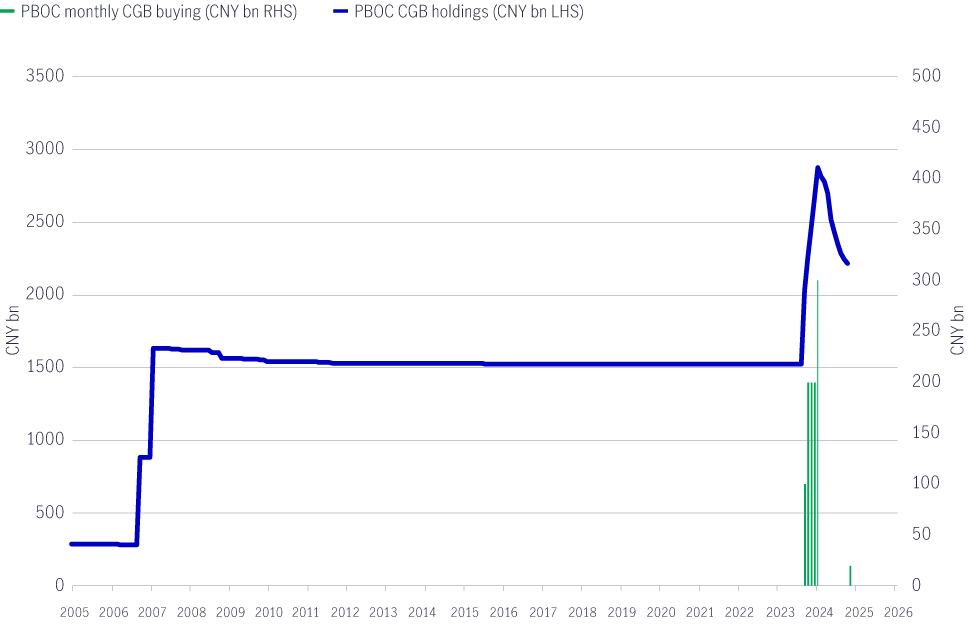

After suspending purchases for 10 months, the PBOC resumed CGB buying and added RMB 20 billion in October as the 10-year CGB yield approached 1.90% (Chart 4).

Chart 4: PBOC resumes quantitative easing4

We expect the PBOC’s CGB buying programme to be closely integrated with fiscal supply. Monthly purchase volumes are expected to be around RMB 150–200 billion, with purchases extended to bonds with 5–10-year maturities (i.e., the belly of the yield curve).

While such purchases are not considered explicit quantitative easing or yield-curve control policies, the implicit policy objectives involve greater coordination of fiscal and monetary policies to facilitate larger fiscal expansion and stabilise the CGB yield curve.

After a period of tit-for-tat tariff escalations combined with technology and export controls, negotiations between President Xi and President Trump in October have led to détente.

Trade tensions are now on the back burner, and the markets' baseline assumption is that the Sino-US trade truce will be maintained or de-escalate further in 2026.

President Trump’s scheduled state visit to China in April and President Xi’s reciprocal visit to the US later in the year are expected to be key milestones.

We expect the 10-year CGB to range between 1.60% and 1.90% in the first half of 2026, while the curve may see bull steepening following the expected PBOC rate cut and CGB buying.

Accordingly, we will maintain an overweight duration position with equal exposure to both onshore rates and high-quality CNH corporate bonds.

Driven by de-dollarisation and RMB internationalisation policies, the CNH bond market has expanded rapidly in terms of liquidity and market depth as issuers have shifted from the USD market to the CNH market for issuance.

New issue premiums, as well as flows from the Southbound Bond Connect programme, are expected to continue providing tactical investment opportunities in this market.

The RMB remains anchored by the PBOC. Its fundamental valuation remains cheap, and with inflows picking up in the second half of this year and a Fed rate cut, we expect RMB appreciation to accelerate from 2025 levels.

Despite numerous challenges faced by the Chinese Mainland economy this year, export growth has remained intact, while China’s GDP growth is broadly in line with the annual 5.0% target.

Heading into 2026, we expect the PBOC to coordinate monetary and fiscal policies to prevent deflation from spiralling further and to support higher consumption, as members of Congress seek to guide the economy into a more self-reliant, sustainable mode.

The Sino-US trade truce is also expected to provide relief and support the stable, positive performance of China fixed income and the RMB over the next twelve months.

Further, the recent rapid expansion of the CNH market from both issuance and investor demand perspectives has shown that China’s fixed income market can provide diversification for global investors amid de-dollarisation and possible further US dollar weakness over the next 12-18 months.

1 Source: Wind, Manulife Investment Management, as of 31 October 2025.

2 Source: Wind, Manulife Investment Management, as of 31 November 2025.

3 Source: Wind, Manulife Investment Management, as of 30 September 2025.

4 Source: Wind, Manulife Investment Management, as of 30 September 2025.

2026 Mid-year outlook: Greater China Equities

Greater China equity markets showed divergent trends in the first half of 2026, with China A-shares and the Taiwan Taiex index registering strong gains driven by resilient technology exports amid global demand for artificial intelligence (AI). Meanwhile, the MSCI China market pulled back, weighed by commerce subsidies amid fierce competition in food delivery and rising AI capital expenditure, which we believe have already been priced in. In this mid-year Outlook, we highlight five positive drivers for China and Hong Kong equities in the second half of the year. Furthermore, the team explains why it believes the Taiwan region’s technology sector should continue to enjoy positive momentum.

2026 Mid-Year Outlook Series: Asia Equities ex-Japan

Asia equities ex-Japan continued the significant momentum from 2025 with strong performance throughout the first half of the year. Amid numerous catalysts, June Chua, Head of Asia Equities outlines in this Mid-Year Outlook why she is constructive on the asset class for the remainder of 2026. Positive drivers include: potential geopolitical resolution in the Middle East and lower energy costs, supportive earnings and valuations, and differentiated growth drivers across the region.

2026 Global healthcare equities outlook: Innovation supports healthcare’s long term case

Global healthcare equities showed resilience amid 2025 volatility. The defensive characteristics, coupled with remarkable therapeutic innovations in the biopharmaceutical, MedTech, and tools sub-segments of this sector, will continue to be rewarded with capital appreciation over a full market cycle. Current valuations relative to the broader market make for an attractive entry point today, and periods like this tend to lead to outperformance for healthcare stocks over the long term.

![]()

©1999 - 2026 Manulife Investment Management (M) Berhad (Registration No. 200801033087 (834424-U))