Financial markets had a rocky start in Q4 2023 as resilient growth and persistent inflation in the US reinforced the Fed's "higher for longer" stance. This triggered a widespread selloff in global equity and bond markets. However, below-expectation inflation and weaker job data in the US prompted the Fed to adopt a dovish stance in November. As a result, both global equity and bond markets saw a significant reversal, leading to a massive rally in the last two months of 2023. Throughout Q4, the US Fed kept interest rates steady and projected rates to settle around the 4.60% mark by the end of 2024, hinting at a potential 75bps rate cut.

Amidst these developments, oil prices experienced notable fluctuations during the same period, particularly in October when prices surged above $90 as the Israel-Hamas conflict escalated. The heightened tensions led to concerns over potential supply disruptions, contributing to the price surge. However, in November and December, oil prices retreated as supply concerns eased, reflecting the evolving geopolitical situation in the region.

Over in China, the PBoC has taken steps to support the struggling property sector by encouraging financial institutions to provide bank loans, debt, and equity financing for a whitelist of 50 property developers. This initiative aims to boost confidence among financial institutions in lending to the sector, demonstrating a proactive approach to addressing liquidity issues and supporting the market's recovery. Meanwhile, China faces potential risks as the US imposes an export ban on AI chips to China, signalling heightened tensions between the two nations. This development could have far-reaching implications for China's technology sector and the broader economic landscape.

In Malaysia, the announcement of Budget 2024 marks a significant step toward reducing the fiscal deficit to 4.3% of GDP in 2024 through targeted subsidy cuts, reflecting the government's commitment to achieving a balance between fiscal discipline and economic growth. Malaysia's GDP surpassed forecasts, reaching 3.3% YoY in Q3, driven primarily by robust performances in the services, construction, and agricultural sectors. Looking ahead, BNM anticipates a 4% expansion in GDP for 2023, with further improvement to 4% - 5% expected in 2024. Moreover, headline inflation has remained steady below 2% YoY for both October and November. In response, BNM kept interest rates unchanged at 3.00% in Q4 and reiterated that future interest rate decisions would remain data-dependent.

Equity market

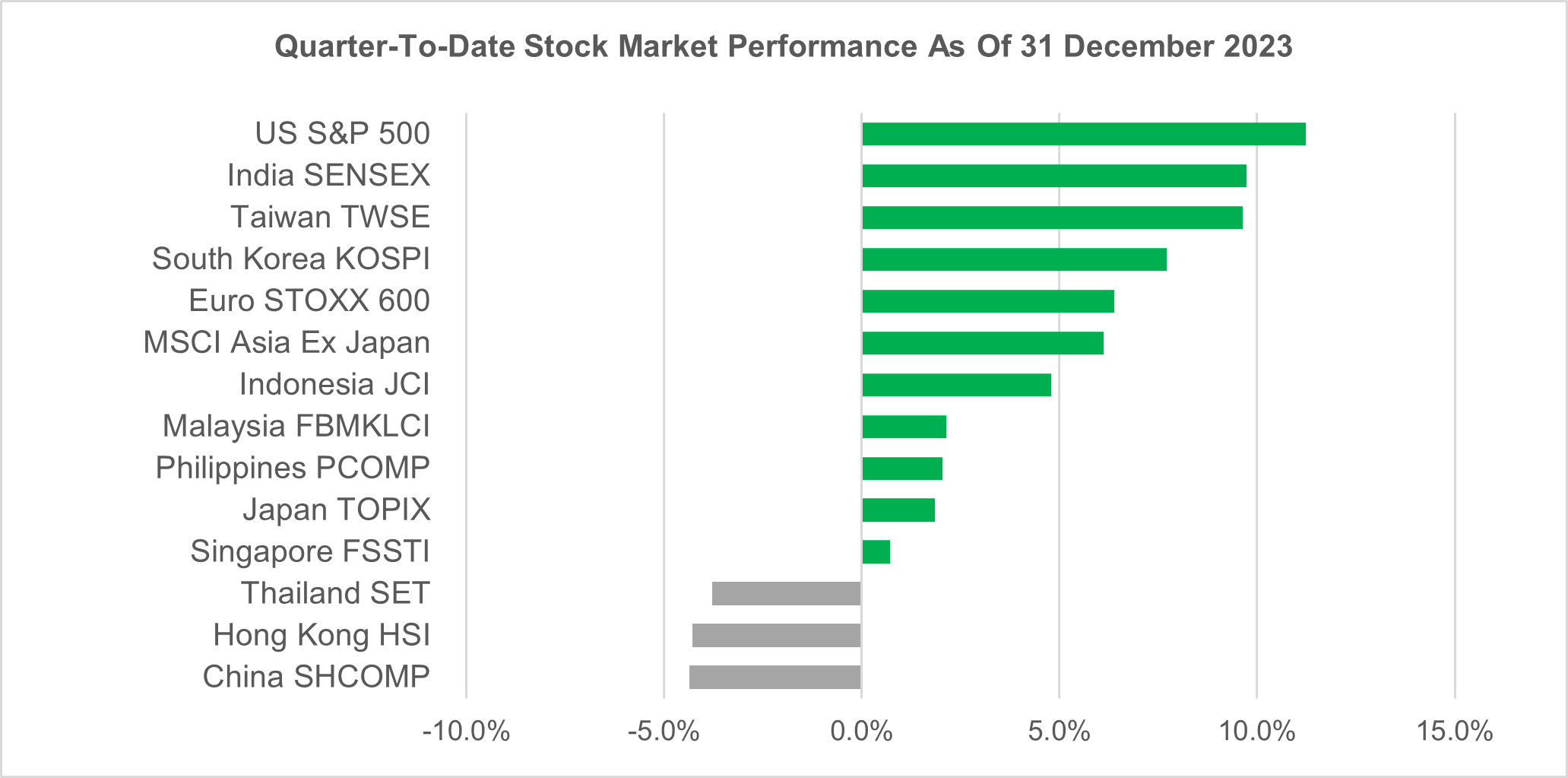

In Q4 2023, global equities got off to a weak start, with losses seen across the board. Both the MSCI World Index and the MSCI Asia ex Japan index experienced significant declines, with losses of 3.0% and 3.9% respectively in October alone. The downturn was largely attributed to the US Fed's "higher for longer" narrative, reinforced by persistent inflation numbers and robust economic data releases in the US. Fortunately, things took a positive turn as lower inflation and a moderating job market prompted the US Fed to adopt a more dovish stance, sparking a substantial rally in most equity markets during the final two months of 2023. As a result, technology-heavy indices such as the US S&P 500, India's SENSEX, Taiwan's TWSE, and South Korea's KOSPI emerged as top performers in the fourth quarter of 2023 due to their interest rate sensitivities.

While several indexes in the region demonstrated strong performance, others faced significant challenges. Chinese indexes such as China’s SHCOMP and Hong Kong’s HSI found themselves at the bottom of the barrel once again, recording disappointing returns of -4.4% and -4.3% for the quarter. Underwhelming earnings reports, concerns surrounding the US-China technology war, China’s struggling property sector and worries about China’s post-pandemic recovery were the main causes of the losses. In addition, Thailand’s SET was the only other index in the region that delivered negative returns, with a decline of -3.8%, as political instability dampened sentiment for the nation.

Taking a closer look at the local equity market, the FBMKLCI continue to play catch up against regional peers, posting a modest gain of +2.1% QoQ, maintaining its positive momentum from the previous quarter. The index's resurgence is attributed to the stellar performance of its top sectors during the period, with the utilities and healthcare sectors delivering impressive returns of +17.4% and +14.2% QoQ, respectively. The utilities sector's strong performance is credited to the government’s energy transition plans. Additionally, utility stocks are known for their strong dividend payouts, adding to their appeal. Meanwhile, the healthcare sector's overall performance was boosted by the enlarged allocation granted to the Health Ministry in Malaysia's budget 2024.

In the broader market, both the FBM100 Index and the FBM Small Cap Index mirrored the FBMKLCI's upward trend, returning 2.4% and 1.0% respectively.

Looking ahead to 2024, we believe that the local equity market is poised for a comeback in 2024, narrowing the gap with regional peers. Performance is expected to be fuelled the domestic economy, supported by clear policy rollouts. Key catalysts such as attractive valuations, high dividend yields, and the weakening Ringgit are likely to attract foreign funds. Furthermore, the global economic landscape is poised for improvement, with the anticipated normalization of interest rates in the 2H 2024 as inflation risks subside.

Source: Bloomberg, as of 31 December 2023. Past performance is not necessarily indicative of future performance.

Fixed income market

Q4 2024 proved to be another volatile quarter for UST yields. Yields initially rose in October, with the 10-year UST surpassing the 5% level for the first time since 2007, driven by the US Fed's "higher for longer" narrative. In a dramatic reversal, the final two months of 2023 saw UST rallying and yields plunging due to softer economic data and lower-than-expected inflation in the US and Europe. This prompted the Fed to pivot to a more dovish stance, citing the surge in UST yields as a natural dampener for inflationary pressure. Consequently, the 2-year, 5-year, and 10-year UST yields bull steepened, ending the quarter with changes of -79bps, -76bps, and -69bps respectively, ultimately closing at 4.25%, 3.85%, and 3.88%.

During their final meeting in 2023, the US Fed maintained the fed funds rates at 5.25% - 5.50% for the third consecutive time, as US economic data showed a slowdown from its strong pace in Q3. The period saw modest job gains, low unemployment rate, and easing but still elevated inflation levels in the US. Chairman Jerome Powell confirmed during that Fed officials had discussed the possibility of interest rate cuts next year. The updated quarterly forecasts indicated that Fed officials expected to lower rates by 75bps in 2024.

In the local market, the MGS yield curve followed the movements of the UST, albeit to a lesser degree. MGS yields experienced decreases ranging from 10bps to 25bps, with the 3-year, 5-year, and 10-year MGS yields ending the quarter at 3.47%, 3.57%, and 3.73% respectively.

Against the backdrop of modest growth and manageable inflation levels for Malaysia in 2024, we are of the view that BNM is likely to maintain the OPR for most of the year. With fiscal consolidation plans limiting government bond supply, the supply-demand profile for government bonds is expected to remain neutral, all of which provides significant support to the local bond market in the coming months. Looking ahead, we hold a positive medium-term outlook for the local bond market, considering the higher likelihood of global rates decreasing in 2024. In the short term, however, movements in MGS could be volatile due to influences from UST movements and changes in global and regional risk sentiment.

Q2 2024 Malaysia Market Outlook: Propelling Ahead

Read moreGreater China Equities 2024 Outlook

This 2024 outlook piece highlights four key megatrends (we call them the “4As”) to help investors navigate the evolving Greater China’s investment landscape.

Five macroeconomic themes for 2024

We dive into the five major forces that will drive global economies and markets in 2024.

Q2 2024 Malaysia Market Outlook: Propelling Ahead

Read moreGreater China Equities 2024 Outlook

This 2024 outlook piece highlights four key megatrends (we call them the “4As”) to help investors navigate the evolving Greater China’s investment landscape.

Five macroeconomic themes for 2024

We dive into the five major forces that will drive global economies and markets in 2024.

©1999 - 2024 Manulife Investment Management (M) Berhad (Registration No. 200801033087 (834424-U))